by Manu Jacob

Energy commodities witnessed a surge in volatility in the first half of 2022. Market players largely found themselves in a dilemma as it was challenging to place bets in the volatile market conditions that arose over the past few months. The demand-supply imbalance in the crude oil and natural gas market following the Russian invasion of Ukraine made the prices jittery. Fears of further supply disruption due to tight supplies in the world market lifted the crude oil and natural gas prices to yearly highs. Higher energy prices and economic uncertainties have accelerated inflation in major economies. Adding to these worries, European Union’s sanctions on Russian energy exports led to uncertainties in the energy market. Europe, Russia’s largest energy client, is caught in the middle of the Ukraine conflict. If Europe’s aim to wean itself from Russian energy exports succeeds, the world economy will face an acute energy catastrophe.

Inflation rates in major economies have accelerated as a result of rising fuel prices. In May 2022, the annualised rate of inflation in the United States reached 8.6 percent, the highest in 40 years. In May, the inflation rate in the Eurozone reached a new high of 8.1 percent, owing to rising oil and gas prices.

To combat inflation, central banks around the world began to withdraw fiscal and monetary policy accommodation. In May and June, the Federal Open Market Committee (FOMC) raised interest rates by 50 basis points and 75 basis points, respectively. Interest rates are now between 1.5 and 1.75 percent. Federal Reserve Chairman Jerome Powell hinted at another raise of 50 or 75 basis points in July.

Meanwhile, in its recent Worldwide Economic Prospects report, the World Bank lowered its global growth prediction for 2022 to 2.9 percent, which is much lower than the 4.1 percent expected in January. The economic growth is expected to languish at this pace in 2023 and 2024 as well if the Ukraine crisis continues to disrupt business activities, investment and trade.

The energy crisis surfaced in the global market during the second half of 2021. It only worsened in 2022 in the wake of the Russia-Ukraine crisis that sabotaged the trade environment, lifting the prices. The West Texas Intermediate light sweet crude oil futures traded in New York Mercantile Exchange (NYMEX) gained around 45 percent in first half of 2022, meanwhile North sea’s Brent variant Intercontinental Exchange (ICE) gained around 48 percent.

During April and May, many European buyers stopped importing Russian oil, but the Russian owned refineries in Europe ramped up their purchases. When the EU bloc announced its sixth set of sanctions on Russian oil imports and its attempt to reduce dependency on Russian oil by 90 percent by the end of 2022, it weighed on the bloc’s members to find alternative fuel sources within a limited timeline. European buyers increased oil imports from West Africa and Latin America to pare the shortage while Russia managed to divert some of its oil exports to India and China. However, in the longer-term, it would be challenging for Russia to divert much of its oil flow to eastern buyers due to inadequate spare capacity of pipelines to the Pacific and China and the inability to divert seaborne trade to Asian destinations from Europe.

The oil output from the producers’ group known as OPEC+ continues to undershot the targeted production levels. Although the US continues to persuade the producers’ group to utilize their spare capacity to balance the market, the cartel even failed to meet the targeted production levels. With a six-year partnership, Russia has remained a crucial supporter of OPEC, helping to amplify the group’s influence in the market and drive prices to more favourable levels. During the short price war in April 2020, the perils of a rupture in relations between Russia and Saudi Arabia were demonstrated.

However, for the Russian sellers seeking a share of the global market, the trade environment is becoming increasingly tough. They need to seek smaller group of potential customers who are unconcerned about western sanctions. These buyers will also look for steep discounts on global oil price benchmarks. But fortunately for Russian producers, the oil prices firmly trade above USD100, and the price of Russian crude has stayed in or above the USD60–70 range even after discounts and additional shipping expenses.

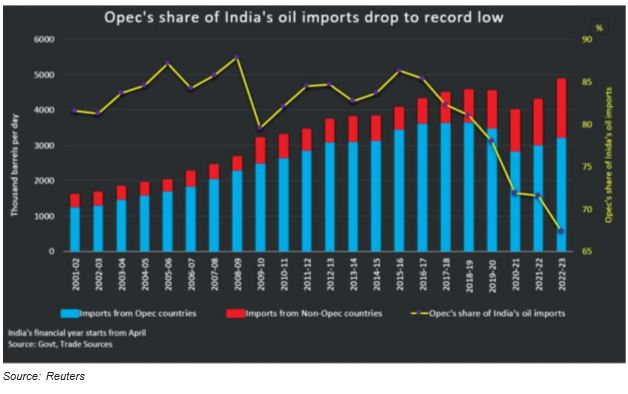

In May 2022, Russia overtook Saudi Arabia as India’s second-largest oil supplier, putting Saudi Arabia into the third position but still trailing Iraq, which remains the top supplier. Indian refiners received over 819,000 barrels per day of Russian oil in May, the highest monthly volume so far, compared to roughly 277,00 in April. Many oil importers have avoided dealing with Russia as a result of Western sanctions imposed in response to its invasion of Ukraine, driving spot prices for Russian crude to record lows compared to other grades. This allowed Indian refiners, who previously avoided buying Russian oil due to high freight costs, to take advantage of low-cost crude. In May, Russian oil accounted for roughly 16.5 percent of India’s total oil imports, while the Middle East’s share fell to about 59.5 percent. At the same time, African oil accounted for 11.5 percent of India’s crude imports, up from 5.9 percent in April. China’s imports of Russian oil reached a new high of 8.42 million metric tonnes in May, up 55 percent from the previous year. That’s equivalent to around 1.98 million barrels per day, up from 1.59 million barrels per day in April. As a result of the increase in imports, Russia has surpassed Saudi Arabia as China’s leading oil supplier.

In the case of natural gas, the spread between the US domestic prices and gas prices in Europe and Asia is extremely wide. Due to a serious shortage, the European benchmark prices were particularly volatile during last winter. In June, natural gas futures on the NYMEX rose to an almost 14-year high to USD9.664 per mmBtu before falling to approximately 6.400 per mmBtu. Whereas a key European benchmark Dutch TTF natural gas futures in ICE hovered near USD38 per mmBtu.

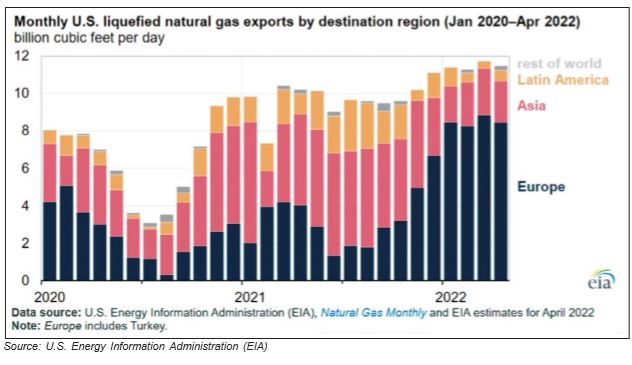

Since Russia’s invasion of Ukraine, Europe’s gas supply has been jeopardised. While there appears to be no immediate danger of a full shutdown of Russian supplies to the region, overall Russian shipments have decreased. Europe has increased imports of liquified natural gas from US. According to Energy Information Administration (EIA), the US shipped 74 percent of its liquefied natural gas to Europe in the first four months of 2022, compared to an annual average of 34 percent last year. In June, an explosion at Freeport LNG’s liquefaction facility and export terminals sent European gas prices skyrocketing once more, underscoring the market’s fragility and the extent to which it remains vulnerable to any supply disruption. Considering this scenario, Europe’s top Russian gas buyers scrambled to secure other fuel supplies and could burn more coal to cope with reduced gas inflows from Russia. Germany, Italy, Austria, and the Netherlands have all indicated that coal-fired power plants could help the continent get through a crisis.