The stock market performed well in April and May, a good start for FY24, as anticipated. The broad market was up by 7% as of 15th May. This uptick could have a hiccup in the short-term due to uncertainty in the global market and a lack of legroom for India’s valuation to expand in a downgraded earnings cycle. However, India has restarted to outperform the rest of the world, which should continue during the year as domestic economic growth contrasts with a recessionary world. A long period of consolidation of over 1.5 years has prepared the domestic market to be a hunting ground for quality stocks. Many stocks and sectors are lucrative, while some pockets are still expensive. Hence, stock picking is the key today as the global trend is muted concerning recession and weak banking stocks are questioning the strength of the financial system. Generally, large caps are maintaining their high valuations, but the correction in midcaps and especially the small caps have made them more accommodative for domestic investors to play on. The buyers – both domestic and foreign institutional investors (FIIs) – have come back, and the inflows of domestic investors are expected to continue in 2023, while FII investments may be volatile based on global trends. Identifying the stocks and getting them into your portfolio is the key.

A pleasing ground pitch report

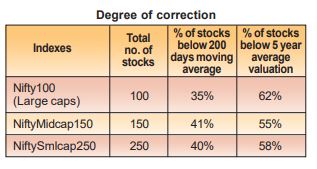

A simple data analysis of trailing P/E and price trends gives a good report. Most stocks in all three categories are currently trading after a deep level of correction. More than 1/3rd of the prices is below 200-day moving average and about less than 2/3rd of the valuation is below the 5 years average. This is a clear sign that the ground is attractive for hunters. That doesn’t mean buying any class of stock or sector and making profit from it. Because some areas may remain soft in the short to medium term due to global uncertainty and slowing demand, affecting the business outlook, and drawing further trouble.

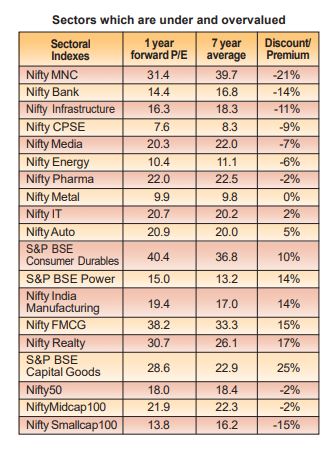

The sectoral picture is mixed, suggesting that half of the value picks are above the long-term valuation and half are below. However, those sectors which are expensive are expected to stay premium in the short to medium-term, being the areas where India is expected to do well, led by sectors like Capital Goods, Manufacturing, Power and Auto. Attractive pockets are MNCs, Infra, Media, Pharma, and small caps. IT and Auto have a mixed valuation, and we have a neutral view. IT is good for long-term investors to nibble on a consistent basis and Auto is expected to do well in the short to medium-term with an upside, especially for commercial vehicle (CV) players. Refer table ‘Sectors which are under and overvalued’.

Factors supporting the rally

The current rally is expected to remain robust in the medium term based on the following factors.

1. Rebound of domestic investors, post-tax harvesting

From December 2022 to March 2023, the Indian stock market experienced notable selling pressure. Then the broad market corrected by -11%. Contributory factors include profit and loss booking by domestic investors excluding mutual fund investors, in which the most damage was done to small caps. Secondly, FIIs also sold in this period as the Indian market was expensive compared to other EMs, however, the amount of selling was moderate compared to the historic trend. The Indian stock market began to rally from March 28th onwards. As the new fiscal year began, domestic investors came back as strong buyers after heavy selling during the last four months in FY23, with an intention to tax harvest. It was to minimize the total tax outflow from capital gains of FY23 by booking losses. This buying tendency is expected to continue, supported by lucrative prices, especially in mid and small caps.

2. Peaking of interest rate

The RBI’s decision to stop interest rate hikes in April is one of the factors that has significantly strengthened the rally. The US Fed’s stance on rate hikes was also confirmed to be similar in May. This is positive for markets as yields moderate, which is the discounting cost while valuing equity. We have noticed that in India, as the RBI announced a pause, market yields reduced to sub 7%, down by about 45bps, providing a boost to domestic equity. The same trend is visible in the US, but there is a concern that the actual global interest rate may stay high for a long time, providing a nominal gain in the short-term. Also, signs of renewed contagion fears among regional US banks are weighing on the global market. And the European Central Bank (ECB) is indicating further rate hikes in the near future. Inflation in India is moving into a tolerable range, while globally it may take some more time. However, a meaningful insight can be expected by the end of fiscal 2024.

3. Fall of commodity prices is a blessing for India

Crude has fallen below $80 from above $100 a year ago. This is positive for India, but negative for the global market, indicating a recession. We need to acknowledge the fact that a significant portion of our industries’ demand is tied to global demand. Domestic industries will benefit from operational gains as their raw material prices linked to crude and metals reduce, but revenue growth may remain muted, limiting overall gains. Additionally, until the government transfers the benefit of the current drop in crude oil prices to the retail consumers, they will not gain from it. Thus, limiting the benefit to the Consumer Price Index.

But the outlook for Indian industry has improved due to the clampdown of global commodity prices. Since April, crude prices have moderated by 13%, and LME Copper and Steel prices by 10%. When the domestic economic environment is stable and commodity prices are reducing, it does provide leeway to Indian corporates due to a cut in operation costs.

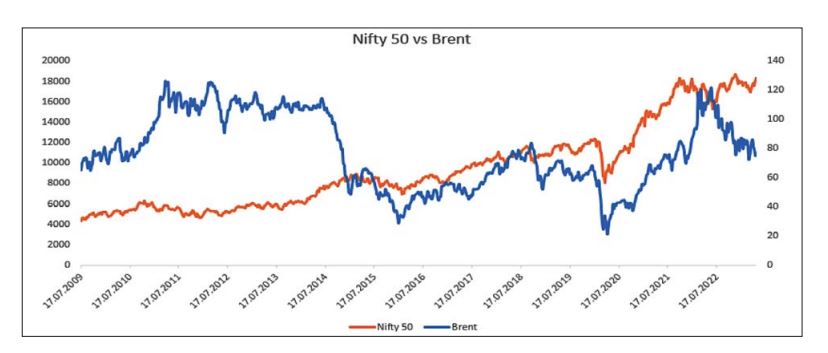

India has a unique relationship with crude. Although the correlation between the Nifty50 index and Brent crude oil is negative at -0.22, based on the last 10 years data, suggesting a tendency to fall together but the relationship is relatively weak because the coefficient is less than 0.5. This is because the stock market has other strong influences like economic, social, and earnings data. Taking an example from recent trends, during the pandemic, the Nifty50 index and Brent crude experienced significant drops. However, Nifty50 recovered faster than Brent, indicating a strong correlation and tendency to outperform. In mid CY 21 to 22, the prices of both peaked and became volatile with a negative bias. However, after the initial hiccups, both are diverging, with crude declining and the Nifty50 rebounding due to an improvement in the profit outlook of India.

4. Return of FIIs

The current market rally is influenced by consistent FII inflows in April and May, driven by lower treasury yields and the weakness in the US Dollar. FIIs have brought Rs.5,700 crore and Rs.17,500 crore in April and till 18th May compared to a net selling of Rs.50,000 crore from January to March 2023. The US 10-year bond yield dropped to 3.6% from the 3-month high of 4.08%. The DXY index, which represents the value of USD compared to a composite of other developed market currencies, has dropped to 103 from a 3-month high of 105.5. India is the clear beneficiary of the drop in commodity prices and bond yields, being the fastest growing economy, inviting inflows. However, we should note that the MoM inflows from FIIs will be volatile in the short[1]term as global economy continues to be fragile.

Investors must carefully assess whether the recent drop in commodity prices is a transitory event or a persistent trend. A prolonged instability in the global economy will inevitably impact the Indian stock market and potentially impede the influx of both domestic and foreign investors. The current optimism is fueled by expectations of a QoQ improvement in corporate margins while the possibility of a global scale of uncertainty could lead to lower-than[1]anticipated revenue growth. Consequently, it is possible that the current forecasted earnings growth of India in FY24 is over estimated, posing challenges to the ongoing rally.

Although challenges persist, there are promising signs within the domestic economy where stocks appear appealing. Sectors and small-cap stocks, in particular, present attractive opportunities for long-term investors. The optimism in the domestic market is driven by expectations of an improved earnings outlook in the coming quarters and the extended consolidation period of over 1.5 years. It has created favorable investment prospects across various stocks and sectors. So, pick your stocks and start accumulating.