by Manu Jacob

Europe was wilfully addicted to Russian energy supplies for decades. Meanwhile, Russia enjoyed its advantage and the viability of supplying its resources to its nearest customer Europe on a large scale. From anywhere else in the world, it would have been tougher and costlier to offer supplies that it provided to Europe. Later on, Russia reiterated its influence on the energy market with its alliance with Organization of the Petroleum Exporting Countries (OPEC).

It was rather a self-inflicted crisis for Europe to wean away from Russian energy resources after the start of Russia – Ukraine war. European Union’s bitter realisation of being highly reliant on its political rival was fairly late. It occurred at a time when the global economy was battling for a complete recovery from Covid’s devastation, and the energy prices were already higher on robust demand. Needless to say, the EU’s decision has not only hurt its economy but also the global economy, as it created an acute energy shortage and accelerated the rise in energy prices in global markets.

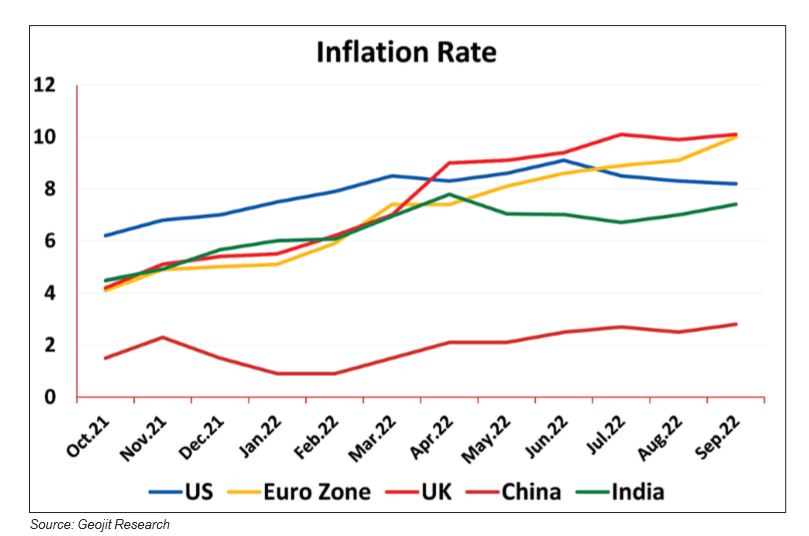

Due to the rally in energy prices, inflation in major economies rose alarmingly. Higher energy costs translated to higher prices from producers to end consumers at a faster pace. Adding to these worries, global economy is braced for another recession after the pandemic as major central banks continue aggressive monetary tightening measures.

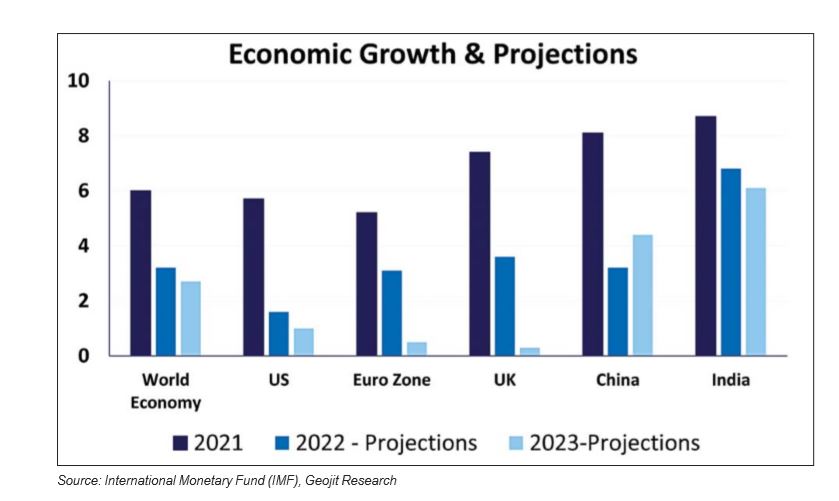

According to International Monetary Fund (IMF), “Global economic activity is experiencing a broad-based and sharper-than-expected slowdown, with inflation higher than seen in several decades. Global growth is forecast to slow from 6.0 percent in 2021 to 3.2 percent in 2022 and 2.7 percent in 2023. This is the weakest growth profile since 2001 except for the global financial crisis and the acute phase of the COVID-19 pandemic.” As per the IMF growth projections, India and China are expected to be the least affected by the ongoing crisis when compared to the advanced economies of the West.

A new, eighth package of sanctions was approved by the Council of the European Union to increase pressure on the Russian government and its economy. The sanction package includes new export restrictions and lays the groundwork for the legal framework required to impose the oil price cap proposed by the Group of Seven (G-7) nations. The European Commission, however, refrained from proposing an immediate gas price cap as the bloc’s members are still divided over the issue. Hence, the commission proposed another set of emergency measures, including joint gas purchases and price correction mechanism in derivative markets.

OPEC+ supply cuts

Despite repeated requests from the US to increase oil production to bolster the world economy, OPEC+, which consists of OPEC and its allies, decided to reduce production by 2 million barrels per day beginning in November during their first face-to-face meeting since 2020 in Vienna. Seemingly, the major oil producers including Saudi Arabia and Russia are aiming to bring oil prices back to above USD100 per barrel.

But in the interim, US President Joe Biden’s administration said in response to OPEC+ decision that it will mandate the release of 10 million barrels from the Strategic Petroleum Reserve (SPR) in November. So far in 2022, the US has released around 165 million barrels of crude oil from the reserves, out of a total proposed 180 million barrels. Additionally, in the run-up to this month’s midterm elections, when OPEC+ output curbs garnered criticism in the US, Biden announced the release of an additional 15 million barrels of oil from the strategic reserve.

Meanwhile, refiners in the world’s largest crude importer China, are expecting a release of up to 15 million tonnes worth of oil product export quotas for the rest of the year to support sagging exports. Such a move would add to global supplies and reduce fuel prices but could support China’s oil demand. Chinese refiners are likely to boost refined oil product exports in the last two months of 2022 and into early 2023 after receiving the biggest allocation from Beijing this year.

Impact on India

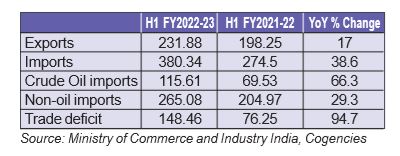

India, the third-largest user of crude oil globally, depends heavily on imports to meet domestic demand. Around 85 percent of the oil used in India is imported. Thus, changes in crude oil prices will have a drastic impact on the country’s import bill. Higher oil prices increase import bills and widen trade deficit. According to data released by India’s commerce ministry, the oil imports increased substantially to USD115.61 billion in the first half of FY2022-23 from USD69.63 billion in the same period in the previous financial year. Subsequently, India’s merchandise trade deficit increased significantly in the first half of FY2022-23 to USD148.46 billion from USD76.25 billion seen in H1 of FY2021-22.

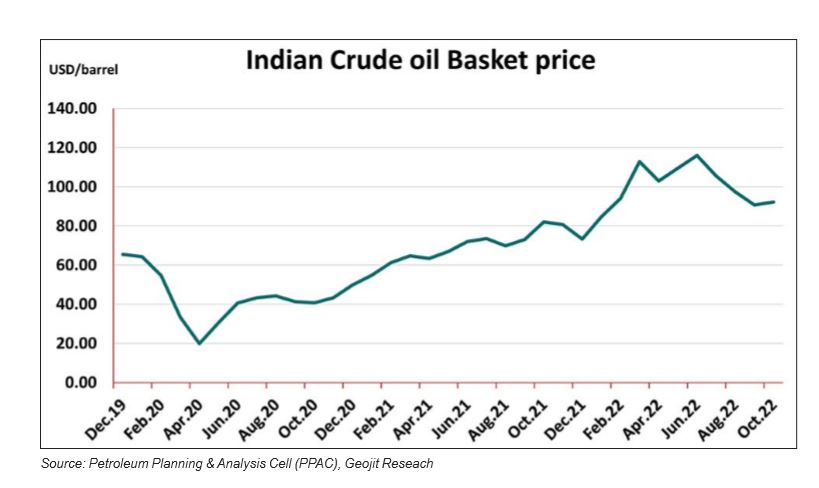

In September, country’s trade deficit decreased to USD25.71 billion from USD27.98 billion the previous month. The trade deficit narrowed on account of a decline in oil imports. The trade deficit was USD22.47 billion in September 2021. India’s crude oil imports decreased 10.3% in September from that of August, presumably as a result of a dip in oil prices. In September, the average price of Indian crude oil fell 6.9% month over month.

Recently, Reserve Bank of India Deputy Governor Michael Patra stated that the country’s current account deficit was projected to stay below 3% of GDP in the current financial year. Meanwhile, The IMF estimates India’s current account deficit to be at 3.5% of GDP. As the current account deficit in India is expected to experience pressure from a persistently high trade deficit, it would weaken the rupee which has recently fallen to all time low.

Lifting the sanctions on Iran will be beneficial for India as it will allow crude oil imports from Iran, helping to diversify nations import portfolio and to lower the prices. India, once Iran’s second-biggest customer, stopped importing Iranian oil in mid-2019 after the Trump administration imposed sanctions on the Persian Gulf. The US and other world powers have been attempting to renegotiate the Iran nuclear agreement, but so far without success. Once the sanctions are repealed, Indian refiners will be able to quickly engage into contracts as they have already started preparations.