Congratulations on landing your first job and earning your first salary! It may sound preachy, but using your hard-earned money wisely is essential. Developing sound financial habits early on can pave the way for long-term financial success.

Here’s a comprehensive personal finance checklist to help you make the most of your first paycheque:

- Create a Budget

Start by listing all your monthly expenses, such as rent, utilities, groceries, car payments, and student loans. Next, set aside funds for savings and investments. Break your expenses into categories, like essential bills, discretionary spending, and savings. This way, you can keep track of where your money goes, prioritise important payments, and ensure you’re saving and investing wisely. - Unsubscribe From Unnecessary Subscriptions

Often, we forget to cancel subscriptions once we no longer need them. You don’t need access to every streaming service and delivery app; a select few are sufficient. While each subscription fee may seem small, they can add up to a significant amount over time. Instead of spending on these subscriptions, consider investing that money in a Systematic Investment Plan to earn returns in the long run. - Eliminate High-Interest Debt

Many fresh graduates start their careers with significant educational debt, often with high-interest rates. This makes repayment challenging and stressful. To manage this better, focus on repaying high-interest loans first to save money in the long run by reducing total interest paid.

Additionally, most new professionals often rely on credit cards to manage expenses. However, mismanaging them can quickly lead to mounting debt and increased financial stress. It is important to remember that credit cards are a form of debt, often with high interest rates. So, first, you need to get familiar with the associated interest rates, fees, and penalties to avoid any costly slip-ups.

Here are some tips for managing credit cards effectively:

• Limit the Number of Cards: Stick to one or two cards with the best terms and benefits to avoid overspending and complicated debt management.

• Pay Off Balances in Full: Try to pay off your balance in full each month to avoid interest charges. If you cannot, aim to pay more than the minimum to reduce the principal faster.

• Set Up Automatic Payments: Avoid missed payments by setting up automatic payments for at least the minimum amount due. This helps maintain a good credit history and avoid late fees.

• Track Spending: Keep track of your credit card spending and set alerts to monitor account activity.

Lastly, consider refinancing or consolidating loans to get a lower interest rate and easier repayment terms. You may want to look into the debt avalanche method for debt repayment. This strategy works by paying down the loan with the highest interest rate first, then the next highest. Many financial gurus prefer this strategy since it results in interest cost savings.

- Establish Financial Goals

Consider setting short-term and long-term financial goals. Whether for purchasing a car, travelling, or saving for a down payment on a home, having specific financial goals will offer direction and encourage you to manage your money wisely. - Start an Emergency Fund

Building an emergency fund is crucial for financial security. Aim to set aside living expenses for at least three to six months in a high-yield savings account or, better yet, liquid funds. These funds will provide a safety net in case any unexpected expenses pop-up and may prevent you from falling into debt. - Contribute to Retirement Savings

It is never too early to start saving for retirement. If your employer offers an EPF or similar retirement plan, consider contributing a percentage of your salary, especially if there is a company match. Additionally, you may want to consider investing in a retirement fund for long-term benefits. Starting early lets you invest more money for a longer time, giving you a better chance to earn substantial returns down the road.

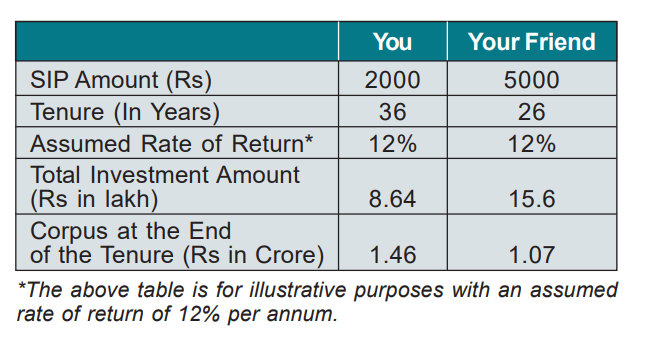

Let’s say you start investing Rs 2000 every month right at age 24. Now, compare that to your friend who waits 10 years and starts investing Rs 5000 monthly at age 34. Both of you aim to retire at 60.

- Invest in Yourself

Warren Buffett, one of the most renowned investors, famously said, “The best investment you can make is an investment in yourself. The more you learn, the more you’ll earn.” So, you might want to take his advice. Further your education, acquire new skills and consistently learn about personal finance and investing. This may enhance your earning potential. Investing in yourself early in your career may lead to higher income and higher returns. - Avoid Lifestyle Inflation

As your income increases, resist the urge to inflate your lifestyle proportionately. Instead, direct any salary increases or bonuses towards your savings, investments, or paying off debt. Living below your means can provide more excellent financial stability and flexibility in the future. - Seek Financial Advice

It is always advisable to consult with a financial advisor to gain personalised insights and guidance on managing your finances. A qualified advisor can offer customised methods for reaching your financial objectives and assist you in navigating difficult financial decisions.

Your first salary marks the start of your financial adventure, and how you handle it now might have a long-term effect on your financial security later.

Adhering to this personal finance checklist can maximise your hard-earned money and build a solid foundation for financial success. Always remember that discipline, consistency, and a long-term outlook are essential for successful money management. With wise financial planning, you may put yourself on a path to reaching your financial objectives and guaranteeing a secure and prosperous future.