By Anu V Pai, Vinod TP

The first half of the year 2021 turned out to be a volatile one for agriculture commodities. While the year kicked off on an optimistic note, the second wave of Covid-19 pandemic in the country played spoilsport. Lockdowns and other restrictions placed in many states to control the surge of infections affected trade and demand.

Oil and Oilseeds rallied….

All the constituents in the oilseed portfolio traded on a greener turf. Among these, Soybean and mustard seed rose the most and hit new highs. Soybean futures in the NCDEX platform increased more than fifty percent in the first half of the year. Sharp rise in demand for Indian soymeal along with concerns brewing over the fall in domestic output during the current kharif season due to poor monsoon led to the upside momentum. On the international front, the fall in production from Brazil and Argentina due to drought amid lower carryover stocks kept the prices on the firm note. However, later the prices fell due to lockdown restrictions across the states and expectations of good monsoon. Then it revived due to the opening up of markets, and an increase in MSP for soybean followed by slow pace of sowing in key growing regions like Madhya Pradesh and Maharashtra. Likewise, uptrend was observed in mustard seed as well. It rallied to a record high after a brief panic sell-off witnessed in the second quarter owing to a rise in domestic mustard seed output along with concerns over the spread of Covid-19 and subsequent closure of spot markets. However, prices recovered later after the government relaxed restrictions, banned the blending of mustard oils with other oils and the gradual decline of arrivals in the spot market as it eventually entered into a lean season.

In the entire edible oil segment, refined soy oil rose the most. Refined soy oil prices extended its gains that started in the mid of last year. This was due to the firmness in international markets on global supply-side disruptions and lower edible oil stocks. Further, improved demand owing to Ramadan also fuelled up the prices in the second quarter of this year. There were some corrective moves after the government imposed lockdowns and restrictions in major Indian states. But later prices started to show revival on the back of rise in crude oil prices.” The crude palm oil prices also rose on back of higher domestic demand for cheaper oil along with strength in international prices but it was less compared to other edible oils. The rise in benchmark CPO prices in BMD Malaysia on lower output and stocks with strong export demand from China and India supported the gains in Indian markets. But prices had started declining on signs of a gradual rise in output in Malaysia. On the domestic front, a cut in import duty of palm oil products to cool off the domestic prices by the government softened the prices further. However, it started to see some revival on back of higher NYMEX crude oil and reports of higher utilization of palm oil as biofuel in major producers.

Spices Recover….

Spices complex on NCDEX kicked off the year 2021 on a relatively firmer note, but the outbreak of the second wave of Covid-19 infections put a break on the advances. With the resurgence of Covid-19 infections, many major markets for physical trade in spices were either closed or functioning partially during April-June period, which also coincided with peak arrival season of spices like turmeric, jeera, and coriander. Among the actively exchange traded spices, turmeric gained the most followed by coriander and jeera. Turmeric prices have been more or less on a steady rise since hitting a six-year low in March last year and the momentum continued till February 2021, when it rallied to a five-year high. While its immunity-boosting properties generated demand, decline in production last year due to unfavorable weather in some of the major turmeric growing regions and good export demand propelled the rally. According to the Spices Board, Turmeric production in FY 2020-21 is seen at 1101920 tonnes, down by about 6.5 percent from 1178750 tonnes produced in 2019-20, while exports of turmeric in the FY 2020-21 is seen at 1, 83,000 tonnes, a jump of 33 percent from the previous fiscal. However, higher carryover stocks along with export and domestic demand being affected due to Covid-19 resulted in a retreat in turmeric prices from the five-year highs. In the meantime, the new kharif season has begun and the initial expectation on acreage is mixed. While turmeric prices are relatively higher than it was last year, higher MSP in crops like soybean may probably see farmers shifting to such crops. Coriander and jeera too had a firmer start this year, but the resurgence of Covid-19 infections during the second quarter of this year led to subdued demand from both domestic as well as from the international markets. Higher production estimates for coriander in the 2020-21 rabi season weighed on as well. The Spices Board has pegged coriander production at 822,210 ton, up 17.3 percent on year, while exports from India were up 21 percent on year at 57,000 ton during the same period. In case of jeera, the spice has been mostly confined to a range of Rs.15200-12450 per 100 kg since March 2020 and the broad sideways moves continued in the first half of this year as well. Lingering worries over demand due to various restrictions imposed to contain the spread of Covid-19 pandemic and rise in supplies are weighing on jeera prices, while lower production estimated for 2020-21 season and rise in exports lent support, limiting losses. According to the Spices Board, Jeera output in the FY 2020-21 is estimated to be 856505 tonnes, down by six percent compared to 912040 tonnes produced in FY 2019-20 and exports are seen at 299000 tonnes, up by 40 percent compared to the previous fiscal.

Other Commodities…..

Among the other commodities, Chana was seen steadily rising since the beginning of this year on robust demand, buying by NAFED and prospects of lower production than the initial estimates for the 2020-21 rabi season. Subsequently, the pulse climbed to its highest level in about three and a half years in April before starting to retreat. Lockdown and other restrictions imposed to control the spread of Covid-19 resulted in a decline in demand. Adding to the woes was relaxation in import norms for certain pulses and imposition of stock limit by the central government on pulses except for moong amidst higher stocks with the NAFED and notification on open market sales. In Cotton complex, prices remained firm in the last six months with intermittent profit booking. Fall in global production in India and Brazil coupled with higher demand led to lowering global ending stocks for the 1st time in four years. On the domestic front, erratic distribution of rains during the current monsoon season caused slow pace of cotton sowing in India. Moreover, firm domestic and export demand after easing lockdown/restrictions pushed up the prices higher. At the same time, the bi-product, cottonseed oil cake rose continuously on the back of strong demand from poultry and feed industry amidst of waning supply in the spot markets. Further, concerns over lower domestic cotton output also supported the prices. Castor prices rose more than 20 percent due to renewed demand for meal in the domestic and international markets. Moreover, fall in output during the last season along with the slow pace of sowing accelerated the gains. Guar complex on NCDEX ended the first half of the year on a firmer note following a lackluster beginning. Fall in export demand has been weighing on guar prices. According to the provisional data from the Agricultural and Processed Food Products Export Development Authority (APEDA), the guar gum exports from India declined by 38 percent to 2.35 lakh tonnes during April-March (2020-2021) this fiscal vs 3.81 lakh tonnes during the corresponding period last year. However, rise in crude oil prices and prospects of higher demand currently lifted both guar seed and guar gum futures.

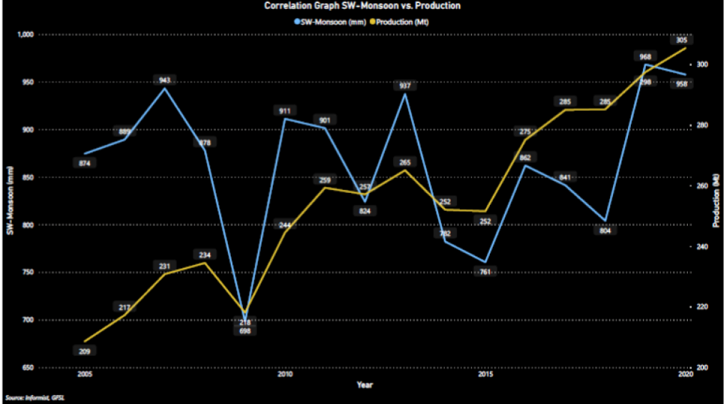

Southwest Monsoons and Kharif Sowing 2021

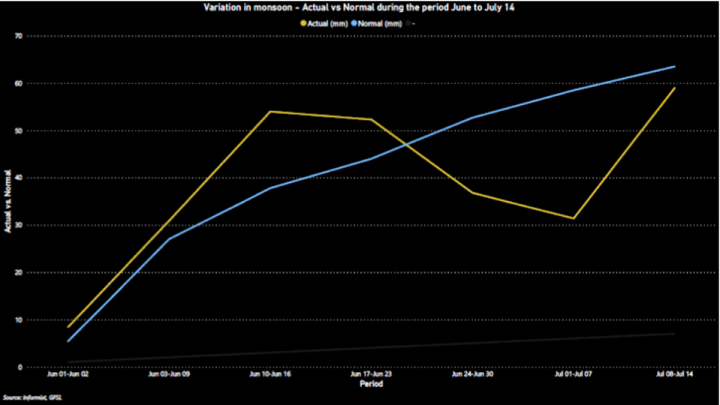

The new kharif season has already begun, and the government has set a target of total food grains production for 2021-22 at a record 307.31 million tonne, comprising 151.43 MT in kharif season and 155.88 MT during rabi with a target for rice production being fixed at 121.1 MT, wheat at 110 MT, pulses at 25MT, coarse cereals at 51.21 MT and oilseeds at 37.5MT. Except Sunflower, tur and sugar cane, all other crops’ sowing was delayed and is below the normal acreage during this year. As of July 16, farmers have sown crops across 61.2 mln ha, down by 11.6 percent from a year ago. This break in monsoon has hit kharif sowing in the country. The IMD has earlier predicted a normal monsoon to 101 percent of LPA, with an error margin of 4 percent with a timely onset. However, monsoon hit Kerala coast three days after the normal date on 1 June. Finally, it covered entire country with a delay of five days on July 13 on account of three-week gap in monsoon advance. As of July 16, the country has so far received 287.7 mm of rainfall, 7 percent below normal of 308.4 mm for the period. Except for southern peninsula, all other regions in India received below-normal monsoon.

Looking ahead, lingering worries over another wave of Covid-19 infections and ensuing concerns over demand as well as supply chain disruptions will have a huge bearing on agriculture commodity prices. Yet, progress, distribution and intensity of Southwest Monsoons, progress in kharif sowing, export demand and government interventions like imposition of stock limits, export-import policy tweaks etc., will be the other predominant factors that will turn out to be decisive.