Consumer sentiments have been rising steadily in India since June 2021. Between June 2021 and February 2022, the Index of Consumer Sentiments (ICS) scaled up by a substantial 31.9 percent. In the first three weeks that ended in March, the index scaled up by another 8.2 percent. This marks a smart recovery in consumer sentiments from the setback it suffered in the second wave of Covid-19. Consumer sentiments had fallen by 15.7 percent between March and June 2021 the period of the second wave of Covid-19. The recovery since June has more than covered that fall.

This recent increase in consumer sentiments is the result of a sharp increase in the proportion of households reporting an increase in their incomes compared to a year ago and also the proportion of households that expect their incomes to rise in the coming year. This has helped increase the proportion of households that believe that this was a better time to buy consumer durables than a year ago. The only caveat was that such optimism was not equally evident on household views on the economic and business environment. They were reticent on both, the short-term and long-term prospects of the Indian economy.

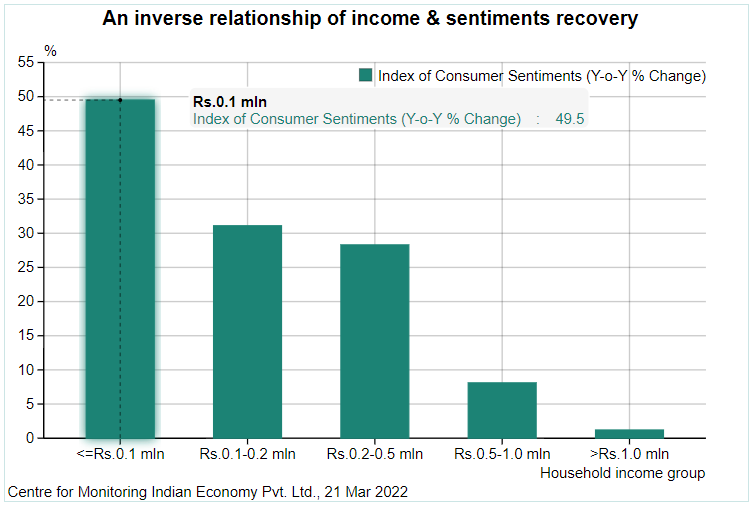

Interestingly, the improvement in consumer sentiments between June 2021 and February 2022 has been the most among the poorer households. In fact, the scale of improvement diminishes as the broad household income levels rise. This is because it was the sentiments of the poorer households that suffered the biggest hits during the second wave of Covid-19. The poorer households have bounced back from a very low base.

Consumer sentiments of households that earned less than Rs.100,000 per annum rose by 49.5 percent after a fall of 28.7 percent. While this impressive recovery is a relief, it does not matter much in the overall household sentiments in India because this is a small set of households with a smaller share of the Indian consumer market at its command. Before the pandemic, in 2019-20, this group of households accounted for 9.8 percent of all households and 3.1 percent of total household incomes. In 2020-21, the year of the pandemic, its share grew as the pandemic impoverished households. The share in total households rose to 16.6 percent and in total income to 5.7 percent. The first half of 2021-22, which includes the impact of the second wave, has not changed these proportions much.

Households with an annual income between Rs.100,000 and Rs.200,000 seem to be shrinking substantially in 2021-22. In the past between 2017-18 and 2020-21, they accounted for 44-45 percent of all households. But, in the first half of 2021-22 their share has shrunk sharply to 25 percent. Their share in total income has more than halved from 31 percent to 14 percent. Consumer sentiments of this group have risen by 31 percent between June 2021 and February 2022.

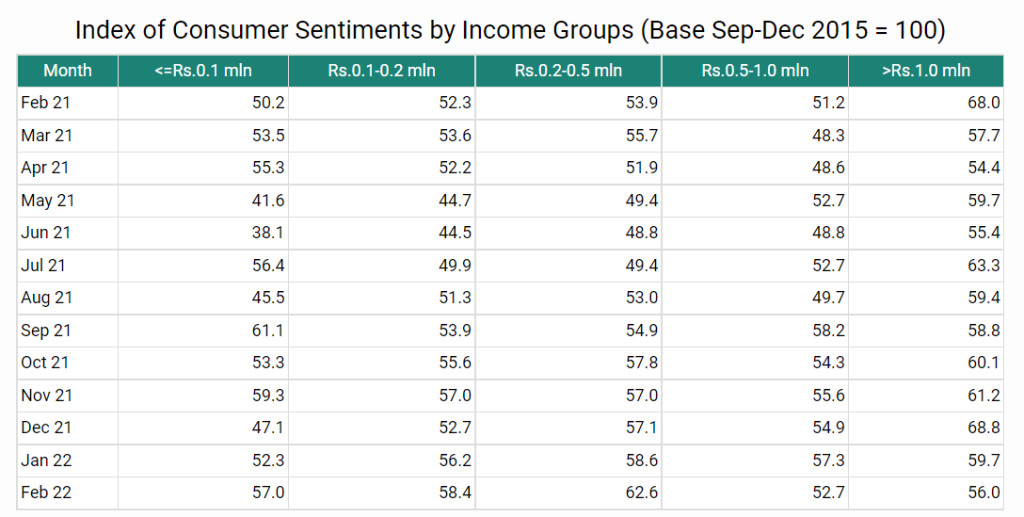

Households seem to be migrating from the income bracket of Rs.100,000-200,000 to higher income brackets. This is evident from the fact that while the number of households in this bracket have shrunk in the first half of 2021-22, those in the lower income bracket have remained unchanged and the higher income brackets have expanded in terms of households. Signs of household income recovery were visible in the first half of the year. Data for the remaining months of the year are still awaited. But, the continued recovery of consumer sentiments indicates that household incomes could be continuing on their recovery path during the second half of 2021-22 as well.

Consumer sentiments of households with annual incomes between Rs.200,000 and Rs.500,000 increased by 28.3 percent between June 2021 and February 2022. This income bracket has now become the most important segment of the Indian consumer market. It accounts for 50 percent of the households and 56 percent of all household incomes. Its share has gone up from 33 percent of all households and 45 percent of all household incomes till recently. In absolute terms, the consumer sentiments index is at the highest in this income group compared other major income groups.

The consumer sentiments index of households that earn between Rs.500,000 and Rs.1 million annually increased by 8.1 percent since June 2021. Households of this income bracket were resilient to the second wave. Their consumer sentiments stagnated and did not decline like in all other cases. This is a relatively small set of households. It accounts for only about 7.1 percent of all households but, it commands a much larger, 19.7 percent share in the total income pie of all households.

Households that earn more than Rs.1 million account for a small share of the total consumer markets in India. In the first half of 2021-22, they accounted for 0.9 percent of all households and 5.2 percent of total household incomes. Their consumer sentiments had fallen by 3.9 percent during the second wave. But, their recovery since then has been unimpressive at just 1.2 percent. The consumer sentiments of this group had peaked in December 2021 and have fallen in both, January and February 2022. About 75 percent of the income of this group is saved. Presumably, the bearish trends in the stock markets have adversely impacted the sentiments of this rich group.

The middle-income groups seem to be seeing a good increase in income and this is reflected in an improvement in their sentiments as well.

Article first published in Business Standard.

Author is MD and CEO of Centre for Monitoring Indian Economy Pvt. Ltd