We do have a positive view of the domestic equity market. However, the market will have to manage the cyclical hurdles during this year. The proportion of risk-reward is not in favor of investors due to the slowdown in the global economy and domestic earnings. However, the Indian economy is strong enough to handle the issue through decoupling strength with a long-term base target of 6% GDP YoY growth even when global economy is slowing. Still, in the short-term, there are some issues which the Indian stock market will have to address like availability of various other decent investable options, expectations of rapid drop-in interest rate, slowing domestic earnings and premium valuation. Despite this, there are options and strategies to handle this issue by investing in a multi-asset portfolio of equity and non-equity.

Reasonable options in non-equities

The outlook for non-equities appears to be equally as promising for debt, commodities, and real estate. A high-quality AAA bond yield is providing a decent 1-year interest income of 8% to 10%. You can expect up to 12-13% for a BBB graded paper. And, the expectation is that RBI will cut rate during H2CY24, which will lead to an appreciation in the value of the bond. Likewise, we can expect a total return of 10% to 15% (interest + capital appreciation) depending on the credit rating and degree of repo rate by undertaking a low amount of risk compared to equity.

In the case of commodities like Gold, Silver, and Metals, the outlook is mixed with a moderate positive outlook. Caution is likely in the short-term during H1 due to a slowdown in the global economy with an improvement in H2.

Outlook on investing in direct real estate is positive providing a yield of 8% for commercial and national average of 4.5% for residentials. The segment has been providing a CAGR annual appreciation of 10-15% in the last 5 years. The ease of realty investment has been further enhanced with the introduction of Real Estate Investment Trusts (REITs) and fractional ownership of properties, providing investors with accessible avenues to generate passive dividend income and stable long-term wealth generation.

The challenge to sustain the ongoing rally

Since October 2023, globally markets have been on a risk-on rally in anticipation of the peak-out of the interest rate cycle. This is because the monetary policy is expected to reverse in 2024 from hawkish to accommodative. The market is anticipating 4 to 5 Fed rate cuts, 100 to 125bps from current effective rate of 5.33%. The US 10year bond yield in anticipation of this has already declined by more than 100bps to 4.1% in the last 3-months. Hence, there is a concern that the market may have already factored in a substantial portion of the future cuts.

There is likelihood that most adjustments in repo rate will occur later in the year. This is because core consumer inflation is rigid, 3.9% in December 2023, and forecast to be above the long-term target, which is negative to expect deep cuts in rates. Additionally, central banks are expected to continue quantitative tightening to address excess liquidity build-up during the pandemic. Similarly, RBI is also expected to hold rate in the short term due to high food inflation led by uneven monsoon and moderation in rabi production. Basically, high interest cost and slowdown in liquidity don’t present a suitable scenario for equity.

Already rolling on a strong pre-election rally

The current upswing in the domestic market is also driven by the prospect of a pre-election rally, following the favourable mandate for the BJP in the Hindi region state election results on 3rd December 2023. Since then the broad market is up by 10% as of 22nd January 2024. Two months before that India was underperforming. It seems that India is on a strong pre-election rally, underpinned by a favourable economic and political landscape, with foreign funds showing heightened interest in anticipation of the continuation of supportive industrial policies. Well, the actual national election results can be expected by May to June 2024. In the last 1.5 months, the broad market is up by 8%, and in 3 months by 14% as of 20th of January.

El-Nino a dent on food inflation

Domestically, an additional hurdle emerges in the form of heightened food inflation in this El-Nino year. CPI increased to 5.69% for December compared to 4.87% in October 2023. Foodgrain prices have already started to increase due to the below average 2023 monsoon and the ongoing heatwave. The uneven monsoon and irregular distribution of rainfall have affected Kharif’s yield. Rabi production is also forecasted to decline owing to the ongoing heatwave. Importantly, the actual rainfall of next year 2024 monsoon will also play a key role in agriculture and the rural sector, as the reservoir levels are below the long-term average. RBI is also holding a cautious view due to concerns about food inflation. This is having a negative effect on rural market affecting FMCG and the agriculture sector.

Premium Valuation

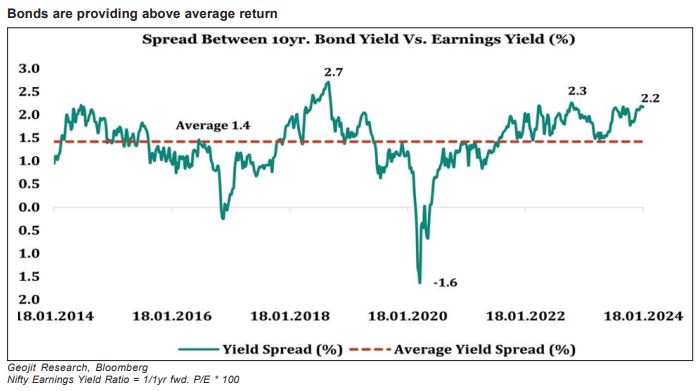

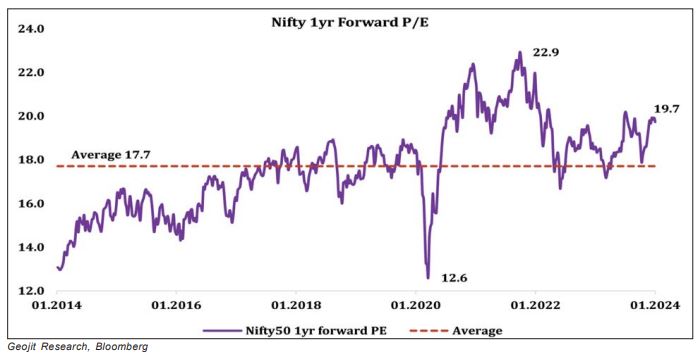

Finally, there’s the aspect of premium valuation. Both India and US markets are trading at a one year forward of 20x (Nifty50 and S&P500), above the long-term average. This is a paradox since the global economy is forecast to slowdown in CY24 and India is likely to do well. The ongoing rally is supported by high domestic inflows, an upside in domestic economic growth, high fiscal spending, quantitative easing, fall in inflation and anticipation of a change in monetary policy.

To sustain the valuation, the earnings growth must be maintained. Based on Q3 results, the earning growth is healthy, but slowdown is visible due to contraction in margin growth and realisation. PAT growth of Nifty 100 large caps was 45% and 25% in Q1 and Q2 and Q3b is expected to normalise to 19%. Nifty 50 EPS growth which is forecast to be 23% in FY24 is expected to witness some downgrade and decline to 14-16% in FY25. A moderation in earnings growth is forecast to lead to a consolidation in future valuation.

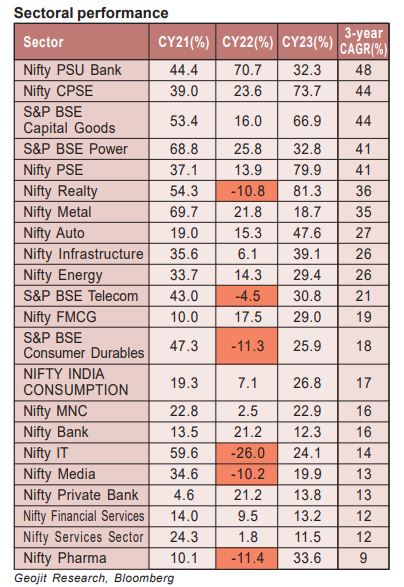

Remedy is to rotate between stocks and sectors

The aforementioned risk factors are anticipated to exert an influence on India’s performance. Currently, we expect a modest return on the main market of 10 to 12% in CY24. It is advised to diversify investment patterns to multi-asset. Strong domestic economic growth and stable high-interest rates will generate decent returns on other assets like debt, real estate, and commodities. It is good to diversify when equities are trading above the long-term average for a prolonged period.

Secondly, within equities, we like large caps compared to mid and small caps. Stock-specific stories continue to drive the mid and small-caps. Rotation in sectors will be the key to generate above-average returns in CY24. We feel that the strong performance of CY22-23 will transfer its momentum to the weak sector during the year. We like IT, Pharma, FMCG, Infra, Private Banks, and Telecom as a safe sector during high volatility.