After enduring a steep decline in April that dragged crude oil prices to their lowest levels in over four years, the prices have recovered, some losses have been overcome and it stabilized in May. The North Sea’s Brent variant traded in Intercontinental Exchange hit $58.40 per barrel in April, the lowest since March 2021, has now returned to around $65 per barrel in May. This recovery has been largely driven by easing trade tensions between the United States and China, which improved the prospects of fuel demand. The world’s two largest economies, and the top two crude oil consumer nations, agreed to a 90-day truce in their trade dispute, dialling back on reciprocal tariffs that had previously disrupted billions of dollars in global trade flows. Washington consented to reduce duties on Chinese goods to 30% for the 90-day period, while Beijing responded by cutting tariffs on U.S. imports to 10%, down from 125%. Although a blanket 10% U.S. duty on most imports remains in place, the temporary reprieve has boosted market sentiment. Given China’s pivotal role in global oil demand growth, the easing of tensions has offered some relief to the crude market, helping lift prices modestly from multi-year lows.

In the meantime, the potential lifting of U.S. sanctions on Iranian oil exports presents a new downside risk. Iranian crude, often sold at a discount, has been a key feedstock for many independent Chinese refiners. Reintroducing Iranian barrels into the global market could not only undermine the margins of these refineries but also add further downward pressure on global oil prices. President Donald Trump’s administration is pursuing a dual-track approach with Iran, applying maximum economic pressure through sanctions while simultaneously engaging in high-level negotiations over Tehran’s nuclear program.

On the supply side, the market is keeping a close eye on the OPEC+ alliance. The crude oil producer group which includes OPEC members along with Russia and other allies, has decided to gradually unwind its voluntary production cuts, raising the likelihood of a supply increase in the months ahead. The OPEC+ planned to accelerate oil output hikes and could bring back to the market as much as 2.2 million barrels per day by November 2025, as the group’s leader Saudi Arabia seeks to punish some fellow members for producing above quotas.

The uneven compliance across member states, with a handful of countries exceeding their allocated production quotas, has troubled OPEC in assessing market fundamentals. Countries like Iraq, and Kazakhstan has persistently breached the quota has undermined collective credibility. In recent months, the gap between actual output and pledged production targets has widened, reinforcing the perception that quota’s function more as guidelines than strict limits. As oil prices softened and voluntary cuts approached expiration, some members accelerated production to capitalize on higher sales, further deepening the divergence.

Kazakhstan, in particular, has defied OPEC+ pressure to curb output. In May, the country’s crude oil production averaged 1.86 million barrels per day from 1 to 19 May, up 2% from April’s 1.82 million bpd, which itself was a reduction from 1.88 million bpd in March. Despite a modest increase in its May quota to 1.486 million bpd from 1.473 million bpd in April under the latest OPEC+ agreement, Kazakhstan’s output remains well above its assigned target.

Iraq, OPEC’s second-largest producer, has also consistently exceeded its production targets. According to OPEC’s own data, Iraq’s output in April surpassed its quota by approximately 90,000 barrels per day, while the International Energy Agency (IEA) estimates the excess at over 300,000 bpd. In response to growing pressure from OPEC’s core members to offset previous overproduction, Baghdad has pledged to cut exports by 100,000 bpd in May, aiming to reduce shipments to an average of 3.2 million bpd. However, Iraq’s history of unmet compliance commitments cast doubts on the credibility of this latest pledge.

OPEC’s decision to roll out additional voluntary cuts in output level, while aimed at capturing market share, adds uncertainty about future price trends. In contrast, OPEC has revised downward its forecast for oil supply growth from producers outside the OPEC+ framework, including U.S. shale. The group now expects non-OPEC+ supply to increase by 800,000 barrels per day (bpd) in 2025, down from the previous estimate of 900,000 bpd. The decline in crude prices has already started to impact capital expenditures in the sector. U.S. output, while still a major contributor to global supply growth, is now projected to rise by just 300,000 bpd this year, 100,000 bpd less than previously forecast.

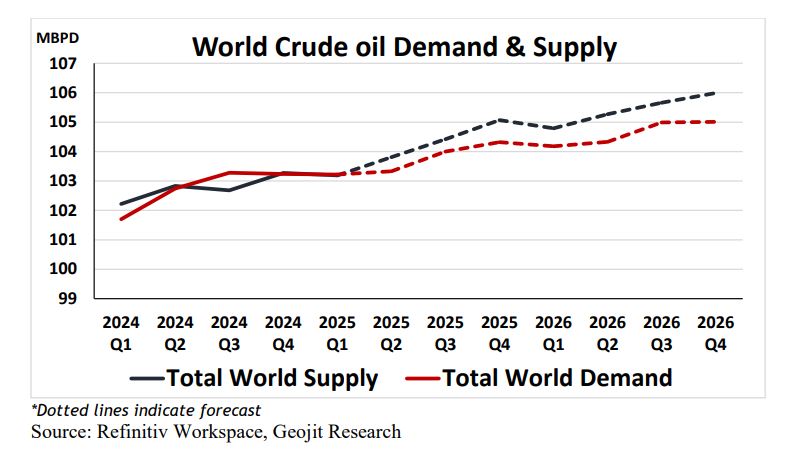

On the demand front, OPEC has kept its forecasts unchanged for 2025 and 2026, following earlier downward revisions triggered by weak first-quarter demand data and lingering trade tariffs. Meanwhile, the International Energy Agency (IEA) has lowered its outlook for demand growth in the second half of 2025. IEA forecasts that the economic headwinds and record-high electric vehicle sales are expected to reduce oil demand growth to 650,000 bpd for the remainder of the year, down from 990,000 bpd recorded in the first quarter. Nevertheless, for 2025, global demand is expected to grow by an average of 740,000 bpd, an upward revision of 20,000 bpd from last month, yet at a slower pace than the projected growth in supply. Consequently, the crude oil market is expected to shift back into surplus for the remainder of this year 2025 and further in 2026.

Looking forward, while the easing of U.S.-China trade tensions has provided necessary support to lift crude oil prices, several factors continue to cast a shadow over the market. These include the possible return of Iranian crude, the gradual rollback of OPEC+ production cuts, and slower-than-expected global demand growth. The sentiments in global crude oil market remains cautiously optimistic yet vulnerable to sudden shifts in geopolitical or macroeconomic scenarios.