In July 2023, the Indian market adopted a sideline stance with a mixed bias, and a downside was triggered from mid-September until the end of October, led by a global sell-off strategy. A reversal has been initiated in November, indicating the potential to sustain the trend in the short to medium term. This shift is attributed to an alteration in the trajectory of global bond yields, supported by a decline in inflation. Central banks are anticipated to respond less aggressively in the future. The Fed should approach this situation cautiously to prevent a slowdown in the economy.

Improvements in the global environment will create a conducive backdrop for a pre-election rally in India. As the US gears up for its upcoming presidential election next year, the global market is showing signs of increased favorability. FIIs sold heavily from August to October. Government spending is expected to continue to be healthy in India, which should be positive for the rural market. Crude prices are falling, which is an advantage for India, fiscally. Pre-election polls indicate a smooth continuation of the reform rally without disruptions. Drawing from historical trends there is a track record of generating robust pre-election returns, reinforcing the potential for a rehearsal rally.

Ease in global trend

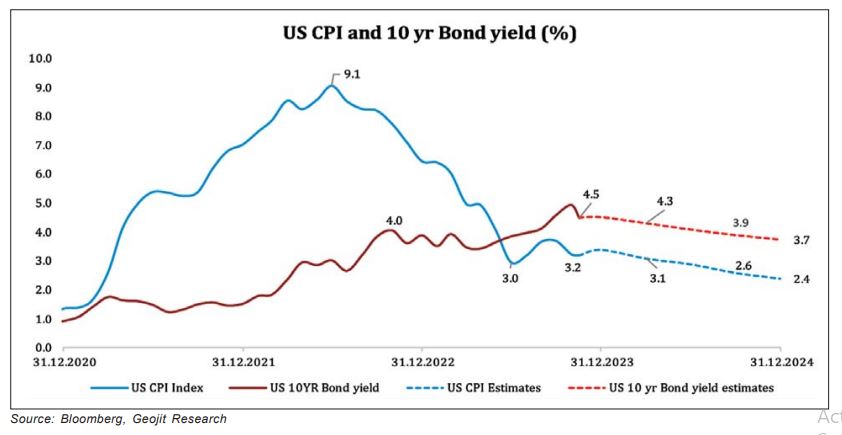

Between August and October, the global market exhibited weakness, primarily driven by apprehensions regarding elevated interest rates and the looming prospect of a more hawkish monetary policy. The US 10-year bond yield during the period increased from 4.0% to 5.0%. A risk-off strategy was triggered as both have an inverse relationship, edging the global market to a sell-off.

Parallely, the inflation level has been drastically falling; however, the prices were a notch above the long-term average, offering little advantage to the stock market. The US monthly CPI fell from 9.1% in October 2022 to 3.2% in October 2023. The high gaps were due to lower-than-normal supply capacities, high fiscal expenditure, and household consumption. However, the economy, over time, appears to have overcome the limitations imposed by the pandemic-induced low capacity, with supplies returning to a more normalized state. Central banks are gradually reducing money supply to contain inflation. Also, geopolitical risk is narrowing, and crude prices are on a downward slope; Brent is below $85. This development instills hope that inflation may become less rigid in the foreseeable future.

US CPI and Bond Yield forecast to decline, but gradually

US October monthly CPI dropped to 3.2% from 3.7% in September, which was better than the estimate. Forecast is that the trend will continue, but though above the long-term monetary target, indicating that interest rates too will remain above the long-term average. A major concern is high ongoing large fiscal program of the government, keeping prices up. With national elections scheduled in both the US and India next year, there’s added impetus to maintain fiscal expenditure. Household consumption is high, led by a high amount of free cash, and a low unemployment rate.

On a positive note, the declining trend of bond yields is poised to benefit equity markets in the short to medium term. It is forecast that US inflation will reduce to 2.4% by December 2024 encouraging a moderation in 10-year bond yield to 3.7% during the same period. In 2023, US 10-year bond yield increased from 3.88% to 5%, up by 112bps, impacting the global market. Currently, the trend has reversed from 5% to 4.5%, and this reversal is anticipated to persist, providing a stimulus to the market in the short to medium term.

Condition is suitable for a pre-election rally

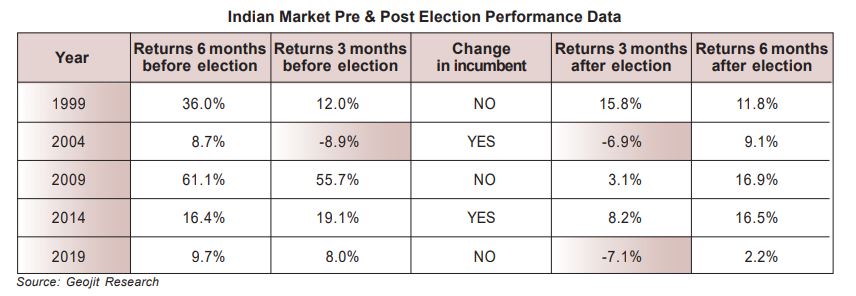

Given that the global market is becoming favorable, in the short to medium-term, India is on the cusp of a pre-election rally. A national election outcome has never impacted the long-term rally in India. Rather, any short-term volatility observed tends to be limited to a period of less than three months, particularly in cases of surprising or hung parliament results. Pre and post-election data below, excluding the 2009 period, where India benefited a lot from the post 2008 global crisis rally, shows that the domestic market has provided a healthy pre-election rally with an average return of 18% for 6 months and 8% for 3 months. And post-election rally gave an average return of 2% in 3 months and 10% in 6 months.

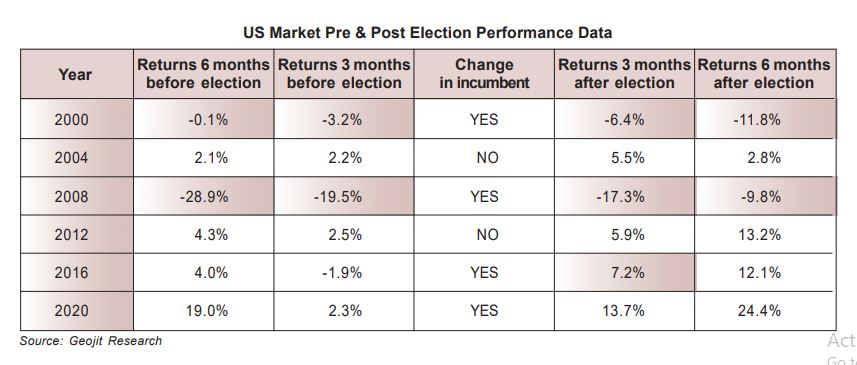

The US presidential election is due in November 2024. Historical trends indicate that the pre-election rally in the US is a bit volatile compared to India. This volatility often manifests as short-term knee-jerk reactions or consolidation, particularly in the 3 months leading up to the election. Such fluctuations can be attributed to a potential slowdown/change in decision-making, government spending, and concerns about the transition in leadership and its impact on economic growth. Data below, excluding the highly volatile 2008 global crisis period performance, shows that the returns from the pre-election rally in the US was an average of 5.9% for 6 months and 0.4% for 3 months, compared to a better post-election return of 5.2% for 3 months and 8.2% for 6 months. The conclusion is similar: other than the 3-month pre-election volatility, the rally is positive.

Based on current poll views, a change is anticipated in the US leadership. Historically, it has not impacted US and global market performance in the long-term. In India, the pre and post-election rally has been positive whatever the election outcome is. And a change is not anticipated by the polls this time. But in case of any big change, the ongoing reformist rally will have a big impact in the short-term post-election.