Some of the key concepts that regularly seasoned traders’ glance at are premium and discount or contango and backwardation in the case of commodity markets, that augment the view regarding price direction or volatility. In this light, let us look at Straddles.

Understanding a straddle

Straddle is the price that a trader is willing to pay for a bet that the asset will or will not move away from the At-the-Money (ATM) strike. (Straddle is in fact a position that involves simultaneous entry into both call and put, but I would like to view it from a price point of view). A trader will also have to account for trading expenses, while calculating the breakeven, which is the price beyond which the actual profit comes in. Let us assume the trading expenses, which include exchange levies, stamp duties, service tax and brokerage expenses to be nil, so as to focus on the academics of the straddle. Let us take Nifty as the asset. The breakeven point on upper side is arrived at by adding the sum of the premia with the higher strike price, and that for the lower side is arrived at the subtracting the sum of the premia from the lower strike price. Let us assume 17000 CE is bidding for 143 and 17000PE is asking for 157. Hence the upper BE would be 17000+143+157 = 17300, while the lower BE would be 17000-(143+157) =16700.

What does the straddle tell us?

In the example above, the straddle tells us that traders are pricing in the potential for a 600-point trading range. As is the case with any marketplace, the seller of the straddle would want to believe that this is too big a price to pay, while buyer thinks the other way round.

There are a few subtle differences between a straddle trader and the naked trader. For one, the straddle is a volatility trade, and does not give as much importance to the direction, or the pace of direction as much as a naked trader (a single leg trader) would. Secondly, a straddle trader is more informed trader than the naked trader, having given some weightage to VIX, and theta among other factors. Towards this end, the position of a naked trader is similar to a blind bet, but that is not to say that they are all adrenaline junkies. Thirdly, a straddle trade is a slow burn, takes time for all ingredients to mix well, while the outcome of a naked trade does not require much time.

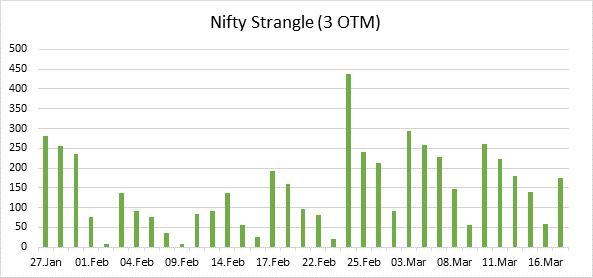

So, while a straddle buyer needs only one of the CE or the PE naked buyer to succeed, such a win needs to be substantial enough, because he/she has paid a substantial insurance by way of a hefty premium (double that of either PE or CE’s premium) for letting the naked buyer bear the risk from unexpected directional move. Thus, while a long straddle is a play on the exuberance of the naked buyer of CEs or PEs, the short straddle becomes a play on the straddle buyer’s judgement of volatility. Interestingly, a naked buyer of CE or PE is seen as an adrenalin junkie, which is not different from how the straddle seller sees the buyer him/herself. A slight improvisation on a straddle is called a strangle. Here, instead of choosing the ATM, out-of-the-money (OTM) strikes are chosen, which takes the game a notch higher, as “time to expiry” becomes all the more crucial, and the breakeven points are set farther away from present market. These make a vivid spectrum of the option arena.

But while they fight it out in the option arena, the stock trader takes home several important information. For one, the coming in and out of a higher straddle/strangle prices, give precious signals towards volatility, the caution or exuberance that a long-term investor could take, or the number of trades or trading range that a short-term trader could attempt.