Focus on multi-asset allocation strategy

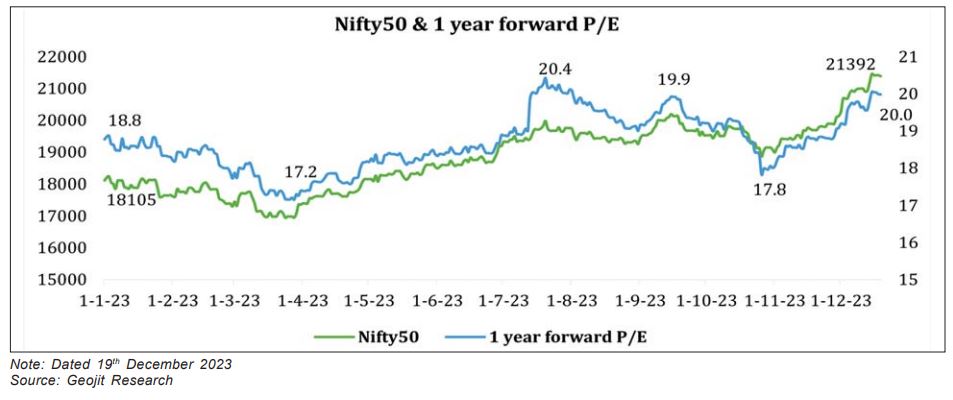

We have a positive view of the CY24 domestic market, forecasting a 10 – 12 percent return on the main index Nifty 50 with a target of 23,600. We value the index at a 1-year forward P/E of 19x, marginally above the long-term average. This is attributed to our anticipation that India will maintain a premium valuation owing to its robust economy, evolving industrial policies, and robust corporate earnings growth. Stabilization of energy prices, including crude oil and gas, is providing support to corporates.

H1CY24 can see a pre-election rally, and the global environment is also supportive due to slight easing of geo-political tension and high interest rate risk. However, the elevated valuations and a slow global economy are likely to limit the degree of gains in equity. But the overall market is good enough to support a multi-asset allocation with a focus on diversification strategy. In addition to equity, we can expect other assets like debt, realty, and commodities to provide decent returns due to a drop in risk, high interest income, and an upside in the domestic economy. In equity, we are more positive on large caps compared to mid and small caps.

CY23: prediction and performance

We had a positive view and suggested a balanced approach to investment. This was due to caution in the short-term, led by hawkish monetary policy (rising interest rate), a premium level of broad market valuation, and FII selling. We suggested value buying as a strategy for investment, focusing on domestic demand-based businesses, and avoiding companies that are highly oriented to the international economy. We believed that India’s current high valuation would fall due to shuffling by foreign investors and a slowdown in domestic earnings growth.

Nevertheless, we foresaw a moderate, positive average return, acknowledging a concern that domestic equities might lag developed and other emerging markets due to their relative affordability and the fact that recessionary risks were factored into their markets.

India consolidated between January to March led by FIIs and retail selling. The valuation contracted and then the domestic market became attractive. And the prospects for the Indian market improved when GDP growth was upgraded. Q4CY22 and Q1CY23 numbers came out better, leading to an upgrade in FY23 GDP growth to 7 percent compared to the 6 percent forecast at the start of 2022.

India’s earnings growth in CY23 has been excellent. The H1FY24 (April – Sept 2023) PAT growth of the Nifty 50 and Nifty 100 constituent stock baskets have been 27 percent and 35 percent, respectively. Surprisingly, the year 2023 has seen a resurgence in domestic inflows, particularly benefiting mid and small-cap segments. As of 19 December, Nifty Smallcap 100 and Nifty Midcap100 have surged by 53 percent and 43.5 percent, respectively, surpassing the Nifty 100’s 18.5 percent increase. Our initial target for Nifty 50 was set at 18,000, subsequently revised to 19,600, with a peak target of 21,000.

Outlook for 2024

- We have a positive view on CY24 and initiate with a base target of 23,600 for Nifty 50 with a peak of 25,000.

- We are positive on H1CY24 in anticipation of pre-election rally, continuation of the growth of India. And expect the decent corporate earnings growth of H1FY24 to continue in H2FY24.

- We are positive on H1 also considering the moderation of global bond yield, leading to the return of FIIs inflow, which for the secondary market was volatile in CY23.

- Overall, we are positive on CY24. However, H2 performance will depend on the outcome of the national election, the final budget, and the continuation of corporate earnings, which we forecast to be stable.

- Corporate earnings are forecast to be marginally moderate in FY25 to 15 percent growth compared to 23 percent in FY24, which is still healthy.

- We like large caps compared to mid and small caps due to elevated valuation, which is about 26 percent above the long-term average.

- We do not forecast any serious issue in the market, as the global economy is forecast to avoid a recession and improve the path in CY25.

- However, key points to ponder are the high valuations of the global and domestic markets at a time when the economy is under a slowdown, which will limit the performance of equity markets. US and India are targeting a one year forward P/E of 19-20x, above the long-term average.

- Domestic issue is that we are in an EL-Nino year, igniting food inflation. Kharif and Rabi production are forecast to be below last year. This is likely to be negative for the rural, agriculture and FMCG sectors. This can affect the rally of CY24. However, the sideeffects on the broad market are likely to be limited to the respective sensitive stocks and sectors and government is taking corrective measures for improving supplies and price control.

In a nutshell, our overall stance on equity for CY24 is positive. However, we anticipate favorable returns on non-equity assets too, by taking low risk, including debt and commodities. High interest income and changes in monetary policy have improved the outlook for debt. In the Indian landscape, current interest income opportunity ranges from 7 percent to 10.9 percent for up to AA credit rating paper (low risk), contingent on the sector and company. With an expected negative trajectory in future yields, the prospect of capital gains in bonds further enhances improving the overall return to approximately up to 15 percent over a 12 – 18month horizon.

The outlook on commodities like metals (gold, silver, and copper) is also positive in anticipation of a weakening in the US dollar, declining interest rate and weakening US economy. It is a good year to consider multi-asset investments as a cut in the Fed rate in CY24-25 is positive for gold, while metals like silver, copper and rare earths are in a positive model. India is pushing for manufacturing and infrastructure, indicating positiveness on commodities. It is a good time to diversify your portfolio when equity is expensive.

Within the equity sphere, our preference lies with large caps due to their relative lower valuation compared to mid and small caps and the expectation of notable outperformance in 2024, fueled by the resurgence of FII inflows. The earnings growth of the Nifty100 index in H1FY24 was 35 percent, while price performance was 15 percent, indicating under valuation.

(Please read our CY24 Strategy Note: http://geoj.it/vW5njt, dated 21st December 2023, for more details.)