by Vinod TP

The edible oil basket has been fascinated by bulls and reached multi-year highs in the last month. The global supply-side disruptions, drought in South American countries, fall in output, geo-political tensions, rise in crude oil prices, government policies and substantial fall in ending stocks are the main factors that fired the rally. The Russia-Ukraine conflict has significantly impacted the global edible oil supply chain. The consequences of it are being reflected in the Indian markets as well since India is one of the largest consumers of edible oils.

Soybean oil rallied on lower ending stocks

The king of edible oils, Soybean oil futures in the U.S Chicago Board of Trade (CBOT) platform rose more than 50 percent, since December 2021, hitting a 14-year high in the last month. Significant fall in global ending stocks and higher global consumption has led to a rise in prices. Fall in soybean production in South American countries like Brazil and Argentina due to severe drought for the past two years and supply-side disruptions in Argentina due to the Covid-19 have caused a sharp fall in ending stocks. Moreover, improved domestic demand for soy oil from the U.S and India supported the gains as well. According to the US Department of Agriculture’s (USDA) March report, global ending stocks for soy oil were sharply down by 23% to 3.98 million tons compared to pre-covid levels. The shortage of stocks was further aggravated by the rise in NYMEX crude oil prices along with the Ukraine-Russia conflict disrupting the trade flow of sunflower oil, which is another most-consumed edible oil. However, major gains in CBOT were capped even during the Russia-Ukraine crisis due to a rise in premiums in the near month contracts compared to far months. The wide difference between the two contracts resulted in an arbitrage opportunity followed by a fall in near-month prices. On the domestic front, similar sentiments were witnessed in soy oil even after SEBI banned futures and options trading in the commodity on NCDEX. According to NCDEX polled spot soy oil prices and refined soy oil prices rose by more than 39 percent after the ban, tracking gains from international markets. However, the central government regularly intervened to cool off edible oil prices by cutting import duty on edible oil along with imposing stock limits in oilseeds. This encouraged large imports of edible oil to India for taming inflation. The Solvent Extractors Association (SEA) reported that soy oil imports to India rose by 72% to 1.63 million tons during the marketing year (November-February) compared to the same period the previous year.

CPO skyrocketed on production and stock concerns

A similar situation of tightness in global supplies is being witnessed in palm oil market as well. The global benchmark, Bursa Malaysia Derivative (BMD) Malaysian Crude the palm oil prices skyrocketed 65 percent from mid of December 2021 and made a fresh new high in the last month. The steep rise was mainly driven by a fall in production in Malaysia for the last four years. Shortage of labour in Malaysia due to Covid-19 lockdown restrictions followed by floods disrupted the plantation operations, leading to a drop in palm oil output. Moreover, rise in domestic consumption from the largest consuming countries like Indonesia, India and China supported the gains. This has subsequently resulted in drying-up of global ending stocks. The USDA reported that the global ending stock dropped by 5 percent to 13.56 million tons compared to the pre-covid levels. In the meantime, the export of oil from the world’s largest producers has remained firm during the past few years due to higher domestic consumption in India and China. Also, the announcement of the Indonesian government to restrict exports of palm oil and increase the limit of domestic sell from 20 percent to 30 percent will likely reduce the Indonesian export volume and further tighten global supplies. The conflict between Russia and Ukraine has further aggravated the situation. The last two factors led to higher volatility of palm oil prices in benchmark. On the domestic front, the situation is almost identical. Initially, the cut in import duty of palm oil products by the government had softened the prices. However, prices later recovered. The spot polled CPO prices rose by nearly 50 percent even after the SEBI ban on futures contract of crude palm oil on MCX. But government intervention on cut in import duty and agri cess limited major upside. The cut in duty resulted in large imports of RBD palmolein to India. According to SEA, the RBD palmolein rose from 21,601 tons to 519,450 tons during the marketing year 2021-22.

A drop in global production and lower inventories spurred mustard prices

In the global market, International Continental Exchange (ICE) canola (Canadian mustard oil) May contract futures prices rose more than 16 percent to $1123 per 20 tones in the last month. This is mainly due to a fall in output in major producing nations like Canada and China, thereby pushing down global ending stocks to multi year lows. The drop in output in Canada was due to record hot summer temperature last year which drastically reduced canola yield. The USDA reported that the global ending stock fell by more than 50 percent to 4.45 million tons compared to peak levels in 2018. Moreover, drought in Canada last year significantly affected the crushing of rapeseed and thereby exports as well, which itself contributed to 50 percent of global exports. Further, the conflict between Ukraine and Russia is likely to impact exports. Canada and China together contribute 20 percent of mustard and 15 percent of mustard oil global exports respectively. Similarly, a northward journey was witnessed in mustard seed prices in the Indian market too, but it was short-lived and is currently trading lower due to the expectation of record output in India and rise in arrivals that started from the end of January 2022. According to Central Organisation for Oil Industry and Trade, India’s mustard seed production in the crop year 2021-22 is expected to be higher by 29% at an all-time high of 10.95 million tons compared to last year.

Rise in sunflower oil prices in spite of higher global production

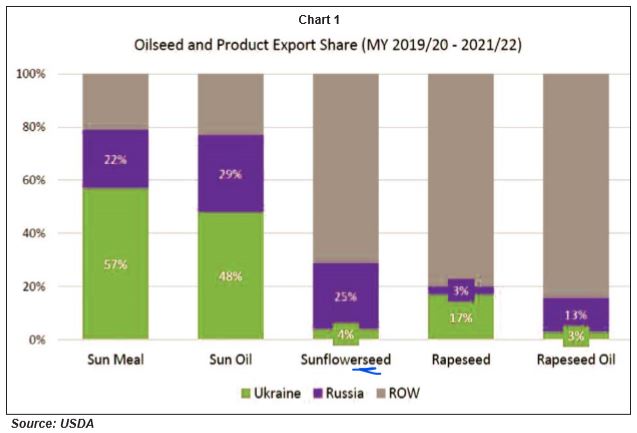

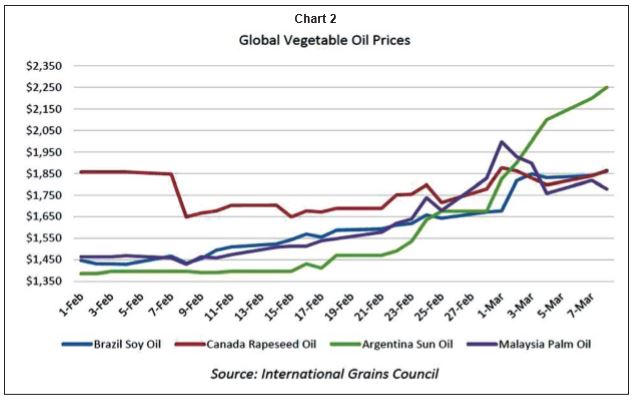

In a normal year, countries like Ukraine and Russia together contribute about 80 percent of the global sunflower seed meal and oil trade. Due to the Black Sea unrest, the port and crushing facility in Ukraine have been muted. According to USDA report, seed exports are down by 57 percent, oil exports are down by 14 percent and meal exports are down by 13 percent respectively. As a result, Ukraine’s sunflower ending stocks are up nearly seven-fold last month to 1.9 million tons. The association also reported that most of the produce has been damaged and spoiled. In Russia too, export enquiries have declined with exporters facing uncertainties in Black Sea shipping routes and the impacts of sanctions. According to USDA, the Russian exports were down by 33 percent for sunflower seed, 4 percent for sunflower oil and 3 percent down for sunflower meal respectively. Uncertainty over Black Sea exports has led to prices from the competitor Argentina jumping 47 percent for sunflower oil. Due to the strife in the Black Sea region, India’s imports of sunflower oil declined in February to 1.5 lakh tons compared to usual imports of 1.75 to 2 lakh tons. If war continues, shipment of sunflower oil may continue declining in the coming months. Looking ahead, lower global carrying stocks, tight supply and geo-political tensions are likely to keep the edible oil prices on a firmer note. Around 70 percent of our domestic edible oil demand is largely met by imports, hence impacting the domestic edible oil prices. Moreover, palm oil is the major contributor of edible oils in Indian markets. Presently, lower palm oil stocks and dip in production expectation in Malaysia, export restrictions in Indonesia and upcoming festivals like Easter and Ramzan will support CPO prices in the near term. The labour shortage in Malaysia is still hurting the palm oil output. Any intervention by the Malaysian government to increase workers would raise the hopes of higher palm oil production. In the domestic market, despite lower global edible oil inventories, higher soybean and mustard seed output in India may probably provide some relief. Any domestic deficit in sunflower oil is likely to be offset by higher domestic availability of mustard and soybean oils. Record mustard output estimation is more likely to see a higher domestic crushing. Imports are expected to pick up in India as government is regularly intervening in the market to check prices. Moreover, current domestic stocks in the ports and pipeline are also increasing, which is a positive sign. However, demand for edible oil is anticipated to scale up as government relaxed restrictions and

economic activities have gathered momentum after mega vaccination drive. Still, the emergence of a new omicron variant and another lockdown in China and other southeast Asian countries must be closely watched.