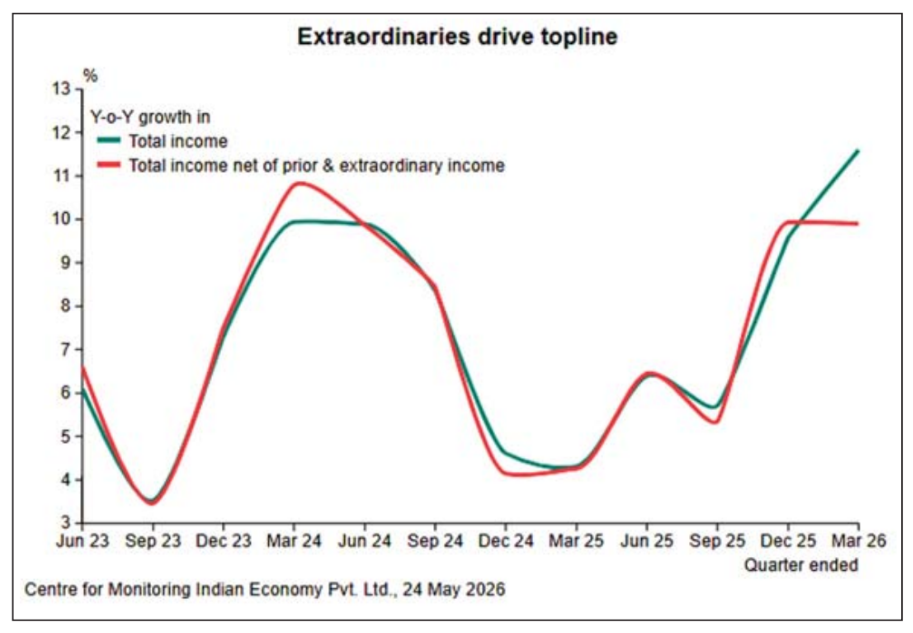

The quarter ended March 2026 saw listed companies consolidate the acceleration in sales growth that was seen in the previous quarter. Total income of listed companies grew by 11.6 percent y-o-y in the March 2026 quarter. This is higher than the 9.6 percent growth seen in the preceding, December 2025 quarter. It is also much higher than the average 6 percent growth recorded in the two quarters earlier and even higher than the 4 percent growth seen in the two quarters before that. While a step-up in top line growth is perceptible in the past two quarters, this is partly driven by extraordinary transactions and price inflation. It is also not widespread in industries.

Total income comprises three broad components net sales, other income and extraordinary income. Of these, net sales grew by 10.1 percent, other income by 7.5 percent and extraordinary income by 211.7 percent. Extraordinary income played a significant role in the acceleration of total income in the March 2026 quarter. This was largely because of provisions written back. The biggest write-back was of the AGR dues by Vodafone. A large write-back was also seen in reversal of impaired financial instruments by Power Finance Corpn.

This little technical detail matters.

Growth in total income after netting out extraordinary income and other income drops to 9.9 percent. This is a full 1.7 percentage points lower than the 11.6 percent growth in total income without making this adjustment.

The 9.9 percent growth in adjusted total income is similar to the 9.9 percent growth seen in a similarly adjusted value in the December 2025 quarter. This adjustment for extraordinary income takes away some of the sheen off the growth seen before the adjustment. Nevertheless, it is still a better growth than the average 7 percent growth seen in the preceding 11 quarters.

The top line growth in the quarter of March 2026 is essentially a story of the growth of the non-finance companies. These companies saw a 13.4 percent growth in total income and a 11.1 percent growth in net sales. Both were the highest growth rates seen in 13 quarters, or more than three years.

In contrast, finance companies saw modest growth rates of 8.2 percent in total income and 7.9 percent in income from operations. Both growth rates are much lower than those recorded in the December 2025 quarter or the average growth rates seen in the past 12 quarters. Growth in total income and income from operations of finance companies has dropped since December 2024. It has also been volatile.

Banking services has taken a big hit. Its total income grew by a negligible 1.4 percent y-o-y in the March 2026 quarter. This is the lowest growth rate in five years. Banking services account for two-thirds of the total total income of finance companies. It, therefore, had a direct impact on the performance of finance companies as a whole.

Within the set of non-finance companies, growth appears to be much higher in the non-financial services companies. Total income of these grew by nearly 22 percent. This is a rather sharp increase. Non-finance services companies were growing at a steady 10 percent y-o-y during 2024-25. The growth fell to about 6 percent and was also volatile in 2025-26. Compared to this recent performance, the 22 percent growth is extraordinary.

But this growth is propped by the communications sector that records a 66 percent increase in total income because of the AGR writeback by Vodafone. Net of this extraordinary transaction, the growth is far more modest. Net sales for example grew by only 11.2 percent.

Net sales growth of non-finance companies paints a more comparable picture and it shows that the manufacturing sector led the growth. While the net sales of all non-finance companies grew by 11.1 percent, that of manufacturing companies grew by 11.5 percent and services grew by a lower, 11.2 percent.

Two industries stand out in the manufacturing sector. Consumer goods recorded a growth of 24.8 percent. This is almost entirely because of the gems and jewellery industry which recorded a growth of 76 percent. This of course, reflects the insatiable demand for gold in India in-spite of a sharp increase in its price.

The second manufacturing industry that performed very well was automobiles. These companies recorded a growth of 26.2 percent in the quarter ended March 2026 after having grown by 24 percent in the December 2025 quarter. All types of automobile manufacturers performed well. Among these, two and three-wheeler manufacturing companies excelled as they grew by 32 percent in March 2026. Net sales of passenger vehicle companies grew by 25 percent.

Machinery companies also reported robust growth in total income. Net sales of these companies grew by 22.8 percent.

Mining companies reported a growth of more than 30 percent. This is largely because of the increase in crude oil prices.

While the March 2026 growth in total income and net sales is better than in the recent past it is partly propped by increase in commodity prices such as gold and crude oil and partly by the extraordinary incomes of some companies. Besides, growth in net sales seems to be genuinely robust only in automobiles and machinery segments. This is a rather narrow base on which the growth rests.