The Indian stock market has been consolidating for a long time. The downward trend began in October 2021, which is 1.5 years ago. The market has been contemplating global and domestic havoc since then. During this period, till 18th April 2023, the broad market, like the Nifty500 index, has delivered a negative return of -5% with high volatility. We believe that many of the issues have been factored in and digested, though not entirely, as some implications are being played out. However, we foresee that the Indian market is going through the last phase of consolidation. We understand that FY24 will be better off compared to FY23, especially in the latter part of the year. The biggest risk for the market is a downgrade in earnings, which has started, visibly, with the IT sector sell-off in April 2023 owing to below-expected Q4 results. The risk is that corporate earnings cut can spread to the broad market. However, the plausibility of deep corrections in earnings and the market is muted due to the peaking of yields, moderation in valuations, and stable domestic demand. We foresee the possibility of an upgrade in equity assets in FY24. We advise a staggered increase in the mix of equity assets in the portfolio for a long-term investor during the next one to three quarters.

India’s stock market is in consolidation for one and a half years

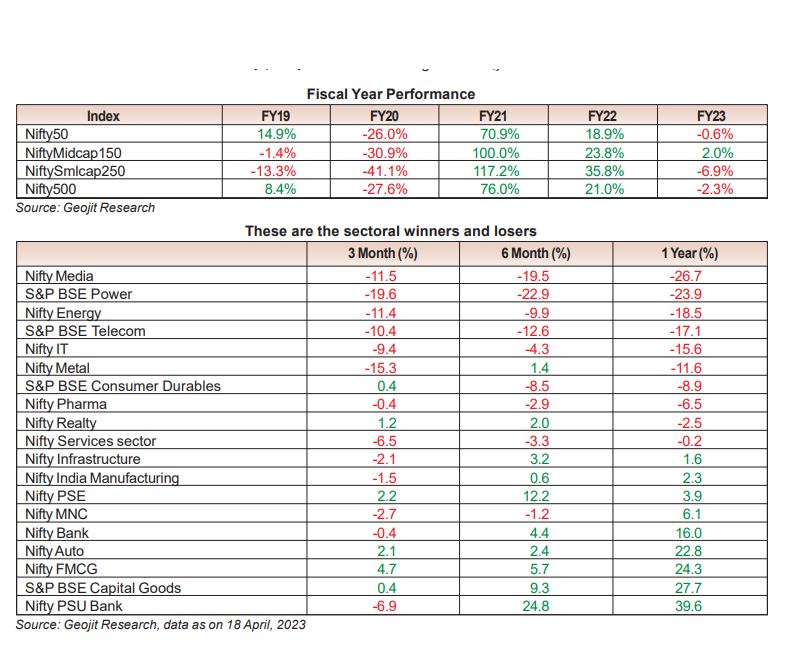

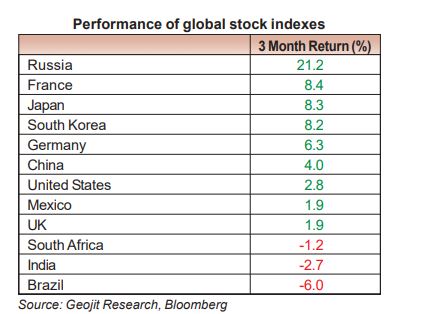

We believe that sooner than later the correction may come to an end. The domestic stock market has had many challenges in the last 18 months, including the post-pandemic tantrums, supply chain constraints, elevated inflation, hawkish monetary policy, the Russia – Ukraine war, the FIIs sell-off, the Adani saga, and finally the recent bankruptcy issues of the US and European banks. In such a chaotic period, the Indian market has done well compared to the rest of the world. However, the broad market is abjectly poor due to sell-off, especially in small and micro caps stocks, as investors’ appetite and liquidity diminished. It was a mixed bag with a negative bias.

The ongoing issues of high interest rates, a fall in confidence in the banking system, high inflation, and recessionary risk will affect the market in the short-term. However, soon, during the fiscal year 2024, we will exit with light at the end of the tunnel. This is because the market yield has peaked, with India’s 10-year government bond yield compressing by 30bps from 7.5% to 7.2% from March to April 2023. This is an early sign of positivity that the risk is peaking out. A drastic downside in risk will happen only when the US yield follows, which is currently inching higher due to the elevated gap between present inflation and the long-term target.

Otherwise, the domestic and global markets have corrected well. The valuation has reduced to a 7-year average, which shrinks the risk of a dire fall in equity assets. Considering the factor that yield and valuation are trending below the long-term average, the equity asset class is in a safe position compared to FY23.

Downgrade in earnings may be the biggest risk for the market

The biggest risk that the market will have to face moving ahead is a further cut in future corporate earnings. That is why even though the valuation has corrected, there is a risk that stock market performance will be delayed in the short-term. For example, India’s corporate earnings growth is forecasted to grow by 18% in FY24. Which we believe is on the higher side due to muted global demand, a loss in pricing power, and global banking sector issue. Earnings may decline by 4% to 6% during the year.

This risk is visible today with the IT sector sell-off in April 2023 due to the lower-than-expected Q4 results. Overall, the IT sector earnings forecast has corrected by 3% to 5%. Because of concerns about the recession, companies are delaying their decision-making process. And during the year, this issue may expand to other industries. However, beyond that, we don’t foresee other big issues. As the markets factor-in this delay, the underperformance of the stock market may end in the next one to two quarters, improving the outlook during the year.

Sectors on which we are optimistic at this juncture are:

Information Technology

Don’t be surprised that in spite of being in a sell-off, the IT sector is a good call to start accumulating for a long-term investor. Volatility will prevail in the short-term due to the risk of downgrades and low earnings growth. But with an eye on 2024–25, it is a valuable asset to own. Due to its high valuation and weak profit growth, which were driven by concerns about a US recession, we had a neutral rating on the IT sector. However, given the consolidation of the IT industry over the past 15 months, we are reviewing whether to upgrade the rating. The valuation has moderated to its long-term average. The optimism stems from the fact that there is renewed demand for cloud and digital transformations in the future. The sector is the core and inevitable partner of future economic growth. The deal pipeline is healthy, providing visibility and strong cashflow. It will lead to a stable dividend policy, buy backs, and acquisition growth.

Infrastructure

The sector continues to remain positive due to early signs of a revival in capex, led by the government’s push for higher spending. We expect infra companies under our coverage to report stable revenue growth with improvements in margins due to moderation in raw material prices and superior execution. The total highway construction up to February 2023 was 8,064km (24.4km / day), and we expect the pace of daily road work construction to pick up pace in FY24 to achieve the ambitious target of 40 km/day. The industry is currently trading at a discount to its long-term average while financial parameters are at historic best.

Pharmaceutical

FY23 was challenging for the pharma sector owing to low growth given the high Covid base, increased raw material costs and price erosion in the US market. This leads to a discount in the valuation of many pharma stocks. For FY24, we expect the growth to be back, and the raw material prices have already begun to cool off. In addition, the Wholesale Price Index (WPI)-linked price hike of essential medicines, new product launches, and the recent spike in Covid are expected to support revenue growth in the domestic market. As the pricing pressure on US generics is expected to persist in FY24, export-oriented pharmaceutical companies may have a modest outlook; however, the moderation in raw material costs and valuation will help to achieve steady performance even in a volatile market.

Capital Goods

We anticipate that businesses operating in the sector will declare favourable outcomes in FY24 owing to substantial inflows of orders and efficient project management. The order pipeline continues to be sturdy across various areas, including power transmission and distribution, water resource management, renewable energy, heavy engineering, railways, transportation, etc. Margins are expected to improve as raw material prices stabilize.

Chemical

The Indian chemical sector has a lot of potential for growth and innovation. Global factors like developing an independent supply chain ex-China and Europe plus one strategy are crucial future drivers. Additionally, a large local market, cost competitiveness, and a pool of talented professionals who provide support are qualitative advantages. Currently, domestic chemical companies in India are prioritizing the introduction of new molecules and processes, backward integration, expanding capacities, and import substitution products, which has helped them win large long-term supply contracts. This has led to a significant re-rating of valuations in the last couple of years, with the average P/E multiple increasing from 15x to above 30x, which is at a premium. Hence, we suggest an accumulation strategy with a stock specific approach.

Market outlook and view

When we started the year, we had a neutral rating on the domestic stock market, assessing high interest rate cycle and recession risk being a problem for the world stock market. It was affecting economic growth and the valuation of the stock market, in which India was the most expensive market. We believed that India would underperform compared to the rest of the world. Year to Date (YTD), the domestic market has been highly volatile, heavily impacted are those stocks and sectors that are highly related to the export market bearing the brunt of economic slowdown.

On a worst-case basis, we foresee a fall of not more than 5% to 7.5% in the domestic market from the current level. While the upside can be in multiples with a 2 to 5 years horizon. Henceforth, we believe that the stock market is in the last phase of the correction. Today, small and microcap stocks are trading at a heavy discount to their historic trend due to lack of activities. The broad market valuations are attractive for a long-term investor. An investor who increases exposure in equity assets during the year will be able to benefit from its outperformance by the end of FY24. The one who harnesses the chaos will be the long-term winner by generating wealth.