We had forecasted that Indian market would perform better in the second half of 2022. The rally, which started in mid-June is fast and furious. It is supported by the comeback of FIIs and de-risking of global market. For instance, Nifty 50 index rallied by 18.5% from the 52-week low to a high on 18th August. The momentum of the rally, hereon, will highly depend on the change of global risk factors. Currently, the global risk is on an inflection point, as fear of recession is sustained, but equity market has rebounded well. India has been outperforming and is expected to continue its resilience. However, a change in risk will impact the overall performance of the broad market, in the short to medium-term.

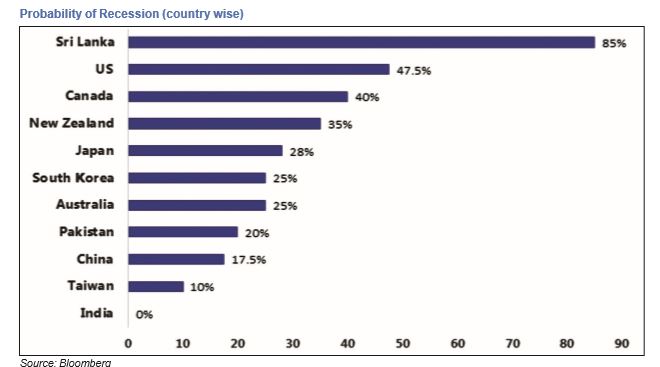

As per the latest Bloomberg survey, the world is at high risk of a recession. Some countries are already facing high degree of economic imbalances. The likelihood of recession risk in 2022-23 is at the highest for developed countries like America and those in Europe. This will have a cascading effect on emerging economies in 2023-24.

The economic growth of India is also expected to slow down, however the risk of recession is zero. It is anticipated that India’s GDP growth will slow from a peak of 8.7% in FY21 to 7.2% in FY23 and 6.5% in FY24. But we need to note that high growth in FY21 was due to low base of FY20. Secondly, the ability of India to grow steadily at a high base when the world economy is consolidating is promising.

However, the risk of downgrade is increasing. IMF in its latest update, stated that the tentative recovery of world economy in 2021 is followed by gloomy 2022 development. CY2022 world GDP growth forecast was cut by 0.4% to 3.2%. RBI has also cut the GDP growth outlook for FY23 from 7.5% to 7.2% in the June 2022 policy. If the trend continues, it will have a rolling effect on the stock market.

Hawkish monetary policy is giving a hiccup to global risk

Globally, monetary policy is expected to be hawkish. Inflation is much above the tolerant level; hence will continue to dictate the mode of the policy. Along with increase in interest rate, the hawkish policy is also reducing the availability of funds in the financial market. This will impact economic growth as suggested by the downgrading of GDP forecast and stock valuation.

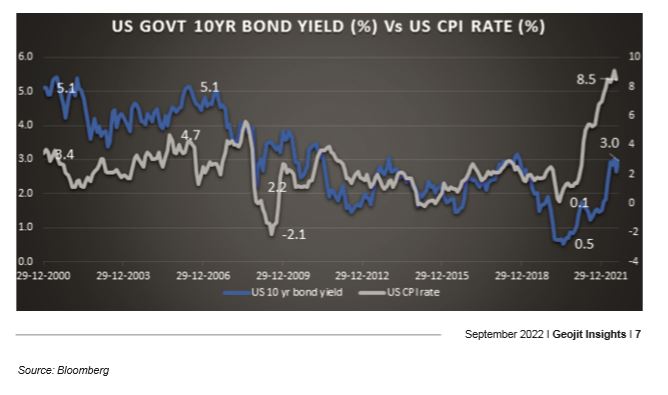

Global bond yield is a good indicator to assess the change in economic risk. Under the current economic circumstances, yields have been increasing due to uncontrollable inflation, rise in geo-political issues and slowing economy. Inflation should subside handsomely, which can prompt the view that monetary policy will change from hawkish to neutral in the near future. But currently, to bring inflation under-control, quantitative tightening is being imposed, leading to rising bond yields and slowing economy, which will have an effect on future corporate earnings growth.

The relationship between yield and inflation is typically in tandem. The gaps between yields and inflation merges in the long-term. These gaps vary due to varied economic reasons. The current factors are the transitory movement from a super easy to tightening monetary policy and supply constraints. This led to elevated inflation while policy is catching up late.

Bond yields are expected to continue its long run by the mid of 2023. The US 10-yr yield is forecasted to increase to 3.50% from current 3.0%. This is reinforced by the fact that Fed rate is expected to increase from current 2.5% to 3.6% by March 2023.

The current big gap between CPI and bond yield reveals that the market is quite confident that inflation will decline quickly and that interest rates will not need to be significantly raised to reach historical levels. To incorporate that, the market may need some time as developed countries in Europe are under the agony of high inflation due to elevated gas and power cost.

Interest rates have opposite effect on valuation

The relationship between interest rate and valuation is inverse. Higher the interest rate, lower will be the valuation and vice versa. When interest rate started to climb and reached a 5-year high like in the US, it had a negative effect on the market leading to a fall in valuation. In India, the 1-year forward P/E corrected from 23x to 10-year average of 17x.

But during the recent rally of the last two months, the valuation has increased to 21.5x, nearing the all-time high. Earnings growth has also corrected. For example, Nifty 50 earnings was forecasted to grow by about 20% in FY23, which has cut to 15% today. Hence, we believe that sustaining the trend is bound to be a challenge in the short to medium-term.

However, the plausibility of further heavy cuts in India’s corporate earnings growth is low due to rapid fall in raw material costs. Also, demand in domestic and global market continues to be buoyant till date. A slowdown in world economy will have a negative impact on sectors like Metals, Mining and Oil. In the short-term, banks will also be impacted due to the hardening of domestic yields leading to a fall in treasury income. However, India will benefit due to improvement in margin and sustenance of demand. Overall, the market will need some time to come back to rally. Stock, sector-specific and balanced equity approach will be the way to handle the short-term volatility.