Indian companies have been reporting superlative profits during Covid times. In 2020-21, the year of the pandemic and the shock of severe lockdowns, the Indian corporate sector is estimated to have seen a massive 138 percent increase in net profits. Part of this was a recovery from a 42 percent fall in the pre-pandemic year of 2019-20. But, the growth in 2020-21 was much more than a mere recovery. In absolute terms, net profit increased from Rs.3.2 trillion in 2019-20 to Rs.7.6 trillion in 2020-21. At this level, the net profit of the Indian corporate sector in 2020-21 was more than twice the average profits generated in the past five years. It was also 81 percent higher than the highest profits earned in any past year.

The computations here are based on a sample of about 30,000 companies for which financial statements are available in CMIE’s Prowess database. These companies account for a miniscule 2.2 percent of the total 1.34 million companies registered with the Ministry of Company Affairs in 2020-21. But this sample of 30,000 Prowess companies accounts for nearly half of the total profits generated by all companies. This is evident from the fact that the Prowess companies paid corporate taxes of the order of Rs.2.1 trillion in 2020-21, which is about 45 percent of the total corporate tax collection of Rs.4.6 trillion by the government in the year.

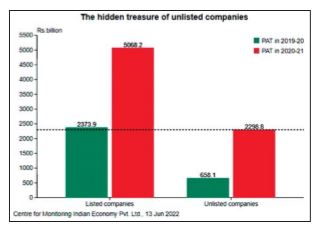

The 30,000-odd Prowess companies include around 25,000 unlisted companies and about 5,000 listed companies. The latter is the full universe of all active-and-listed companies.

Listed companies usually account for about 90 percent of all profits. In 2019-20, their share in total profits fell to about 88 percent and in 2020-21, it fell further to 74 per cent. The fall in share in 2020-21 is rather sharp in a year when the corporate sector as a whole recorded unparalleled profits. This suggests that profits of unlisted companies grew faster than those of listed companies. We examine this next.

Net profits of 4,512 listed companies for which audited financial statements are available for the two years 2019-20 and 2020-21 grew from Rs.2.37 trillion in 2019-20 to Rs.5.07 trillion in 2020-21. This implies a growth of 113.5 per cent. In contrast, in a similar comparison, the net profits of 25,223 unlisted companies grew from Rs.0.66 trillion in 2019-20 to Rs.2.3 trillion which implies a growth of 249 per cent.

Evidently, the phenomenon of extra-ordinary profits in the Covid-shocker year 2020-21 cuts across listed and unlisted companies. Both have made extraordinary profits during the year.

We know from interim financial statements published by listed companies that they continued to report extra-ordinary profits in 2021-22 as well. Net profits of listed companies grew by 66.2 percent in the year. This is nearly half the growth of the previous year. Yet, it catapults listed companies into a new stratosphere of profits. Profits of listed companies touched Rs.9.5 trillion in 2021-22.

Will the unlisted companies continue to record similar superlative profits. They outperformed listed companies in the difficult year of the pandemic in 2020-21. Logically, they should follow the direction of listed companies in 2021-22 as well. Profits of the unlisted companies should continue to soar in 2021-22. We will know only after 6 to 8 months when most unlisted companies will have filed their financial statements with the Ministry of Company Affairs.

But, there is reason to be optimistic. We base this optimism by assuming that (1) the unlisted companies are likely to be smaller than listed companies and (2) if the performance of smaller listed companies was shining in 2021-22 then that of unlisted companies would also be good in the year.

Now, we study the performance of listed companies by their size. We divide the listed companies into ten size bins ten deciles of equal number of companies in each. Decile 1 comprises the largest 10 percent companies, decile 2 comprises the next largest 10 percent companies and so on where decile 10 comprises the smallest 10 percent companies.

First, six deciles reported profits at the aggregate level in 2021-22. In the previous year, only 3 deciles had reported profits and before that only 1 and 2 deciles had reported profits. Therefore, profits are better spread across companies by their size. Secondly, all size groups have seen an improvement in profit performance compared to the average profits they earned in the past five years.

This spread of profits goes beyond bigger companies to even smaller companies. This prosperity of 2021-22 is likely to have spread to unlisted companies as well.