Mutual funds can be considered one of the most versatile investment avenues. They’re known for providing benefits such as portfolio diversification, professional management, convenient accessibility, and the potential for tax savings. Nonetheless, before you commit to investing in a particular mutual fund scheme, it’s advisable to gain a clear understanding of the approach employed to compute the returns, as well as strategies to optimise them.

This article is here to help you get the basics of mutual fund returns and how to make sense of them.

What Are Mutual Fund Returns?

Mutual fund returns are the profits or losses you earn from investing in a mutual fund scheme over time.

As an investor, you get two types of returns from a mutual fund investment – Dividends and Capital Gains.

Let’s understand each of them.

- Dividends are like regular earnings that certain mutual funds share with their investors. These earnings come from the income your investment generates. The payments can either be given as cash or used to buy more units at the current value. But remember, these earnings are not guaranteed. They depend on the scheme’s performance and dividend policy.

- Capital gains are the difference between mutual fund units’ selling and purchase prices. If the NAV of the mutual fund goes up, you make a positive gain. If it goes down, you incur a loss. You receive gain/loss when you redeem or move your mutual fund units to a different scheme.

How Are Mutual Fund Returns Calculated?

The mutual fund return computation method depends on the investment type and frequency, the holding duration, and the compounding effect. Some popular ones are:

1. Absolute Return

This is the simplest method of calculating mutual fund returns. It measures the percentage change in the value of the investment over a given period.

For example, if you invest Rs 10,000 in a mutual fund scheme at a NAV of Rs 100 and sells it after one year at a NAV of Rs 120, the absolute return is 20% calculated as (120-100)/100

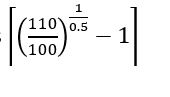

2. Annualised Return

This is a more accurate method. It takes into account the time value of money and the compounding effect. It calculates the average yearly profit your investment would make, whether you hold it for a longer or shorter period than initially planned.

For example, you invest Rs. 10,000 at an NAV of Rs 100 and sell it after six months at Rs 110. The annualised return is 21.55% calculate as

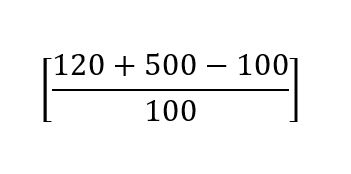

3. Total Return

This includes both dividends and capital gains in the calculation. Suppose you invest Rs 10,000 in a dividend-paying scheme at a NAV of Rs 100, receive Rs 500 as dividends during one year, and sell it at a NAV of Rs 120 at the end of the year. The total return is 25% calculated as

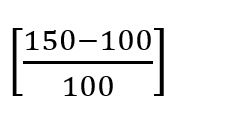

4. Trailing Return

Trailing return is a historical method of calculating returns. It measures the past performance of a scheme over a specific period. It is usually expressed as one-year, three-year, five-year, or ten-year trailing returns. If a scheme had a NAV of Rs. 150 on March 31, 2023, and had a NAV of Rs 100 on March 31, 2022, its one-year trailing return is 50% calculated as

5. Point-to-Point Return

This is a customised method of calculating returns. It measures the scheme performance between any two dates that you choose. You can use this method to compare schemes or various investment periods for the same scheme.

6. Rolling Return

It measures the average performance over multiple periods within a given time frame. You can use it to assess the consistency and volatility of a scheme’s returns over time.

How to Gauge the Performance of Mutual Funds?

To evaluate the scheme’s performance, consider following

- Define your goal: Understand your investment goals and how you’ll use the money. For short-term plans, pick safer options like debt funds. If you’re in it for the long haul, consider riskier ones like Equity or Hybrid funds. Even though they come with more risk, they also offer better chances of getting higher returns over the long run.

- Narrow your preference: Create a list of the schemes in which you intend to invest. Lacking a catalogue of preferred mutual funds will restrict your ability to make effective comparisons.

- Past performance: Examine the historical performance of the Mutual Fund scheme you’ve selected to comprehend the associated risks and the returns it has generated. Given the uncertainty of the future, focus on the fund’s track record and its ability to maintain consistency when making investment decisions. Keep in mind that past performance doesn’t guarantee future results, so it’s wise to regularly assess your investments and grasp how they’re progressing.

- Benchmark comparison: You can assess a scheme’s performance by comparing it to its benchmark index. The gap between the scheme’s returns and the benchmark is called alpha. If the alpha is positive, it means the scheme has outperformed its benchmark.

By following these steps, you can enhance the potential of maximising your investment returns. However, it’s crucial to consistently monitoring your investments over time.

Conclusion

Mutual fund returns are vital in mutual fund investing, but they are just one aspect. As an investor, it is crucial to grasp how these returns are calculated and what factors influence them before you commit to any investment plan. It is equally important to assess mutual fund returns using different techniques and standards so that you can make well-informed choices about where to invest your money.

If manually keeping track of returns feels complex, visit the Geojit website to monitor your investment’s performance.