India seems to be on the verge of overcoming the two biggest hindrances of 2026, the trade war and the crude crisis. Since all these depend on phase-wise implementation and developments to agreements, they continue to be watchful. Hence, though the overall sentiment has improved, the market has upgraded itself to a cautiously optimistic mode.

Other sets of near-term factors which the domestic market will have to overcome are a weak outlook on Q1FY27 results and its drag on Q2, as corporate earnings estimates face downgrade risk with modest growth for FY27. Monsoon has a weak outlook, which may add to the domestic slowdown. An important revival is needed in FIIs’ outlook on India, which continues to be undermined compared to emerging areas like tech-based capex growth. The continued preference for global bond markets over Indian equities and bonds remains a headwind for foreign capital inflows. A reversal of this trend is important for a sustained recovery, though elevated bond yields are likely to persist for the time being. Despite these issues to be handled by India in the rest of the year, we can expect the outlook to have improved, with strong traction noticeable in the broad market led by micro- and mid-caps.

A year that tested every investor’s nerve

If 2025 was the year Indian markets provided a moderate performance, 2026 has been the year that reminded every investor that markets rarely move in straight lines. The year began with India wearing the proud badge of the world’s fastest-growing major economy, with FY26 GDP growth comfortably above 7% and headline inflation at just 2.7%. Yet beneath that strong macro story, storm clouds were already gathering. The West Asian conflict escalated sharply through early 2026, becoming the single most consequential external shock for Indian markets. Crude oil surged from around $67–68 per barrel in FY26 to above $115 in recent months, dramatically widening the import bill, fanning wholesale price inflation to 9.68% in May, and squeezing corporate margins across sectors. The US–China trade war continued to disrupt global supply chains, while a weakening rupee compounded the pain for foreign investors already reassessing their emerging-market allocations.

Foreign money left, but domestic capital held the fort

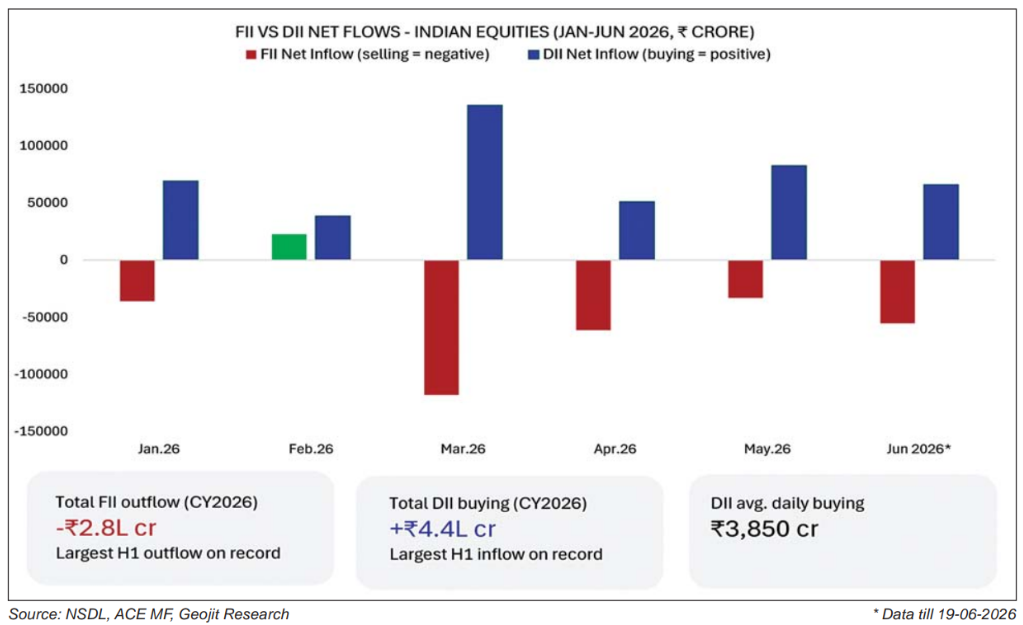

The most visible casualty of this environment was the relentless selling by FIIs. Triggered initially by India’s rich premium valuations relative to emerging-market peers, FII selling continued on India’s poor earnings growth in FY25. FII selling began as early as October 2024 and continued well into mid-2026. By June, to date (19-06-2026), cumulative foreign outflows for the calendar year had crossed nearly Rs 2.8 lakh crore – a staggering withdrawal that in any previous cycle would have caused a far deeper correction. The Nifty 50’s maximum drawdown was around 15% on 2nd April YTD, a remarkable show of resilience, traceable almost entirely to domestic investors. SIP flows held firm. DIIs stepped in as consistent buyers, absorbing billions in supply. This structural shift, from a market driven by foreign flows to one anchored by domestic capital, is perhaps the most significant story of 2025-26. Indian retail investors proved more patient and disciplined than during past downturns, choosing to stay invested rather than panic and exit, other than in a profit-booking mode of February-March 2026.

Geopolitics, oil, and the long shadow of the Fed

Central to the volatility has been the interplay between geopolitics and energy prices. The West Asian conflict triggered fears of sustained disruptions to the Strait of Hormuz shipping lanes. A brief ceasefire in early April sparked a 3.8% single-day gain in the Nifty, only for that optimism to fade as deeper tensions remained unresolved. The US Federal Reserve added another layer of complexity. Under new Chair Kevin Warsh, the Fed adopted a cautious, data-dependent stance, abandoning earlier hints of rate cuts in the face of resilient US employment data and consumer price inflation climbing back to 4.2%. The ECB has already moved with a 25-basis-point hike, and the Bank of Japan followed with a historic rate increase. RBI, while maintaining a broadly supportive domestic liquidity stance, has signalled vigilance.

The monsoon factor

While attention has been riveted on oil prices and central banks, a quieter but equally critical risk is unfolding domestically: the 2026 southwest monsoon. The India Meteorological Department (IMD) has forecast rainfall at 90% of the long-period average, with the probability of a deficient season rising to 60%. A return of El Nino conditions strengthening through September 2026 raises the spectre of lower agricultural output, higher food prices, and weaker rural consumer spending. Sectors with direct rural exposure, namely tractors, two-wheelers, FMCG, fertilisers, and sugar, warrant caution. The saving grace is that reservoir storage remains above last year’s levels and the 10-year average, and food buffer stocks are adequate. While FMCGs are adapting to price hikes, which may moderate impact on corporates.

Signs of stabilisation

As on mid-June 2026, the mood has upgraded to cautiously optimistic, with strong signals of recovery in domestic & global risk appetite. By 19th June, the Sensex had gained around 2.7 % MTD to close at 76,803, marking its second consecutive week of recovery. Encouragingly, FIIs turned net buyers, infusing Rs. 4,859 crore in the cash market in a single day (19th June), raising hopes of a broader revival in foreign inflows after a prolonged period of outflows. Brent crude dipped below $80 per barrel on optimism around US–Iran peace talks in Switzerland, providing immediate relief to inflation expectations and the rupee, which strengthened nearly 1% against the dollar. India also appears to be making progress on trade fronts, with a US–India trade deal inching toward finalisation after tariffs on Indian exports were reduced from around 50% to 18% earlier in the year. The India–UK trade deal has already been signed. Taken together, these developments suggest that the two big macro headwinds of 2026 viz. geopolitical tension and trade uncertainty, may be gradually but meaningfully receding.

Where do investors go from here?

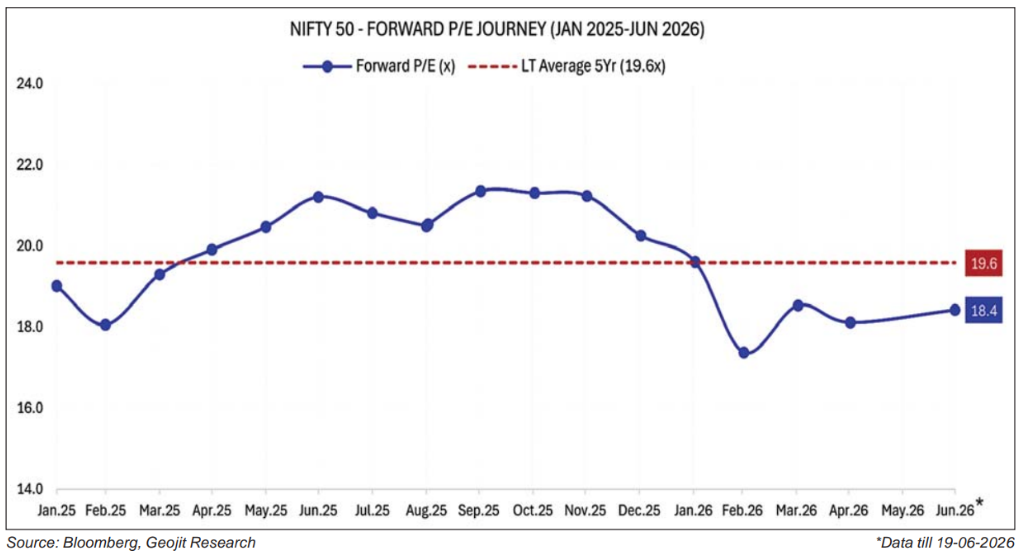

Large-cap stocks, now trading near their long-term valuation averages at 18.4x forward earnings offer a better risk-reward profile than richly priced mid- and small-caps, and are likely to be the first beneficiaries when FII flows resume in earnest. Defensives such as pharmaceuticals, healthcare, and select private-sector banks have shown their value through this consolidation. IT, which has faced pressure from a tighter global interest rate environment, could emerge as an attractive contrarian opportunity for long-term investors. Valuations have become relatively compelling, while the growing adoption of artificial intelligence presents a significant long-term growth opportunity for the sector. Allocating 10–20% of a portfolio to international equities with exposure to AI and new-age technology can help insulate it from purely domestic cycles. For those already invested, a measured and patient stance with a focus on emerging sectors has historically been the most rewarding approach during periods like this.

The path to recovery

Markets rarely recover in a straight line. Key variables to watch include the pace of monsoon progression, the trajectory of crude oil prices, the outcome of US–Iran negotiations, elevated global bond yields, the return of FII flows, and the shape of Q1FY27 corporate earnings, which are likely to absorb the peak impact of the energy shock. Yet, the structural story of India remains intact. A growing economy, a deepening pool of domestic investors, improving trade relationships, reasonable valuations after a long correction, and the gradual easing of global macro headwinds all point to a market in the later stages of base-building. For patient, disciplined investors, the current moment may well look, in hindsight, like the dawn before the next sunrise.