Sankaran Naren, Executive Director and Chief Investment Officer, ICICI Prudential Asset Management Company has over 30 years of experience in the financial services industry which includes investment banking, fund management, equity research, and stock broking operations. He joined ICICI Prudential AMC in 2004 and oversees the entire investment function across the Mutual Fund and International Advisory Business of the company. Naren is also a member of the Committee on Equity matters at AMFI.

In this exclusive interview with Geojit Insights he talks about the impact of Covid on the Indian markets, asset allocation and investing in mutual funds to achieve short-term and long-term goals.

What according to you is the impact of Covid resurgence on markets and what is the way forward for the equity market?

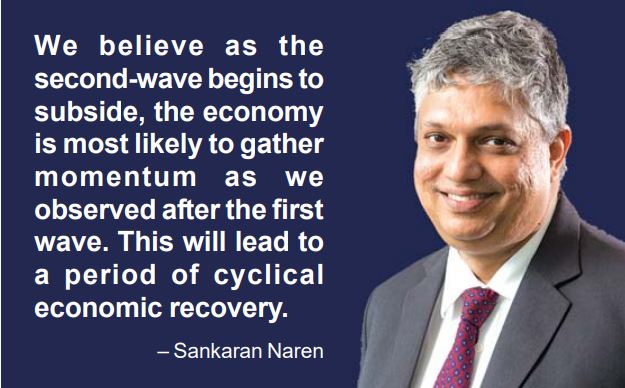

Since the second wave of Coronavirus is an evolving situation, the sentiment in the market is that of uncertainty. However, this is not the first time the market is facing uncertainty related to the pandemic. Indian investors and corporates have faced a similar scenario a year ago, and so from that perspective, for now, we are better placed to face the challenges developing from the second-wave. In due course, as vaccination drive becomes more widespread, the virus spread is likely to be under control, a scenario which we have already seen happen in the developed world. We believe as the second-wave begins to subside, the economy is most likely to gather momentum as we observed after the first wave. This will lead to a period of cyclical economic recovery.

At the same time, the US Federal Reserve is continuing with its accommodative stance on its monetary policy. However, this stance may not last for long. Therefore, one of the key risks global equity markets likely to face is reversal in Fed stance leading to tapering of quantitative easing program. This development has the potential to derail global and US markets. Since we live in a world which is much more intertwined than earlier, it is not just local conditions, a global development of this magnitude is sure to impact domestic market as well. Needless to say, this could keep volatility at elevated levels as and when it plays out.

You have been vocal about asset allocation. What is your take in the current market environment?

We need to shift focus from long-term debt funds to asset allocation funds where investors get a mixture of equity and debt. While the debt cycle has possibly ended on the duration side, equities have had a healthy period. Equities can deliver returns despite being a much riskier asset class. On the other hand, debt is a lower-risk asset class in comparison to equities, but debt funds could offer sub-optimal returns during this phase. Hence, we are recommending investors to move to dynamic asset allocation category.

For investors looking to take exposure to equities can consider investing through the SIP route with a long term (10-year) investment horizon. Those within an investment horizon lesser than 5 years, should consider investing in a scheme which is hybrid in nature such as the asset allocation scheme or the balanced advantage category of schemes. These categories of funds are well placed to take advantage of market volatility and such products have the flexibility to move assets between equity and debt based on their relative attractiveness.

When it comes to SIP which category of funds can one consider now?

We believe value is in the early stages of playing catch-up with growth and quality which has significantly rallied over the past few years. There is good scope for return to be made from value investing. Even today there are many sectors where valuations are attractive. Many of these pockets have not delivered returns in the period after 2008. When it comes to equity investing, value oriented approach is something we would actively recommend for long term investors to consider. So, value is clearly a segment where one can initiate an SIP with long term approach. For those looking to invest in broader markets, can consider investing in mid and small cap funds but with an investment horizon of 10 years.

What is your take on the fixed income space? Which are the pockets you are positive on?

As a fixed income investor, one should be cognizant of the fact that capital gains strategy has played out meaningfully and going forward return expectations need to be moderated. Also, in terms of portfolio selection, you would need to focus on the steepness of the yield curve and the credit spread of the fixed income assets.

We believe that we are currently at the fag end of the interest rate cycle. Thus, we suggest a more nimble and active duration management strategy that can allow you to benefit from the high term premium and manage your portfolio from the expected high interest rate sensitivity. We continue to recommend an accrual strategy with an aim to benefit from higher carry. Given that the spread premium is reasonably high, compared to the repo rate, there is a compelling opportunity to invest in good quality AA corporate bonds.

For long term investment in debt, one can consider dynamic duration category of fund.

What would be your recommendation for short term parking of funds in debt market?

For parking surplus funds, one can consider any short duration fund across categories such as low duration, ultra short duration and floating interest rate category of schemes.

Similarly, if one is looking for long term debt market exposure what would be your recommendation?

For long term investment in debt, one can consider dynamic duration category of fund.