Peace in West Asia appears to be a growing possibility in the current global scenario. Despite high decibel activity on social media, particularly by President Trump, it is becoming apparent that the US is not inclined toward further military actions. This sentiment has led to expectations that crude oil prices may stabilize between $80 and $90 in the near term, providing relief for India. Such an outcome could mitigate downside risk to FY27 earnings, potentially restoring investor confidence.

A projected decline in India’s EPS of 2% to 4% aligns with recent market trends, as indices have corrected by ~15% over the past two months. Although market targets for 2026 have contracted by 5% to 10%, alongside a 5% reduction in country valuation, there remains a potential upside of 10% to 15% for new investors at current levels.

The year commenced with a Nifty 50 target of 29,150, reflecting expectations of a domestic consumption revival. In light of recent geopolitical developments, preliminary forecasts suggest a revised base target of ~27,000 for the Nifty 50 by December 2026, based on a forward P/E multiple of 19.5x. Sectors expected to outperform include consumption-driven segments such as Automotive and FMCG, as well as growth-oriented areas like Capital Goods, Power, EMS, and Infrastructure. Value opportunities are emerging within the IT sector, while a buy-the-dip approach is recommended for growth-oriented segments such as Private Banks and Real Estate, given current valuations below historical averages.

Q4 Results: Muted expectations with limited near-term impact from war

Global equity markets are navigating a phase of heightened uncertainty, shaped by geopolitical tensions, shifting commodity cycles, and a recalibration of earnings expectations. Over recent days, volatility has been driven primarily by developments in West Asia, particularly concerns around supply disruptions in critical energy routes and INR depreciation, alongside early signals emerging from the Q4FY26 earnings season. While these factors have introduced caution, they have not fundamentally altered the long-term constructive outlook for Indian equities, which continue to benefit from relatively strong macroeconomic fundamentals and improving earnings visibility into FY27-28.

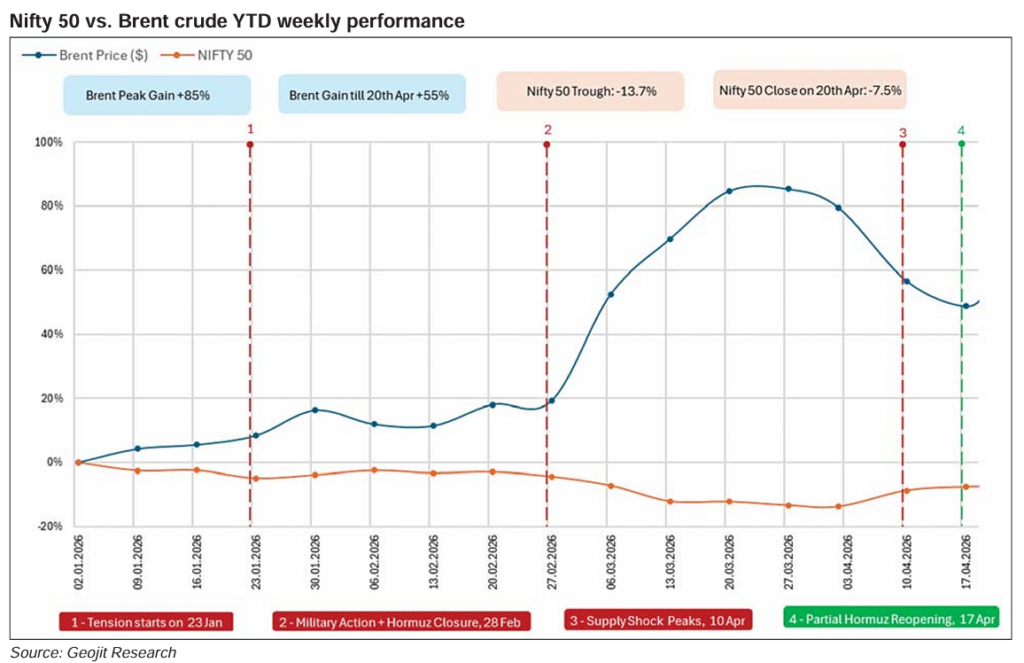

The geopolitical environment has once again emerged as a dominant force influencing financial markets. Tensions involving the US and Iran, coupled with intermittent disruptions around key maritime trade routes, triggered a sharp but temporary spike in crude oil prices. For India, which remains heavily dependent on energy imports, such fluctuations have significant macroeconomic implications. Elevated crude prices tend to exert pressure on inflation, widen the current account deficit, and weaken the domestic currency, thereby impacting investor sentiment. However, recent diplomatic progress and indications of de-escalation have led to a moderation in oil prices, providing a degree of relief to emerging markets. This easing has contributed to a stabilization in bond yields and currency movements, creating a more supportive environment for risk assets, even as the underlying geopolitical risks remain not fully resolved.

Against this global backdrop, India’s domestic economy continues to display resilience. The upward revision of growth forecasts by multilateral institutions reflects confidence in the country’s structural drivers, including consumption, infrastructure development, and digitalization. Policy interventions by the central bank have further reinforced macro stability, particularly through liquidity management and measures aimed at mitigating currency volatility. Although FIIs had been persistent sellers in previous months, driven by relatively elevated valuations and global risk aversion, recent trends suggest a gradual moderation in outflows. This shift has been complemented by sustained domestic institutional participation, which has provided a stabilizing counterbalance during periods of external stress.

Higher impact is expected in Q1FY27.

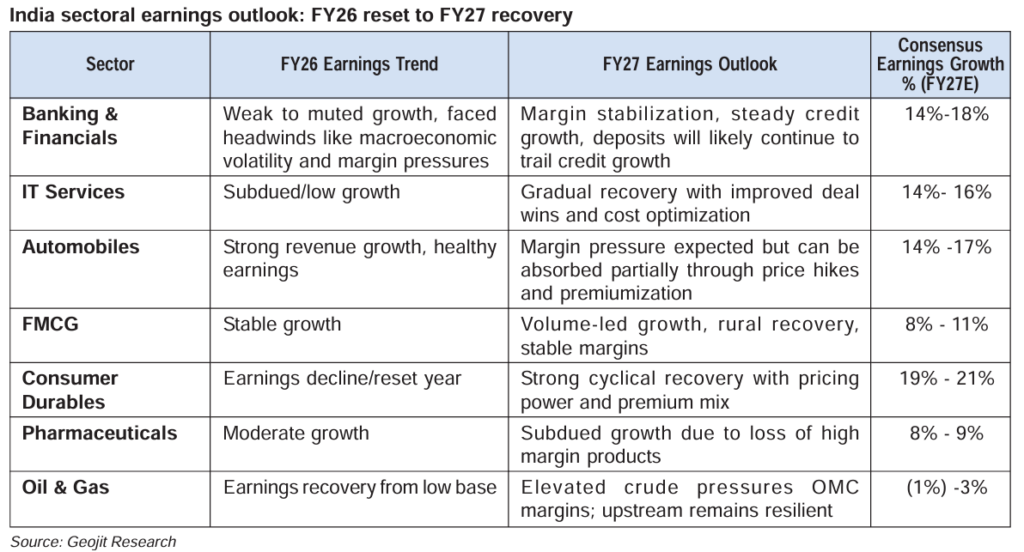

Corporate earnings, however, are currently in a transitional phase. The Q4FY26 earnings season is unfolding against a high base from the previous year, coupled with the lagged effects of tighter financial conditions and geopolitical disruptions that intensified toward the end of the quarter. As a result, the overall earnings picture remains mixed, with certain sectors facing near-term pressures even as underlying fundamentals remain intact. The information technology sector, for instance, continues to grapple with subdued global demand and structural disruptions arising from rapid advancements in artificial intelligence, which are reshaping traditional business models and pricing dynamics. Despite this, the sector’s valuations have corrected meaningfully, potentially offering long-term investment opportunities.

In contrast, sectors such as automobiles and pharmaceuticals demonstrate relatively stable demand dynamics, although they are not entirely insulated from input cost pressures and global uncertainties. Financial institutions are navigating a more complex environment, characterized by steady credit growth but rising funding costs and emerging concerns around asset quality in select segments. Meanwhile, the oil and gas sector reflects the dual impact of fluctuating crude prices, benefiting upstream companies while creating margin pressures for downstream players due to constrained pricing flexibility.

Within the broader consumption landscape, the consumer durables segment provides a particularly illustrative example of the current market dynamics. Following an exceptional performance in FY25, driven largely by an extended and intense summer that significantly boosted demand for cooling products, the sector has entered a phase of normalization in FY26. A relatively milder summer, combined with elevated channel inventories and regulatory changes such as stricter energy efficiency norms, has weighed on both volumes and margins. The sharp increase in key input costs, especially copper, has further compounded these challenges, necessitating price adjustments that have temporarily softened demand.

Despite these near-term headwinds, the structural growth story for consumer durables remains compelling. Rising income levels, increasing urbanization, and a clear shift toward premium and energy-efficient products continue to underpin long-term demand. The transition toward higher-rated appliances, driven by regulatory changes, is expected to enhance product mix and improve realizations over time. As inventory levels normalize and seasonal demand patterns stabilize, the sector is well positioned for a recovery beginning in FY27. Market participants are increasingly recognizing this potential, with companies that are highly established in the branded segment.

The FMCG sector, on the other hand, is witnessing a gradual recovery, supported by improving rural demand and stable input costs. While growth remains steady, the sector faces potential risks from weather-related uncertainties, particularly the outlook for the monsoon, as well as the possibility of rising crude-linked input costs. Nonetheless, the relative defensiveness of the sector continues to make it an attractive allocation during periods of heightened volatility.

Every bit of volatility is an opportunity.

An important development in recent weeks has been the recalibration of market expectations by global brokerages, reflected in target price cuts and earnings downgrades across several sectors. These revisions are largely driven by a combination of higher input costs, weaker global growth assumptions, and increased geopolitical risks. However, the magnitude of these adjustments suggests that a significant portion of the downside may already be reflected in current valuations. India’s premium relative to other emerging markets has moderated, making it more attractive from a relative valuation perspective.

Capital flows remain a critical determinant of market direction. While foreign participation has been subdued, there are early signs of stabilization as valuation comfort improves and macro risks begin to ease. The interplay between foreign and domestic flows will continue to influence liquidity conditions, particularly in the context of global monetary policy and risk sentiment. A sustained period of geopolitical stability, coupled with a favourable earnings trajectory, could act as a catalyst for renewed inflows.

Looking ahead, the trajectory of equity markets will be shaped by the evolution of geopolitical risks, the stability of commodity prices, and the pace of earnings recovery. While short-term volatility is likely to persist, the broader outlook remains constructive, supported by resilient domestic demand and improving corporate profitability. As the market transitions from a phase of earnings downgrades to one of recovery, it is likely to present selective opportunities across sectors that are aligned with structural growth trends.

In essence, the current environment represents a period of adjustment rather than deterioration. The convergence of moderating valuations, stable macroeconomic conditions, and improving earnings visibility creates a foundation for gradual market recovery. For investors, this phase underscores the importance of maintaining a long-term perspective, focusing on fundamentally strong businesses, and navigating volatility with a disciplined approach. Buy in every dip is the best strategy with a 2-3 years view.