The intermediary space has been in a state of flux, having had to grapple with a slew of regulations especially post 2020. One of them was insisting upfront margins at client level for all trades. On exit of positions, clients were able to use only 80% of sales proceeds, for entering new positions on the same day. In reality, most brokers transfer the full sale proceedings only on T+1, while some facilitate it on T itself on early pay-in.

Another one was segregation and monitoring of client collateral at the client level. This intends to plug misuses of client’s fund by unscrupulous trading members. Subsequently, intermediaries were also asked not to use the client’s funds for bank guarantees. These bank guarantees are usually issued by banks towards security deposits and margin requirements. While frontline brokerages were already employing best practices, the regulation does cramp those who had been putting clients’ fund for the benefit of raising bank guarantees. By insisting on not using the client’s funds, such funds thus do not get exposed to risks, but increase such intermediary’s working capital requirements.

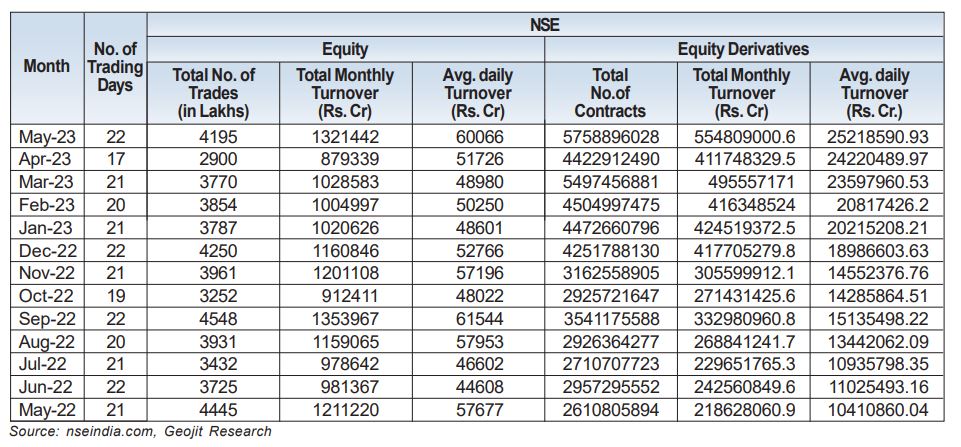

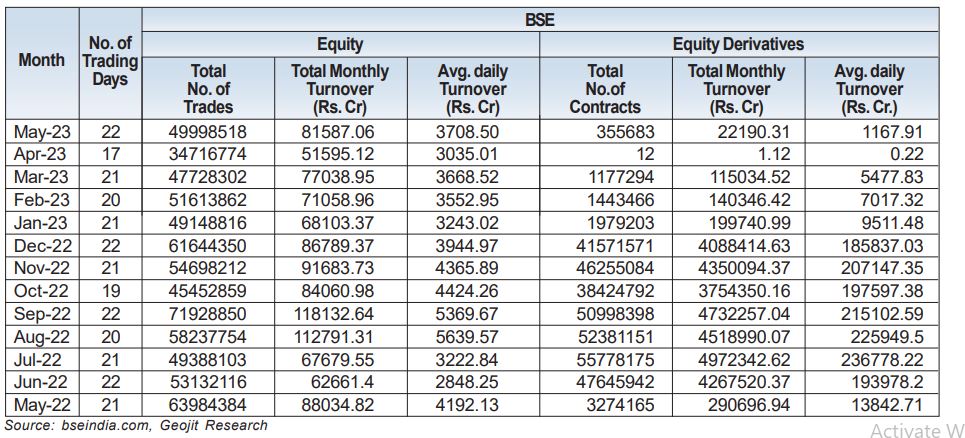

While these regulations protect investors money from misuse, or from excessive exposure to market volatility or overtrading, it is also argued whether the turn of events have crippled volumes at the exchange. A cursory look at the indices would be enough that the outcome has not been bitter, with benchmark indices near record peaks.

There is however a decline indeed in cash market volumes, but not acute enough to be pinned on a specific reason, namely margin. In my opinion, rise in volume is usually seen during periods of high volatility. In fact, VIX has been on a decline from 25 levels to around 11 now, during the last one year. During this period, September and December months saw rise in VIX which, expectedly led to a rise in the number of trades during those months, before easing.

If you look closer, there also has been spurt of high activity in cash market as well, and so it has not been a one way decline anyway. Cash market volumes always go higher when there is a consolidation or decline, after an uptrend in the previous months. May months in both 2022 and 2023 were such periods, with May 2023 witnessing repeated swings throughout within a 400 point range. Volumes were apparently higher on a YoY basis, in May 2023, because, it was preceded by a strong uptrend in mid March through April, resulting in higher volatility with VIX above 13. Volumes usually thin out when there is upside-directional clarity.

Besides the impact of margin rules on leveraged trades, the lack of sizeable fluctuations has also discouraged swing traders or those looking for 1 to 5 day trading window, especially as VIX is closer to record lows. The option space, at the same time, besides being cheaper for the buyers, provides something for everybody irrespective of direction or volatility. But I do not think that traders are abandoning cash market for options. It is just the new age entrants as well as seasoned traders have found opportunities in the option segment. Cash market volumes remain robust. I feel, it is natural to have a vibrant options market co exist with a docile cash market, and I do not see this as a dichotomy or discrepancy that needs to be acted upon, as long as cash market remains deep enough to provide price discovery and easy entry and exit to stakeholders.