Fast-moving consumer goods (FMCG) companies, those that sell biscuits and other bakery products, soaps and other toiletries, packaged cooking oil and the type face the double whammy of rising input costs on the one hand and shrinking demand caused by an elevated inflation rate on the other. FMCG companies also seem to be facing adverse terms of trade. Wholesale prices of oils and grains, the two principal components for most FMCG companies have shot up but consumer prices of end products have not increased proportionately.

The wholesale price index for oils and fats in the quarter ended June 2022 was up 13 percent and wholesale wheat prices were up by 10.6 percent. In comparison, consumer prices of bread and biscuits were up by a lower 9.6 percent and 7.6 percent, respectively, and those of soaps and other toiletries were up by less than 9 percent in the same quarter.

Statements by FMCG companies suggest that volumes had declined in the June 2022 quarter. For example, Hindustan Lever’s recent investor presentation showed a decline in volumes for two consecutive quarters for its category of products. The company is a leader in a wide range of consumer goods across foods, toiletries, and home care. Godrej Consumer and Marico reported a 6 percent fall in volumes in the June 2022 quarter compared to a year ago. Britannia Industries, a leader in bakery products, reported that its volumes were flat in terms of the number of packets it sold in the June 2022 quarter.

Most industry leaders lamented in their recent quarterly investor presentations that inflation is hurting demand. The inflation grief of consumer goods companies is touching. But the terms of trade described above are not really severely adverse. The pain is too little and too late, but the moaning is dramatic. The industry had enjoyed elevated profit margin through the pandemic.

Inflation had jumped up to 6.2 percent in 2020-21 after having remained below 5 percent in the preceding five years. In this year of the pandemic and high inflation, consumer goods companies recorded their highest ever sales and the highest operating profit margin in well over a decade.

Cosmetics, toiletries, soaps and detergents companies recorded their best operating profit margin at 21.7 percent in 2020-21 even as sales grew at a healthy clip of 13.3 percent. This was the fastest topline growth in seven years. It is the weighted average of a sample of over 90 listed and unlisted companies in the industry adding up to sales of about Rs.1.2 trillion. 15 of these are listed companies with sales of Rs.0.7 trillion. These had an operating profit margin of 24.5 percent. This was also a record.

Extraordinary margins continued into 2021-22 (23.5 percent) and the topline continued to grow (11.4 percent nominal and 4.8 percent inflation-adjusted) when inflation was still elevated compared to the five years before 2020-21.

Operating margins dropped to 22.4 percent in the March 2022 quarter and to 21.3 percent in the June 2022 quarter when inflation rose to 6.3 percent and 7.3 percent, respectively. This presumably, is the angst of the industry. But these margins are much better than in most pre-pandemic years. Inflation-adjusted sales growth was positive. Year-on-year, sales grew by 4.7 percent in the March 2022 quarter and 6.8 percent in the June 2022 quarter. This suggests that overall, volumes of listed companies have not shrunk as suggested by the industry.

Hindustan Unilever, the leader of the industry said in mid-June that inflation was having a severe impact on its business. Apparently, the company’s response to the threat of inflation was to raise prices of its products. The company raised prices by 9-10 percent in the March 2022 quarter and then raised them again in the June 2022 quarter.

It is apparent then that above some income level the demand for cosmetics, toiletries, soaps, and detergents is price inelastic. And loss of volumes from the price elasticity of demand from lower-income consumers can be easily offset by the richer consumers paying a higher price. In a way then, it appears that HUL’s strategic response to inflation’s demand destruction causes more inflation.

Britannia proposes to do the same. It proposes to raise prices by 6-7 percent in the July-September 2022 quarter since price increases of the previous quarter were not enough. During April-June 2022, the company’s operating profit margin had dropped to 13.3 percent compared to 15.6 percent and 19 percent clocked in 2021-22 and 2020-21. The 50-odd listed and unlisted bakery products companies have seen their average operating profit margin rise dramatically from about four percent in the past to 13 percent in 2020-21. Margins of half a dozen listed bakery products companies have risen similarly from about four percent to 19 percent in 2020-21. These corrected to 15.5 percent in 2021-22 and to around 13 percent in the June 2022 quarter. Britannia’s price hikes seem to protect these elevated margins.

Inflation hurts the lower end of the FMCG market as consumers in the lower income brackets are forced to allocate larger budgets for fuels and other essentials. Discretionary spending on cosmetics and even toiletries, etc. can take a hit. Industry leaders’ plea to bring down inflation is possibly to bring those budgets back into consumer goods.

Recent news reports suggest that FMCG companies may pause their price hikes as commodity prices have eased. Apparently, they would not like to lose the lower end of the market if margins can still be protected. A fall in input costs may enable that in the coming quarters.

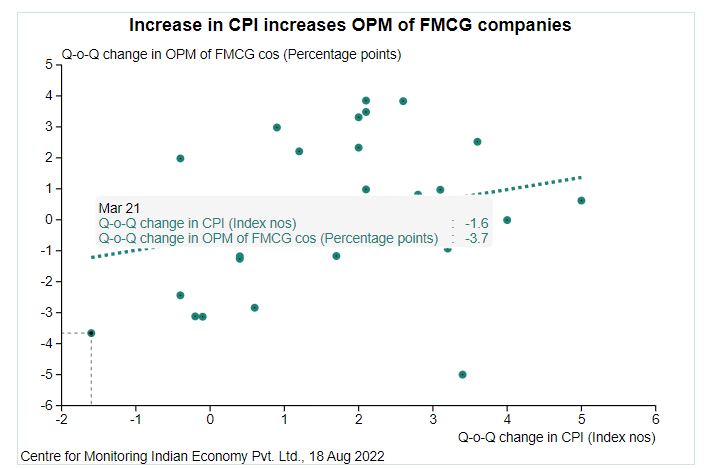

The operating profit margin of a little over 100 FMCG companies rose from 15.8 percent in the March 2022 quarter to 16.4 percent in the June 2022 quarter. Operating profit margins increased by 0.6 percentage point when the consumer price index rose by a record 5 points (from 166.5 to 171.5) in this quarter. Quarterly data of the last seven years indicates that an increase in consumer price inflation is positively correlated with an increase in the operating profit margins of these FMCG companies. If inflation is a threat to FMCG companies, they manage this threat very well.