Wealth is created when you invest during the worst period of the stock market. We are in a corrective phase, which may continue in the short to medium term due to Russia-Ukraine war, China’s supply chain crisis, hyperinflation and hawkish monetary policy. However, we can be certain that this hostile trend will not last for the long term. Because most of these negatives are being factored in the stock prices. Remedial actions and reactions like corrective monetary policy, moderation in war and falling commodity prices have been initiated. Central banks have been behind the curve to initiate a generalised hawkish policy, which can continue in the near-term, impacting performance of equity market. But this is also leading to a sharp fall in commodity prices and economic growth, downgrading future inflation forecast and rising recession risk. Undoubtedly, if this policy continues, it will lead to over combative strategy bringing about a slowdown in economy and a reversal in rate-hiking policy in 2023. The ongoing heavy correction in the stock market is an opportunity in disguise. It is a good time to start increasing exposure in equity from a balanced portfolio which we had suggested at the start of the year.

How far will the market correction go?

We had suggested a conservative view for the 2022 equity market due to the elevated commodity prices, premium valuation and in expectation of economic slowdown. We had anticipated a total correction of up to 10% for the broad market in the light of FIIs selling led by rising bond yields. We had also suggested that you minimize risk by creating a balanced portfolio by reducing the exposure in equity and raising exposure in debt, gold and cash. Nifty 500 index, has corrected by 15% YTD, higher than our expectation due to super hawkish change in monetary policy led by factors like the Russia-Ukraine war and China’s Covid-19 zero tolerance policy.

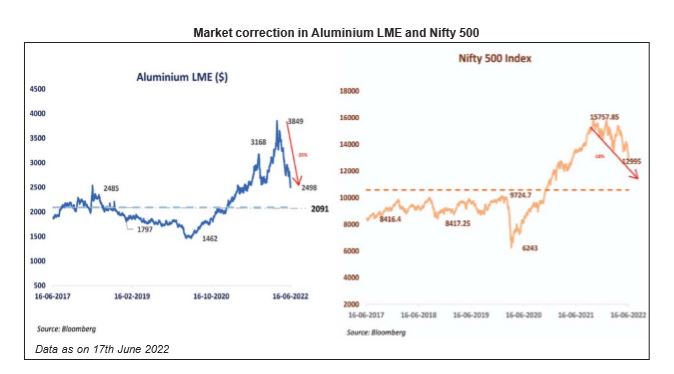

The current situation continues to be slowly evolving with increased dynamics in the volatile stock market. Based on the current assessment, the market can further correct by another 5 to 10% based on developing factors. This hostile period can last for two to nine months but not for a long-time. Because two of the key reasons of hyperinflation, namely war and supply chain issues from China can revert in the future. Commodity prices have started to correct and stock market is factoring in earnings downgrade. For example, aluminum prices (a key industrial product) and broad market like Nifty 500 have corrected by 35% and 18%, from their respective highs.

Valuation is attractive on long-term basis

Earnings downgrades are snowballing in line with the downfall of economic forecast due to elevated commodity prices and aggressive monetary policy. In

main indices like Nifty 50 the earnings have corrected by -7% in the last two months. High inflation has started to pinch the economy as disposable income is falling, affecting demand, especially for discretionary products and services. Due to continuous price hikes many sectors are facing volume and demand pressure.

Actual valuation of Indian and US market

The actual valuation has corrected to marginally below the long-term average. This trend can continue in-line with downgrade in earnings. However, if this trend continues, the valuation will become attractive over the next one to three quarters. Please note that every peak and trough of a market has its own valuation trend and nobody can assess the bottom of this valuation trend.

Will tighter liquidity and interest rates continue to impact valuation?

An assessment of Federal Open Market Committee (FOMC) statement shows a forecast of Fed rate to return to 3.5% in December 2022 and then increase to 4% in H1’2023 before reducing to 3.5% by December 2023. Current effective rate after this week’s hike is 1.75%, suggesting another 175bps hikes in the next four policy meetings, to be held in July, September, November and December 2022. In H1’CY23 we can expect a total hike of 50bps, reducing the possibility of a hawkish rate hike in H2’CY23. As market factors in this phase of rate hike in bond yields, we can presume that we are in the last phase of consolidation, which can end during the year. US 10-year bond yield had peaked to 3.5% and is currently at 3.2%, but can increase to 4% to 4.5% in the future, depending on the developments.

Be smart, invest more than regular amount to get attractive returns

This is not the time to be greedy but to be smart and rationale. Invest a larger than regular amount on a consistent basis over the next three to nine months, with a view that the worst will be factored in between. We had suggested investing in large caps, which can be continued in the short to medium-term because the performance of equity may be polarized in the next few years. However, it is fair to increase exposure in high quality mid and small caps due to overwhelming fall in price and valuations. Defensives and value stocks will perform the best in the broad market. The best sectors will be FMCG, Consumption, Auto, Telecom, IT (large caps), Pharma (large caps) and Green Energy. A rationale investor will be able to generate alpha returns even in a volatile market with a proactive and structured portfolio.