Since the pandemic-led fall and subsequent upswing, copper prices were largely volatile. In the past two years, the price of red metal has dominated at a greater trajectory and exhibited large fluctuations. Numerous factors including energy crisis, power rationing, geopolitical turmoil, disruption in mine production etc. had influenced the prices during that period. In the first quarter of 2023, the metal’s prices rallied as manufacturing activities in China resumed after authorities scrapped its strict Covid-19 restrictions in January while a widening market surplus of refined copper along with macroeconomic headwinds depressed prices in the second quarter. Rising uncertainties regarding economic growth in the second half of 2023 amid ongoing high inflation and elevated benchmark interest rates from major central banks are expected to weigh the sentiments in copper market.

Lackluster economic numbers from China, the largest consumer of the red metal accounting for more than 50 percent of the total global consumption, signaled a slowdown in its industrial sector and pressurized prices. China’s industrial production grew at a slower pace of 3.5 percent year-on-year in May 2023, compared to a 5.6 percent rise in April, while the manufacturing PMI fell to a five-month low of 48.8 in May of 2023 from 49.2 in April, marking a second straight monthly contraction. China’s factory inflation fell to 4.6 percent in May as faltering demand weighed on a slowing manufacturing sector. Decline in copper imports by the top consumer also indicated a slowdown in demand. China’s customs data showed that its imports of copper fell 4.6 percent in May from a year earlier as weak demand and a fragile economic recovery depressed buying interest while domestic production remained robust.

Meanwhile, the central banks across the globe were aggressively tightening their monetary policy to control inflationary pressure. Yet, inflation in the major economies is still high even after a series of rate hikes, which took their borrowing cost to decade highs. The US Federal Reserve in its June policy meeting kept the interest rates unchanged between 5 – 5.25 percent after ten consecutive rate hikes since the Fed began tightening its monetary policy in March 2022. Now, the Fed has signaled another half percentage point hike this year as the economy is still combating inflation. The European Central Bank increased interest rates for the eighth time in a row in June and hinted at more policy tightening to control excessive inflation. The ECB has now hiked borrowing costs by a total of 4 percentage points in a year, marking its quickest rate hike ever. In the meantime, People’s Bank of China (PBoC) lowered its major lending benchmarks in June, the first time in ten months in an effort to support a faltering economy. The PBoC cut its 5-year loan prime rate to 4.20 percent, the 1-year loan prime rate to 3.55 percent and the medium-term policy loan rate is cut to 2.65 percent. However, the easing was not adequate enough for the ailing property market. The most recent relaxation of monetary policy comes as the second-largest economy in the world’s second-largest economy’s post-pandemic recovery is beginning to lose some of the early momentum it garnered in the first quarter.

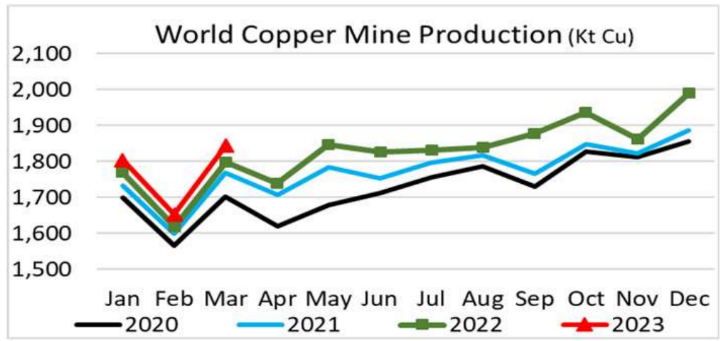

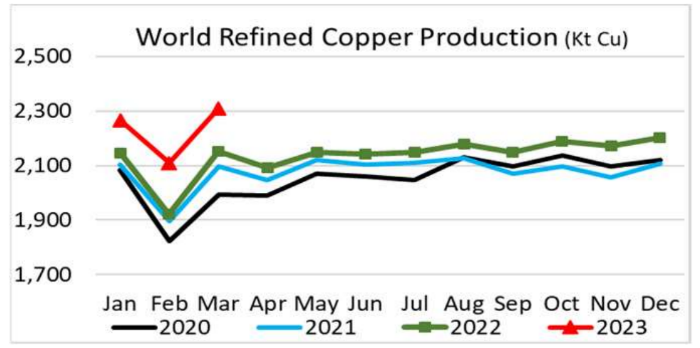

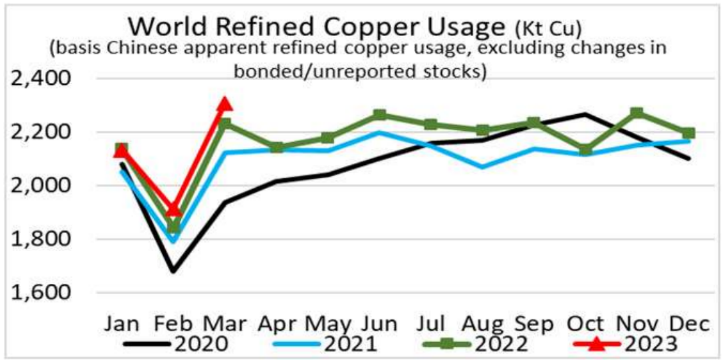

On the supply side, production is seen rising and so is the market surplus. According to the International Copper Study Group (ICSG), the worldwide refined copper market surplus increased to 3,32,000 tonnes in the first quarter of 2023 compared to 8,000 tonnes surplus seen during the same time last year. The global output of the metal increased by over 7.5% year over year to 6.69 million tonnes in the first quarter, while consumption increased by 2.3% to roughly 6.4 million tonnes. During March, the copper market was in a surplus of 2,000 tonnes. According to ICSG, the global refined production rose 9.5% in March to 2.31 million tonnes, while demand grew 20.6% to 2.30 million tonnes. In China, the largest refined copper producer, the output increased 13.5% on year in the first quarter. In Chile, the second-largest producer, production was down 5% due to a fall in primary electrolytic production by 14%. In the Democratic Republic of Congo, production rose about 13% due to ramping up of new solvent extraction and electrowinning plants.

Meanwhile, global secondary production from scrap rose 6.6% to 1.11 million tonne. In the first quarter, demand from all countries, excluding China, is estimated to have slipped 2% on year due to lower usage in Europe, Japan, and the US. Consumption in China grew 5.5%.

The average monthly global copper mine capacity is currently at 2.29 million tonne as against 2.19 million tonne a year ago. In the first quarter, mine utilization rate fell to 77.2% from 78.8% because several mines in Chile, the largest producer of copper from mining, were negatively impacted by operational issues, lower grades, and reduced water supply due to the drought in the central region. The global copper mine capacity rose nearly 4.3% to 6.87 million tonne in the first quarter of 2023 due to additional production at new or expanded mines. Copper stocks at major exchanges rose by 20.5% or 39,021 tonne to 228,526 tonne in April from stocks held at end of December, the ICSG said.

The second half of the year is expected to be much more challenging for the copper prices from demand perspective. The economic growth numbers from major economies have significantly slowed down and is expected to subdue further due to higher borrowing cost. Moreover, elevated inflation level is expected to dent consumer demand in major economies. The metal’s supply is expected to increase at a faster pace considering the increased mine capacity and consistent growth in refined copper production. Additionally, the inventories would pile up due to low demand for metal, maintaining a surplus in the global copper market this year.