The last six years have been unusually volatile and uncertain for the global economy. The COVID shock, Russian invasion of Ukraine, elevated inflation triggered by disruptions in supply chains, the consequent monetary tightening by central banks, the Gaza conflict, and Trump’s tariffs happened in quick succession impacting markets. Of these disruptions, only the COVID shock impacted the global economy significantly triggering a global recession in 2020. The other crises impacted the markets only temporarily. As economies exhibited resilience, markets recovered.

Trump’s tariffs triggered heightened volatility in markets. However, global economic growth was not much impacted by trade-related disruptions. Global economy is estimated to have grown by 3.3 percent in 2025. However, the lingering conflict in West Asia, closure of the Strait of Hormuz, the sharp spike in the price of crude and disruptions in the availability of LPG and LNG have started impacting growth, particularly in emerging and developing economies.

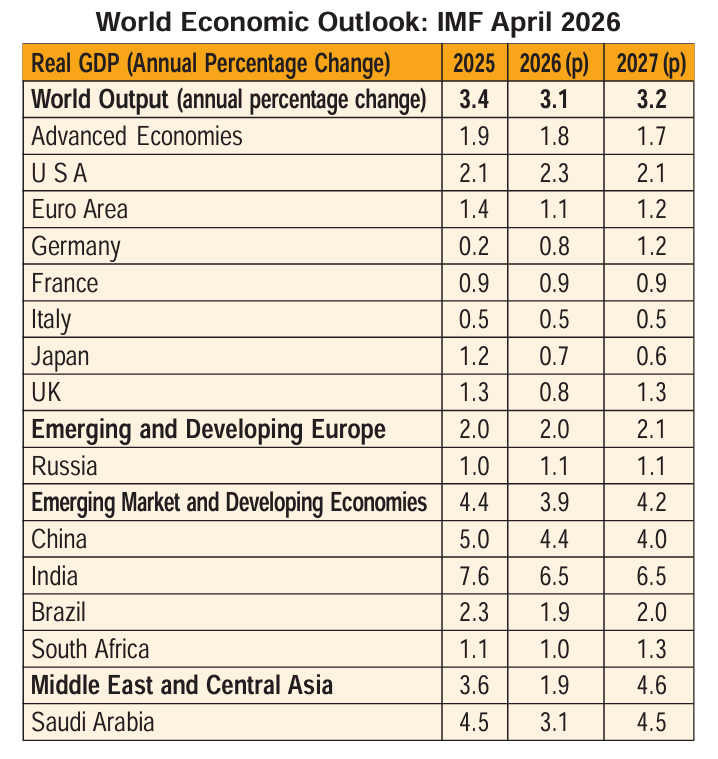

IMF’s latest (April 2026) World Economic Outlook has projected global growth to decline to 3.1 percent in 2026 and then slowly recover to 3.2 percent in 2027. IMF also projects higher inflation of 4.4 percent for 2026. Energy importing emerging and developing economies will be the ones worst affected by the conflict. See the table:

The above growth projections assume a short-duration war. If the conflict extends over a longer period disrupting energy markets further, global growth could dip to 2.5 percent. In such a scenario stock markets will come under increasing pressure. Inflation will rise; global inflation is projected at 4.4 percent for 2026, up from 3.8 percent earlier.

India’s resilience

India’s growth has been revised up from 6.4 percent earlier to 6.5 percent in the latest April report. India’s growth has been strong since mid 2025. The growth momentum continues. Domestic projections for India’s growth are better. RBI’s growth projection for FY27 is 6.9 percent. As per the revised GDP series India’s GDP growth rates for FY24, FY25 and FY26 have been estimated at 7.1 percent, 7.2 percent and 7.6 percent respectively. This is impressive growth, particularly in the context of the 50 percent tariff imposed on India by the US last year. In the light of the 10 percent tariff on exports to US after the US Supreme court verdict striking down Trump’s reciprocal tariffs, India’s exports are expected to do well in FY27. This is positive for growth in FY27.

FPI selling and rupee depreciation

A relevant question from the market perspective is, despite India’s excellent GDP growth numbers, why are the FPIs on a selling spree in India? In CY25 FPIs net sold equity for Rs 1.66 trillion in the Indian market. The sales continue in CY26 till now. Broadly there are two reasons for this: One, foreign portfolio flows have been chasing better returns in markets like South Korea, Taiwan and China where valuations were lower and earnings growth expectations are much higher. For instance, earnings growth in South Korea in CY2025 was 67 percent and Kospi gave 75 percent returns. Similarly in 2025 Taiex gave 27 percent returns supported by 46 percent spurt in TSMC which accounts for 40 percent of Taiwanese market cap. In sharp contrast, India’s earnings growth in FY25 was only 5 percent and for FY26 is estimated at around 10 to 12 percent only for Nifty and slightly higher for the broader market. In brief, despite superior GDP growth India could not deliver decent earnings growth. FIIs sold in India and chased superior returns elsewhere.

Sustained rupee depreciation added to the concerns of the FPIs. The REER (Real Effective Exchange Rate) of the rupee fell 8.1 percent during the period from February 2025 to February 2026. The nominal rupee depreciation was 8.5 percent during FY26. Expectations of further depreciation in the context of rising trade and current account deficits triggered more FPI selling, which, in turn, depreciated the currency further.

External sector vulnerability

Trade deficit and CAD are India’s structural problems. The war in West Asia aggravated this external sector weakness. Brent crude which was trading around $70 before the war spiked to a high of $119 and then cooled to around $95 by 21st April. As I write, the uncertainty on the war front continues with the extension of ceasefire. If there is a deal and Hormuz Strait is opened, crude will decline and the external sector problem will become manageable. On the other hand, if unfortunately, the conflict escalates and crude remains high for an extended period, India’s external sector vulnerability will deteriorate and this will have implications for the stock market, too.

In brief, the implications for the economy and markets will be decided by the duration of the war. Amidst the volatility and uncertainty, the market signals indicate that the war is unlikely to prolong since an extended conflict will be ruinous for all including US and Iran. Let’s hope for the best.