The level of uncertainty in the global economy has been elevated during the last five years. The uncertainty began with the Covid-19 shock of 2020, followed by the Russia – Ukraine war in 2021. The inflation shock of 2022 and the conflict in Gaza in 2023 aggravated the uncertainty. The year 2024 ended with the election of the mercurial Donald Trump as the US president and 2025 has begun with Trump’s threat of across-the-board tariff hikes on imports to the US, particularly steeply on China, looming large over global trade, with potential consequences for the global economy.

How is the economic scenario likely to pan out in 2025?

What are the implications for stock markets?

The New Year has begun on a positive note with the end of hostilities in Gaza. This is a positive. However, the uncertainty for the global economy remains elevated since President Trump’s likely economic policy decisions, particularly on tariffs, are not yet clear.

Global economy holding steady

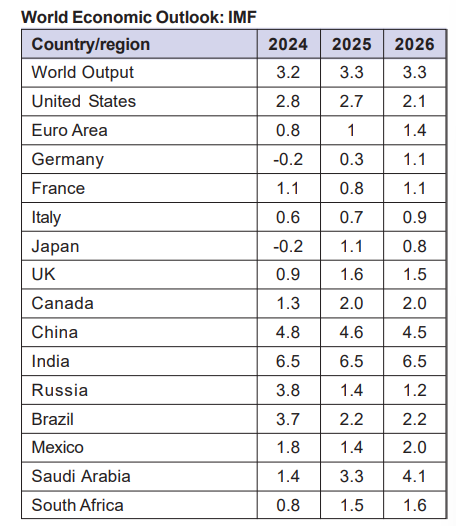

IMF’s 2025 report on the Global Economic Outlook describes the global economy as ‘holding steady.’ The growth projection for World output for 2025 and 2026 is 3.3 percent for both years, mildly up from an estimated 3.2 percent in 2024. Global headline inflation is expected to decline to 4.2 percent in 2025 and to 3.5 percent in 2026. IMF projects ‘solid’ growth of 6.5 percent for India in 2025 and 2026. See the table.

The highlights of the IMF Report are as follows:

• Economic growth is robust in the US. Consumption remains strong, supported by wealth effect and less restrictive monetary policy.

• Growth in the euro area will remain subdued. There are heightened political and policy uncertainty.

• Growth in China is projected at 4.6 percent. Trade policy uncertainty is high and the property market continues to be a drag.

• In India growth will remain solid at 6.5 percent in 2025 and 2026 despite the slowdown.

Stock market trends, particularly in the early months of 2025 are likely to be disproportionally influenced by President Trump’s actions. Trump’s declarations, particularly on tariffs, are inflationary and, therefore, it would be difficult to walk his talk, beyond a point. After the initial days of rhetoric President Trump is likely to settle for negotiations. A trade war will be bad for every country including the US.