Retirement may not be on your mind, especially if you are young. You might think that there’s still time, and you can think about it later, right? But we can never foresee the future and at times, things don’t work out the way we expect it to.

When it comes to retirement planning, it requires a proactive approach to plan towards your retirement. The earlier you prepare for retirement, the better off you will be in the future. But no matter where you might be in your retirement planning stage — or how much you need to keep aside for other goals, build a strategy that you are financially confident about and stick to it to achieve your retirement goals.

Here are some of the reasons why planning ahead for your retirement is crucial and why you have to be disciplined and stick to your retirement plan.

- Longer life span. Statistics show that life expectancy is increasing steadily. And this can be your very first reason to jump-start your retirement planning. A longer lifespan means you need more retirement funds to live an easy life, especially when you’re no longer working or have a steady income.

- Anticipate financial obstacles. It is good to be positive about one’s future. But it is also pragmatic to anticipate that there may be speed bumps ahead in your life. Therefore, working on your retirement with a robust retirement plan can enable you to overcome any money problems in the future.

- Leave a legacy. As a parent, you want to do more for your family. You wish to leave behind an impact that lasts a lifetime and beyond. And to do so, you need to begin today and get your finances in order so that your heirs stand to benefit from what you sow.

The Right Time to Start Retirement Planning

Ideally, the best time to begin planning for retirement is the day you receive your first pay cheque. So, even though retirement may seem a lifetime away, planning for it in your 20s is not too early.

If you start investing when you are young, you have time on your side to start building good financial habits and benefit from the power of compounding. With every passing year, your investment will generate its own returns — an exceptional wealth building benefit known as compounding.

Notwithstanding your age, the best time to start saving for retirement is now.

A Guide to Calculate Your Retirement Corpus

Here is how you can create your own personalized financial strategy that will help you create your retirement fund.

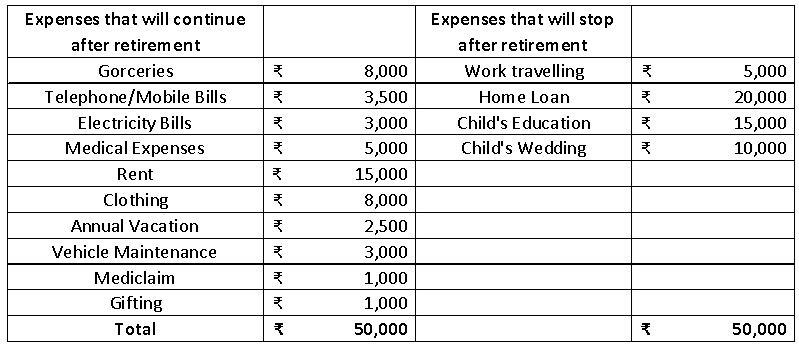

Step 1: Understand your monthly expenses

Note down all your monthly expenses at the moment. Make sure you separate out those that will discontinue upon retirement. It is important to note that there are certain expenses that might increase after retirement (like medical), but they can be balanced out by the expenses that might decline (like rentals, clothing etc.).

So, assuming you are a family man aged 30, you categorize your family’s expenses as follows:

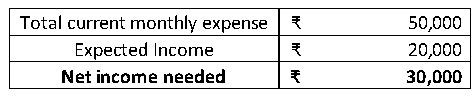

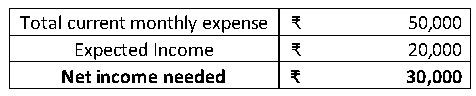

Step 2: Calculate Expected Income After Retirement

Say you have already expected a certain income after retirement, based on the various investments you’ve made in the past years and will continue to make until you are 60.

For the purpose of illustration, let us assume the following amounts in the table below.

Step 3: Calculate the Net Income Needed After Retirement

Since the expected income from different sources could help you cover some of your monthly expenses after retirement, let’s deduct that from your currently monthly expenses. Based on our assumptive calculations so far, the present value of net income needed after retirement would be –

Step 4: Taking Inflation into Account

Now, let’s not forget that whatever you plan to save for your retirement is likely to be affected by inflation.

So, to understand the buying power of your rupee, you need to look into the future value (after 30 years) of your total expenses by including an assumed inflation rate.

Based on compounding formula, the future value of your Rs 30,000 today will be:

As we know, your expenses will not be the same after 30 years and you need to equip yourself to meet such high expense all through the retirement years.

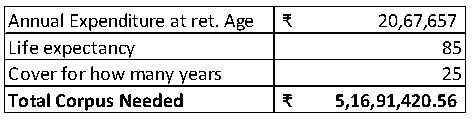

Step 5: Calculate the Retirement Corpus needed at 60

Now assuming that you plan to retire at the age of 60, let’s look at the table below that illustrates the total amount that need to be accumulated on the day you retire, based on 85 years of life expectancy.

Based on assumptions, we have illustrated that you may require ₹5 crores to sustain your current lifestyle even after retirement.

Where Can You Invest for Your Retirement

When deciding on an investment avenue, remember to look into your risk appetite and the risks of the investment vehicle. If your retirement is more than 10 years away, you may consider investing in equities. Equity has the highest potential of earning returns. It carries risks in the short term but that can be mitigated if you stay invested for a long period of time.

You can either choose to make direct equity investments or opt for Mutual Funds.

Mutual funds can not only give you exposure to various asset classes and achieve diversification, but also help appreciate your investments in the long run with good returns.

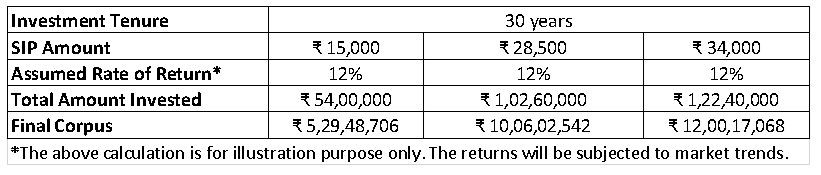

A proven way of investing for your retirement is to opt for the Systematic Investment Plan [SIP] in mutual funds. You can begin a monthly SIP that auto-debits your bank account and invests in mutual fund schemes on a pre-determined date every month.

Investing via Systematic Investment Plan –

- Is lighter on your wallet

- Provides a disciplined approach towards investing

- Averages the cost of your purchases [Rupee Cost Averaging] through market cycles and volatility

- Offers you the benefit of the power of compounding

The following illustration may help you understand how investing via a monthly SIP can help you grow your wealth –

Along with SIPs, one may also include PPF, NPS etc. which helps in creating a balanced portfolio. You may keep higher allocation into equity-oriented investments in initial years and reduce equity exposure as you approach the retirement age.

As an essential part of your financial wellness, retirement planning is crucial. Speaking to a financial advisor specializing in retirement planning can help you save the right amount for yourself and your family. They can help you analyze your expenses, prioritize your financial objectives, and show you how to build a portfolio of assets for a fruitful and comfortable retirement.

Begin planning your retirement today and give yourself the ultimate peace of mind. A good financial advisor can help you manage your assets and protect you against the unexpected so that you never got shot in a downswing. Also remember one thing, do not use the investment set aside for your retirement for other goals. You should have distinct portfolios for each type of goal.