Net sales of listed non-financial companies declined in the quarter ended June 2023. The 3,344 non-finance companies for which financial statements were available for the quarter ended June 2023 collectively show a 2.6 percent year-on-year fall in their net sales.* Sales were also down 4 percent compared to the March 2023 quarter but, this is a seasonal decline seen in almost all June quarters. Demand seems to shrink a bit regularly in the April-June quarter. A year-on-year (y-o-y) comparison does not suffer from such seasonal effects. Our discussion would therefore focus on the y-o-y change.

A fall in sales is indicative of lack of adequate demand or a fall in commodity prices or both. Usually, a fall in demand is reflected in a fall in prices and so, there should be no need to introduce prices separately as an explanatory factor. But commodity prices are driven largely by global economic-political factors and not entirely by local demand-supply movements. Commodity prices can also be wildly volatile at times and their gyrations can heavily influence if not entirely determine the profits of companies in India. To understand whether the fall in sales reflects a fall in demand or a fall in prices, it would be useful to tease out volumes growth from the overall growth in sales.

Economic Outlook presents a unique time-series of price-inflation-adjusted sales growth of listed companies. This has been created by CMIE using appropriate price deflators for each industry on the nominal quarterly y-o-y growth rates. The resultant series reflects volumes growth. It is also called the real growth series while the unadjusted series is the nominal prices growth series.

We find that while nominal sales shrunk y-o-y by 2.6 percent in the June 2023 quarter, real sales grew by 3 percent. This implies that the fall in sales in the June 2023 quarter reflects a fall in commodity prices and not a fall in volumes. Volumes expanded by 3 percent.

Volumes growth has averaged around 3 percent y-o-y in the recent three quarters. They grew by 3.8 percent in the quarter ended December 2022, by 2.4 percent in the quarter ended March 2023 and by 3 percent in the quarter ended June 2023.

This does not seem very impressive given that we are now used to considering real growth of about 6 percent as a given. India’s real GDP averaged at 6.3 percent in the three quarters discussed above. The non-agriculture growth was even higher.

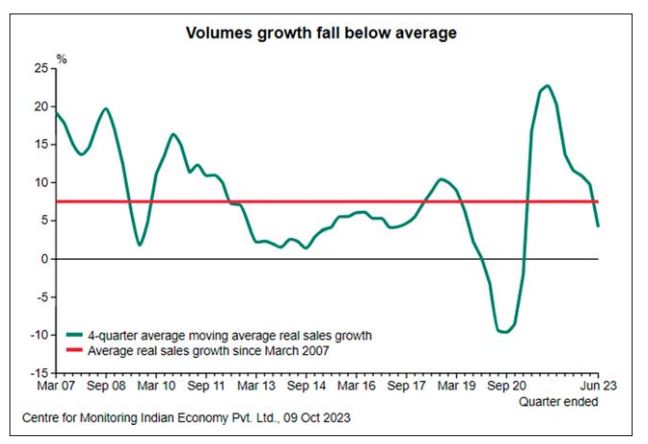

Has growth in real sales, or volumes, of the listed corporate sector slowed down? We answer this question by comparing the corporate sector’s recent growth with its own long-term pre-Covid record. We use the 10-year period from 2010 through 2019. This includes elevated growth rates between 2010 and 2012, a slowdown during 2013 and 2014 followed by steady growth from 2015 through 2017, acceleration in 2018 and then a sharp slowdown in 2019. An average of this period thus includes the various normal ups and downs in the business environment.

The average quarterly y-o-y real sales growth during this period was 6.2 percent. The median was 5.25 percent. There was a period of weak growth from the quarter ended December 2012 through September 2014. Five of the eight quarters during this period saw a growth of less than 3 percent. The average growth during this period was 1.7 percent. Topline growth was hit again in 2019, just before the Covid pandemic. The average quarterly growth during the year was a meagre 0.17 percent with the second half of the year recording a decline.

Compared to the long-term average, the 3 percent average we see in the recent three quarters is a significant slowdown. However, it is not as bad as the low-growth times seen in the past. But the prospects of volumes growth in the coming quarters may not be very good.

Commodity prices may remain elevated given that the world entered into a second war front in October. Foreign trade may also be somewhat impacted with this. This will not help volumes growth but could push up commodity prices.

An equally important factor is that the Indian economy is already slowing down. Real GDP growth is projected to slowdown from 7.8 percent in the quarter ended June 2023 to 5.8 percent in the September quarter, 5.9 percent in the December quarter and 5.7 percent in the March 2024 quarter. Historically, there has been a good positive correlation of 0.789 between real GDP growth and volume growth of listed companies. The projected slowdown in real GDP growth could therefore cast its shadow on the volume growth of non-finance companies.

The Author is MD and CEO of Centre for Monitoring Indian Economy Pvt. Ltd.

*All growth rates reported here are based on a common sample of companies for which data was available for the current and base year periods.