The global market is attempting to end the year on a positive note after a long period of consolidation. Remarkably, the Indian market is providing positive returns when the rest of the world is set to close with negative returns. The ongoing global rally is based on optimism that the worst is over, which we agree, as inflation is forecasted to have peaked. Moderation in geopolitical risks and easing of China’s zero-Covid policy will improve supplies. However, the trajectory of global inflation will continue above the tolerance level, keeping the interest rate high.

Developed economies are at risk of recession in 2023, which can have a ripple effect on the stock market. The domestic market has been resilient despite high valuation and is trading on a best-case scenario, not factoring in the dicey global scenario. Nevertheless, bounce back of the global market will benefit India. However, the high valuations can lead to underperformance. The domestic rally can be tested in the short to medium-term. The global economy is forecasted to improve by the end of 2023, while the stock market is overlooking near-term issues which may arise due to the recession and its consequences.

Weak forecast for G8 economy

Forecasts indicate that the economies of most of the prosperous countries will be fragile in 2023 and 2024. Real GDP growth is expected to plunge in 2023 due to high inflation and interest rates. This is expected to increase unemployment and affect at the ground level. This can affect the rest of the world and the stock market in 2023.

Comparatively better forecast for BRICS economy

However, BRICS (Brazil, Russia, India, China and South Africa) economy is expected to improve in 2023 and 2024, better than G8 (Canada, France, Germany, Italy, Japan, Russia, the USA and the UK). The effect of inflation is forecasted to be lower, and the rate of unemployment will be held steady. Despite this, the overall growth of the economy is expected to be lower than the long-term average.

Overall, it can be presumed that the world economy will be severely affected in 2023 and will take time to revert to the average fiscal strength. World fiscal deficit is expected to be high due to two factors i.e., high government spending to support the weakening economy and fall in tax revenue.

This can affect emerging markets (EMs) more than developed economies due to volatility of currency. However, a key hypothesis in the forecast is that recession is likely to be short lived, being triggered by supply issues and not by fundamental problems. Supplies are presumed to improve due to moderation in geopolitical issues, easing of zero-Covid policy and increase in capacity. The real benefit of rise in supply is yet to be realized but demand has started to reduce.

Domestic stock market will be affected

India’s economy is expected to be the best in the BRICS and EMs category, with high decoupling. GDP is forecasted to grow at an average of 6% in FY24 and FY25. Despite a strong economy, the domestic stock market will be affected as it is vulnerable to the movements in the global financial market. Weak global market will affect the sentiment of foreign investors. Currency movement of EMs is anticipated to be volatile. Currency depreciation means the chances of “importing” external inflation is high. The fiscal position could worsen in the near-term due to high government expenditure and gross capital formation during weak global economy and national election period. DIIs and retail investors were the strong buyers in the market while FIIs were selling. Their patience will be tested in 2023.

High valuation of stock market does not factor these uncertainties

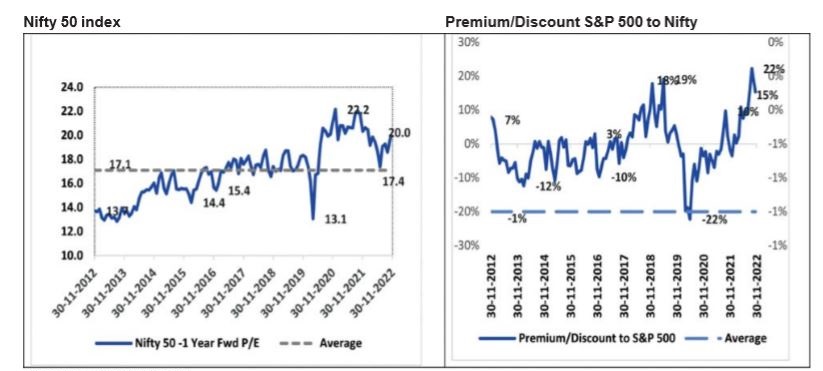

The valuation of the Indian stock market continues to be on the higher side, not reflecting the recessionary risks. The valuation of main indices is high due to the resilient nature of large caps when the rest of the world was consolidating. This was due to limited selling by FIIs in India compared to other EMs and strong buying from retail and DIIs. Going forward, FIIs selling pressure may ease, but attractiveness of the Indian market when compared to the developed and emerging markets will wane because of its premium valuation. For instance, Nifty50 index is trading at 20% premium to S&P 500, historical high level, and 100% premium to MSCI-EM.

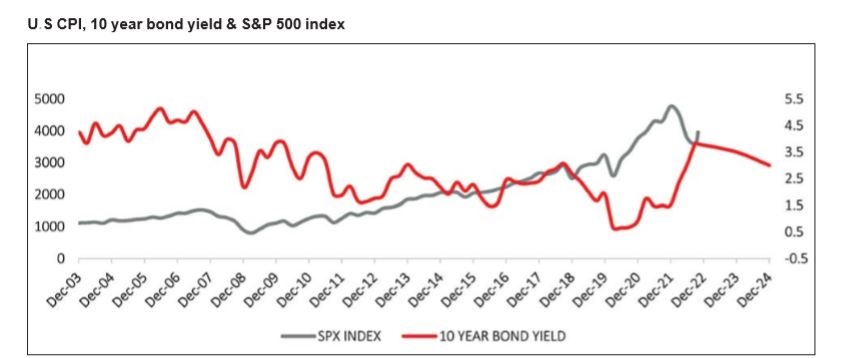

The long-term rally of the stock market was driven by low interest rates. Fed’s effective interest rate went to as low as zero during 2020. The data provides a strong inverse relationship between the two: the lower the interest rate higher is the stock market. Following the Covid correction, US market reached a new high, supported by loose monetary and expansionary fiscal policy. In 2022, S&P 500 corrected by 27% when interest rate was rapidly raised to 3.8% by November 2022. Interest rate cycle is expected to stay line in 2023 and 2024, which will have an effect in the short to medium-term.

Read more articles by Vinod Nair, Head of Research, Geojit.