The world is heading towards inflation. It is forecasted that high inflation will stay put for the next one to two years. Hyperinflation is not a good situation for the stock markets because it eats into the pockets of households and corporates, diminishing demand. It increases the production cost, affecting profitability. It makes the economy less effective, hitting the outlook of stock markets. However, the stock market being a balancing machine, gravitates towards the segments which are not (or less) affected by inflation. As a result, the equity market always provides an opportunity to increase your wealth through constantly changing portfolio balancing. Today’s crux is to invest in stocks and sectors which are least affected by inflation, have stable revenue outlooks, and are less interest rate sensitive. Such ideas are expected to have a premium valuation and outperform compared to the broad market.

Go for sectors which are less affected by inflation

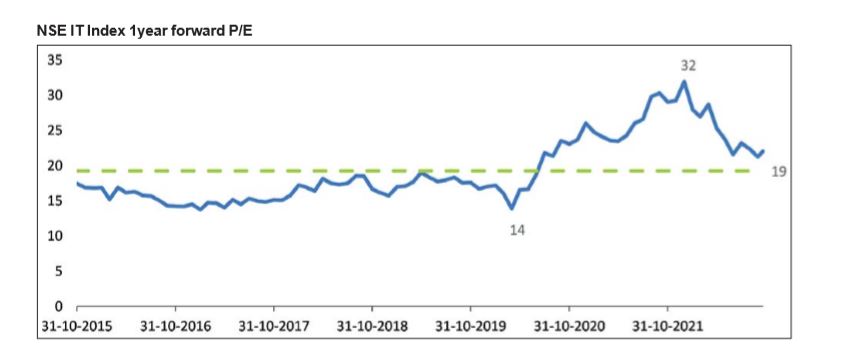

Information Technology

Generally, rising inflation put pressure on the margins of companies. But some of the sectors are protected from inflation. Information sector is one of them. IT companies are trading with a lower beta of 0.80, indicating the defensive nature of the stocks. Moreover, the benchmark index, the NSE IT index, has corrected from its peak by more than 30% before resuming its bargain moves. This resulted in valuations becoming attractive despite macroeconomic headwinds. Top large IT companies reported decent revenue in Q2FY23, which is in line with market expectations. The top-line revenue growth of leading IT companies witnessed double-digit growth, propelled by growth in revenue from cloud, engineering, and digital services. Furthermore, during pre and post covid order backlog has increased as most clients shifted to digitalisation and cloud platforms to better cost optimisation. This will likely accelerate revenue in the near term. Earnings growth in IT is expected to remain strong due to new deal wins and may even benefit from the rupee’s depreciation. On the valuation front, Nifty IT is currently trading at 22x, which is lower than the two-year average forward PE, which is deemed attractive.

Pharma

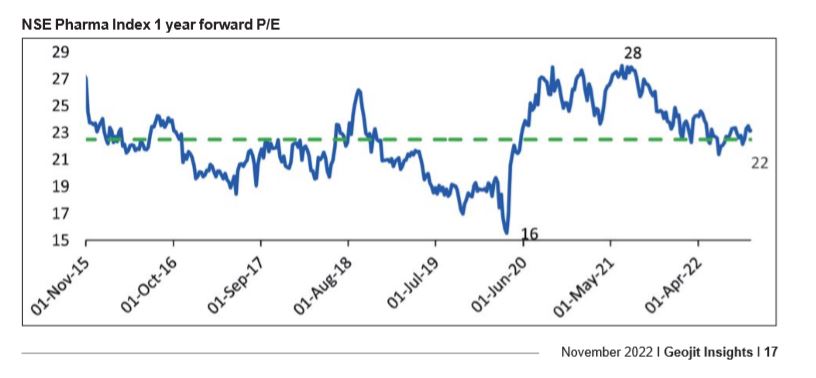

Pharma and healthcare are unlikely to get impacted by discretionary spending cuts. The industry has been facing selling pressure over the last one year due to a rise in fuel and raw material costs. Currently, the raw material prices have started to ease, which will support the margins in the coming quarters.

Complex injectables and respiratory products (especially inhalers) within traditional generics and biosimilars/specialty are likely to be key growth, and margin drivers over the next few years, although challenges related to approvals, market share ramp-up and competition will continue. We expect US price erosion and inflationary pressures to soften. Additionally, pharma companies could leverage their strong balance sheets and inorganic growth. The index is currently trading at a one-year forward P/E of 23x, which is a discount of 8% compared to the 3-year average P/E of 25x. We presume that the pharma sector will have premium valuations due to high healthcare demand in developed economies and the quality of Indian products.

FMCG

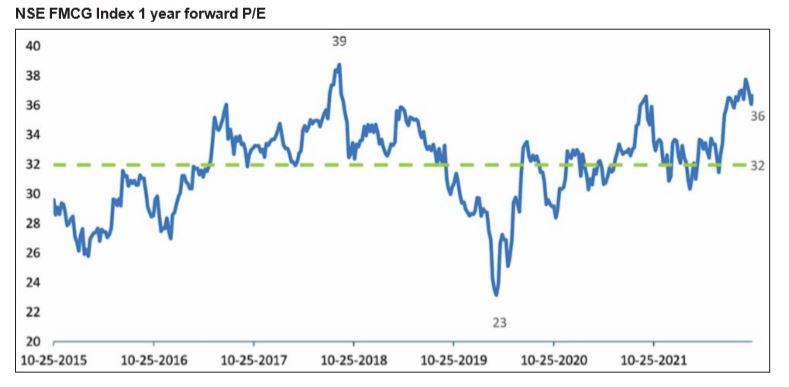

Consumer staple businesses are less affected by inflation due to the essential nature of the products and grammage adjustment formulae. Also, consumers may continue to buy even if the products are charged at higher prices. B2C companies with dominant market share and pricing power, though they may temporarily experience some impact on their margins, are able to pass on cost increases to the customers.

And unless there is a price war, those prices do not significantly decrease to the previous levels even when the prices of the inputs start to stabilise.

These established and mature firms offer low stock price volatility, consistent dividends, and a good hedge to inflationary environment.

Currently, the demand is picking up, supported by a normal monsoon and festive season compared to a decline in prior quarters. At the same time, the correction in input prices in recent months is expected to be reflected in the margins from Q3FY23 onwards. That may be the reason for the consumption-based companies to derive premiums, especially during the economic slowdown. The NSE FMCG index is currently trading at a 1year forward PE of 37x, compared to a 7year average of 32x. We presume that such high valuation will stay, and any correction can be a long-term buying opportunity.

Telecom

The telecom sector’s rapid expansion over the past few years was fuelled by low tariffs, increased accessibility, the introduction of Mobile Number Portability (MNP), the availability of cheap handsets, and growing 3G and 4G coverage. Additionally, the government’s push towards a digital economy also aided the growth. Even though tariffs began to rise in the last year, the telecom sector remained relatively immune to inflation, as affordability remained largely unaffected.

The government allowed the industry to defer their AGR/spectrum dues by four years along with an equity conversion option. Spectrum prices are declining, while for future auctions, governments have increased spectrum life to 30 years. While data consumption post-COVID-19 has increased significantly, with WFH, digital adoption across 4G, home broadband, digital services and payments, the long-term sector outlook remains positive. The industry has taken price hikes on prepaid tariffs by 20-25% in the last year, leading to ARPU moving up. Consolidation in the sector led to few players in the market which helped pass the higher cost to consumers. Going ahead, the telecom sector is very well placed to capitalize on emerging opportunities led by 5G deployment.

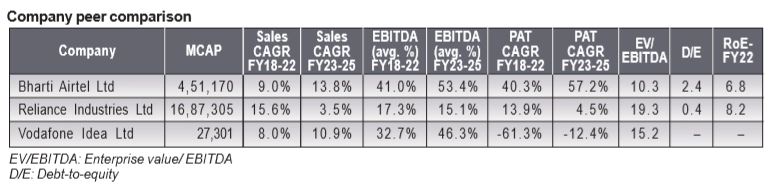

Company peer comparison

Investors should focus on stocks and sectors which are less elastic to high inflation, which is expected to stay high in 2022-23 and affect the profitability of corporates. Secondly, value buying should be the theme because highly valued stocks will not perform during periods of high inflation and high interest rates. Areas in the best position are strong service providers; staple business with a high growth cycle; steady source of raw materials (no supply issue); and low leverage. On a short-to medium-term basis, large caps are a better bet because they are in a better position to handle economic uncertainties. They are at low risk of earnings downgrade compared to Mid and Small caps. We foresee opportunities in sectors like IT, Pharma, FMCG, Telecom, Gas, and Private Banks. Broadly, we like consumption, green initiatives (like solar, wind, hydro power, hydrogen, battery), specialty chemical and manufacturing. The strategy should be to invest in growth stocks that are least impacted by high inflation.