The West Asia crisis continues to impact the market direction. However, the rebound from recent lows signals a gradual shift in sentiment, from fear to cautious optimism, anchored by an intact ceasefire and the market’s growing belief in a contained scenario. Yet the structural risks have not disappeared. Over the past two decades, global crude oil prices have crossed the $100 per barrel mark on four distinct occasions, each driven by geopolitical shocks or a surge in demand. Yet, history shows that such spikes do not always spell disaster – once the dust settles, prices tend to return to their normal range.

In this environment, a staggered investment approach is more appropriate than waiting for complete resolution. Investors expecting a clean, final settlement, may find themselves waiting indefinitely. Even if a diplomatic agreement is reached, the Strait of Hormuz may not reopen fully. The fine print of any nuclear pact between Iran and the West will require months of re-negotiation. What makes a deal more likely, paradoxically, is Iran’s weakened economy — the country urgently needs foreign exchange inflows to stabilise its finances, giving it strong motivation to reach an agreement sooner rather than later.

The Hormuz dependency: India’s energy Achilles’ heel

For India, the stakes in this geopolitical standoff are exceptionally high. The country imports approximately 90% of its energy requirements, a significant share of which transits through the Strait of Hormuz. A prolonged closure of the Strait would be economically catastrophic, disrupting fuel supply chains, pushing up manufacturing costs, and widening the current account deficit.

The government has so far absorbed much of the pressure. The evidence is visible in the April 2026 Wholesale Price Index (WPI) data: India’s wholesale inflation surged to 8.3%, a 42-month high, dramatically overshooting the consensus estimate of 4.4%. The Ministry of Commerce and Industry attributed this spike primarily to a steep rise in mineral oils, crude petroleum, natural gas, and basic metals. WPI inflation in fuel and power alone soared to 24.71% in April from just 1.05% in March — a staggering single-month acceleration. Crude petroleum inflation hit 88.06%, the highest since October 2021.

These figures highlight a key reality: the government and oil marketing companies have been absorbing a significant part of the impact from rising global crude prices to shield consumers. However, this cushion has limits. With fuel prices now being increased in favour of fiscal sustainability, a rise in CPI inflation in the coming months appears increasingly difficult to avoid. The prime minister’s appeal for “economic patriotism”, urging citizens to use public transport, carpool, shift freight to railways, and adopt electric vehicles, reflects the government’s acknowledgment that demand-side conservation, alongside supply-side measures, is now essential.

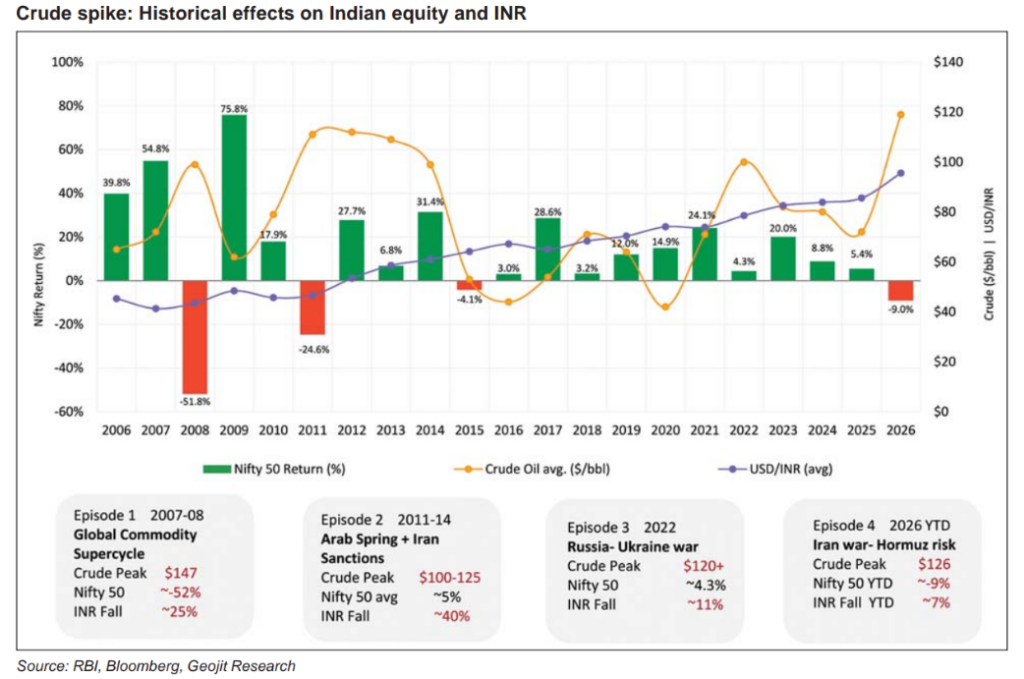

Oil above $100: Four spikes in the last 20 years and how the markets reacted

India and its financial markets have navigated the oil above $100 situation three times before. Each episode offers a different lesson and understanding them is essential for calibrating expectations for 2026.

2008 Global financial crisis: Brent crude touched an all-time high of $147 in July 2008, driven by speculative demand and supply constraints. India’s markets suffered badly — the Nifty fell more than 50%, the rupee depreciated nearly 25%, and the current account deficit widened sharply as capital fled. Yet within six months, oil had collapsed below $40, and the Nifty staged a sharp recovery.

2011–14 Arab Spring and Iran sanctions: This period marked one of the most sustained episodes of external stress on India’s economy. Crude oil prices remained above $100 per barrel for three consecutive years, driving India’s current account deficit to a peak of 4.8% of GDP. Equity markets reflected this strain: the Nifty fell 25% in 2011, amid concerns over the twin deficits, rebounded 28% in 2012 on the back of Fed’s quantitative easing (QE3) optimism and government reform signals, and eventually stabilised as global oil prices corrected below $50.

2022 Russia–Ukraine War: This episode was the most surprising. Brent crude crossed $120, yet the Nifty gained 4% for the year, outperforming global markets. Strong domestic SIP flows absorbed FII selling, corporate earnings held up, and India benefited from discounted Russian crude that materially reduced its energy import bill. The rupee fell only 11% over the year.

2026 YTD — Iran War and Hormuz Risk: The current market environment is more complex than previous cycles. The Nifty 50 is down nearly 9% YTD, FPIs remain net sellers, and unlike 2022, there is no cushion of discounted crude oil. Weak earnings growth over the past two years has pushed valuations closer to long-term averages, while the rupee has depreciated around 7% in the last five months. The Nifty’s recovery in H2 2026 will largely depend on the de-escalation of tensions around the Strait of Hormuz, earnings revival and the timing of a US Fed rate pivot.

One reassuring historical pattern stands out: in all three previous episodes, oil ultimately corrected sharply. Our base case is that Brent crude eventually settles in the $85–90 range as geopolitical risks ease.

Mid & small caps’ remarkable resilience in turbulence

Amidst the large-cap uncertainty, Indian mid- and small-cap indices have delivered a standout performance. The Nifty Smallcap 100 has surged over 20% from its March 2026 lows. The Nifty Midcap 100 has climbed nearly 15%, touching fresh highs in May 2026. The BSE small-cap and mid-cap indices are on course for their best monthly rally in over 12 years—echoing the sharp rebound seen in May 2014.

This rally is powered by three converging forces. First, domestic liquidity remains robust, reflecting the enduring faith of retail investors in India’s growth story. Second, structural themes such as defence indigenisation, manufacturing expansion, infrastructure spending, and digitalisation, continue to create a multi-year growth narrative for emerging Indian businesses. Third, valuations in these segments had corrected meaningfully through 2025, making many stocks genuinely attractive before the recent rebound.

In Q4FY26, the broader market earnings grew by a robust 20%, which is better than consensus estimates. The full impact of GST rationalisation was played out during the quarter and supported consumer discretionary, durable, and staple earnings growth. If the trend continues, it would certainly be positive for the market. However, considering the uncertainty in earnings revival in Q1FY27 and current premium valuation, there is room for near-term consolidation in mid & small cap space. The Nifty Midcap 100 now trades at a price-to-earnings multiple of around 26x 1yr fwd, which is marginally above its 5-year average. The Nifty Smallcap 100 is at 22x — higher than the long-period average but less stretched. For context, the Nifty 50 trades (18x) at a discount to its long-term averages, offering a more balanced risk-reward profile compared to mid- and small caps.

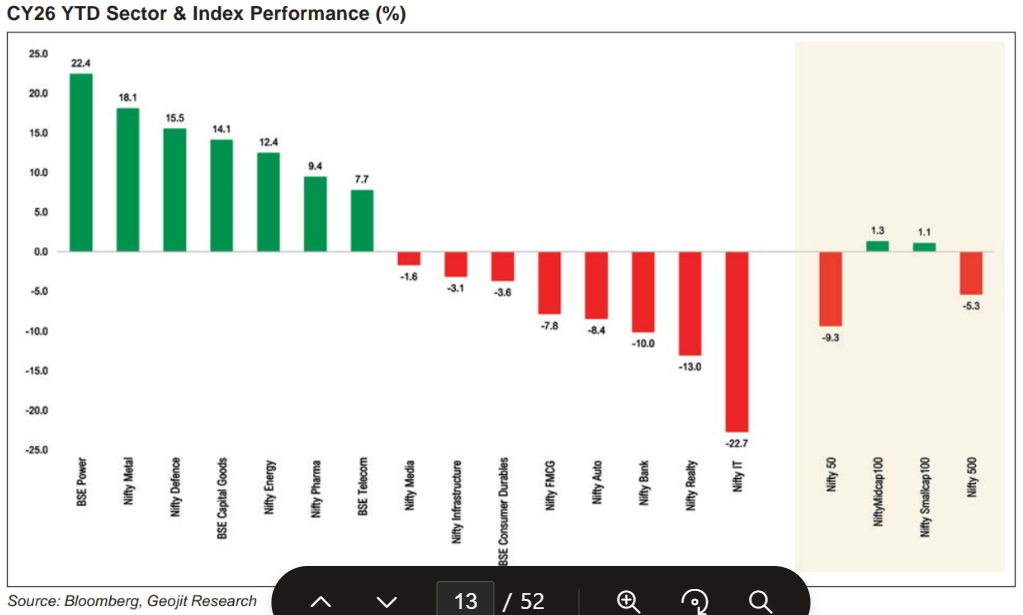

On a year-to-date basis, the Indian equity markets have shown a clear divergence across sectors. Cyclical and growth-oriented segments such as Power, Metal, and Defence have outperformed, driven by strong government infrastructure spending, rising demand for energy, and increased focus on domestic manufacturing and Defence modernization. Similarly, gains in Capital Goods and Energy reflected optimism around industrial growth and infrastructure spending. Defensive sectors such as Pharma and Telecom remained resilient because of consistent demand and improving profitability. Nifty IT was the biggest drag, due to global slowdown fears and pressure on export-driven earnings. Realty underperformed amid valuation concerns, slower urban consumption, and tighter liquidity conditions. Overall, while the Nifty 50 declined (-9.3%), resilience in Midcaps (+1.3%) and Smallcaps (+1.1%) highlighted investor preference for domestic growth stories over global-exposed large caps.

Resilience with eyes wide open

India’s macroeconomic fundamentals are significantly stronger today than during previous oil shock periods. The banking system remains well capitalised, the fiscal deficit is under control, the current account deficit is manageable, and steady SIP inflows continue to provide structural support to equities. However, with crude prices rising sharply and the rupee remaining under pressure, the RBI is expected to stay vigilant on intervention measures while closely monitoring the outlook for inflation and GDP growth.

Currently, the economy is confronting a supply-side shock, not a demand collapse. The Hormuz situation, Iran-US diplomacy, US Fed policy signals, and domestic earnings delivery will each play a defining role in shaping the second half of 2026. For investors, the broader message is clear that India’s long-term growth story remains intact, although near-term visibility remains clouded. In this environment, a staggered and diversified investment approach appears more prudent than waiting for the perfect entry point, as markets continue to reflect cautious optimism despite lingering risks.