“I have never been a guy who tries so many fancy shots because we have to play 12 months of the year. For me, it’s not about playing fancy shots and throwing my wicket away. We’ve got Test cricket after the IPL, so I’ve got to stay true to my technique and find ways to win games for my team….” These were the comments of Virat Kohli, acknowledging the challenges of switching between formats (Test vs T20), after scoring a match-winning hundred in a must-win IPL match against Sunrisers. Espncricinfo.com argues that Kohli may have been responding to the criticism he often faces for how he bats in T20, as we all know that despite accumulating a mountain of runs across formats, he is not a 360-degree player that is required of T20. The natural question here is should one play according to the nature of the format, or should one play to one’s strengths and hope that it be rewarded?

If you can take the cues from cricket allegory, this is a very relevant question that an investor faces regularly. Should investors ditch the long-term holding approach, and play around, when opportune, by letting go of non- performers, or even better, cash out outperformers? While there is no question about the virtues of long-term investing, those who have the time, and inclination to work the resources, have plenty of room to try and experiment towards seeking alpha, or in other words, excess return over what a passive investor would otherwise have earned by just holding on to investments.

Let me recall one more anecdote from IPL. Recently, Punjab Kings made a tactical call as they chased a score of 214 set by the Delhi Capitals with five overs remaining. Atharva Taide, who had scored 55 runs from 42 balls, went off the field and became only the second player in IPL history to retire out. At that point, Kings were 128 for 3, needing 86 to win from 30 balls. With a strong line-up including Jitesh Sharma, Shahrukh Khan and Sam Curran waiting to bat, withdrawal of a struggling player seemed convincing. In investment parlance, this is akin to weeding out nonperformers, but the key is to identify them early enough and make way for proven performers, and giving them enough time to perform, an onerous task that separate sweet success from painful loss.

In longer formats, batters must place a value on their wicket; the best T20 batters are those who unlearn the adage. They “destigmatize risk,” espncricinfo.com quotes the former New Zealand captain Daniel Vettori describing it. Destigmatizing is a difficult exercise because as humans we are hardwired to avoid risk. So, it takes a lot of unlearning to let the guard down and access another area of your resources, albeit temporarily, to maximize your chances of success.

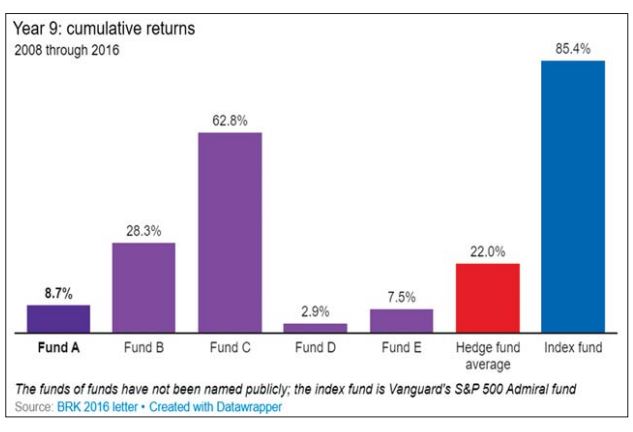

“Though markets are generally rational, they occasionally do crazy things,” legendary investor Warren Buffett, the CEO of Berkshire Hathaway, wrote in his annual letter, saying that his ten-year-long bet with a hedge fund manager delivered an “unforeseen investment lesson.” The letter mentions “Seizing the opportunities then offered does not require great intelligence, a degree in economics or a familiarity with Wall Street jargon such as alpha and beta. What investors then need instead is an ability to both disregard mob fears or enthusiasms and to focus on a few simple fundamentals. A willingness to look unimaginative for a sustained period — or even to look foolish — is also essential.”

Warren Buffet took this bet with Ted Seides of Protege Partners to prove that an S&P fund, would outperform a handpicked portfolio of hedge funds over a period of ten years, because in his view, the hedge fund industry charged exorbitant fees.

While Buffett won according to the terms of the bet, the hedge fund side showed the merits of a bit of extra tweaking and pruning following the 2008 crash, which put them ahead of Buffett’s Vanguard fund until 2012. And Protégé did outperform the market in the previous cycle: according to Investopedia, their flagship fund returned 95% from 2002 to 2007, net of fees, compared to 64% for the S&P 500. In other words, there is no doubt about the merits of long-term holding, but for those with resources for that tweaking here and there, and with an ability to destigmatize risk, there is enough reason to believe that alpha is indeed there for the taking.

Reference: espncricinfo.com; investopedia.com

#Cricket and Stock Market

Click here to read articles by Anand James