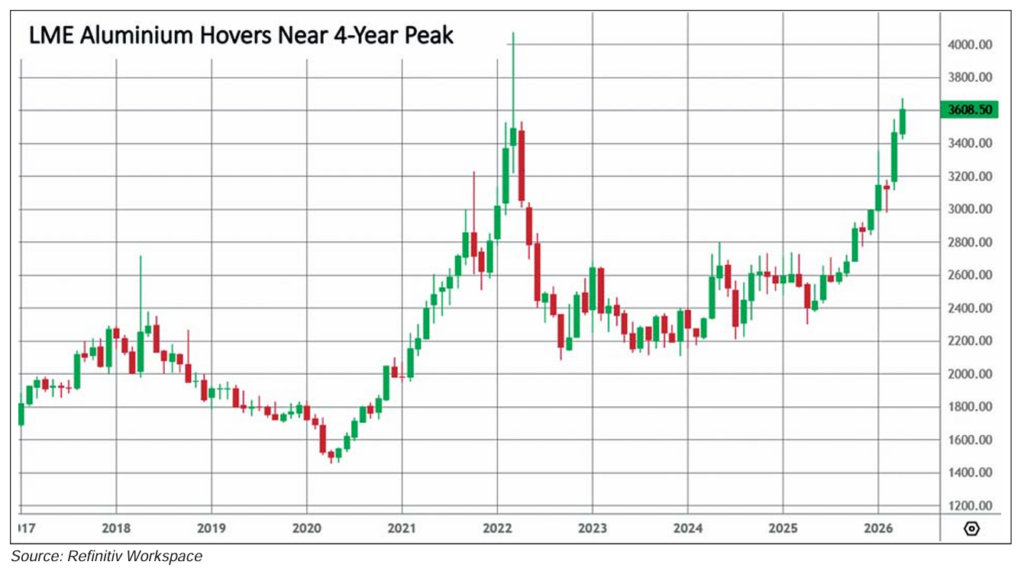

Aluminium prices have remained on a firm upward trajectory thus far in 2026. Tightening market fundamentals began pushing prices higher from October 2025, and disruptions linked to the Iran conflict have added further momentum to an already supply constrained market. As a result, LME aluminium prices climbed to a four year high, while India’s MCX aluminium futures hovered at record levels. Strong demand signals from China and increasingly tight global supply conditions have continued to support prices of the light metal.

The conflict involving Iran has triggered an unprecedented crisis in the global aluminium market, with potentially severe ripple effects across sectors such as construction, packaging, transportation, and renewable energy. Even if hostilities were to end immediately, Emirates Global Aluminium could take up to a year to recover from the damage caused by a missile strike on its Al Taweelah smelter in the month of March. Aluminium Bahrain (Alba), the largest single site aluminium plant outside China, has also been affected, although the full extent of the damage remains unclear. Before the attacks, Alba and Qatar Aluminium had already curtailed production due to power shortages. In addition, severe disruptions to shipping through the Strait of Hormuz raise the risk of further production losses as smelters draw down their inventories of raw materials.

The unfolding crisis in Iran has significantly escalated energy costs, adding further pressure to the aluminium market. Aluminium smelting is highly energy intensive, requiring vast and uninterrupted electricity supplies, and the surge in oil prices has pushed up power generation costs globally. This has increased production costs, particularly in regions heavily dependent on fossil fuels, with producers passing these higher expenses on to the market. Even before hostilities erupted in the Gulf, a global shortage of affordable power was already forcing capacity reductions and closures. In March, the Mozal aluminium smelter in Mozambique, majority owned and operated by Australia’s South32, was placed on care and maintenance after the company failed to secure an economically viable power supply contract.

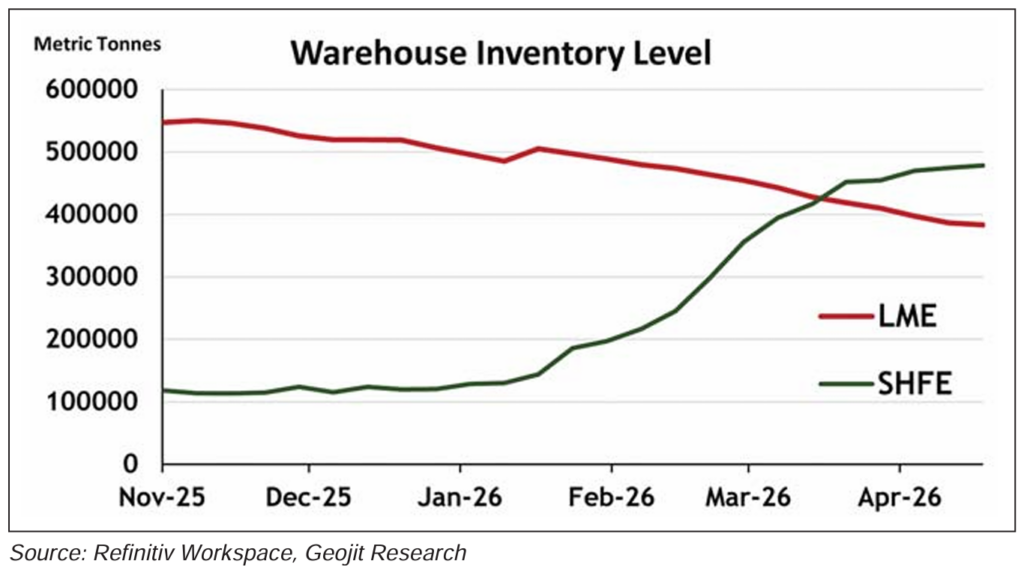

The LME stocks have fallen below 400,000 metric tonnes, with an additional 100,000 tonnes held off warrant. CME warehouses have also seen heavy withdrawals, with total deliverable stocks plunging 70% since the start of the year to just 1,864 metric tonnes. Meanwhile, warehouse stocks on the Shanghai Futures Exchange have now climbed above 400,000 metric tonnes, surpassing LME inventory levels. China’s aluminium imports have also stayed robust, with inbound shipments of unwrought aluminium and aluminium products increasing by 6.9% year on year in March to 360,000 metric tonnes.

Rising regional premiums and sustained supply disruptions in the Middle East are reshaping global aluminium trade flows. Russia’s major aluminium producer, Rusal, is actively diversifying its export destinations by redirecting shipments toward Japan and South Korea, reducing its reliance on the Chinese market. Rusal produced approximately 3.9 million tonnes of aluminium in 2025 and sold 4.5 million tonnes of aluminium and alloys during the previous year, including inventory sales. At the same time, China remained a significant buyer of Russian aluminium, importing more than 2 million tonnes in 2025.

China remains the world’s largest aluminium consumer, accounting for over half of global demand. This strong appetite is fuelled by infrastructure development, the expansion of electric vehicle production, and investments in renewable energy, all of which are aluminium intensive. Recent stimulus measures have provided an additional lift to consumption, keeping demand levels high. Given China’s central role in the market, any shift in its economic momentum has a direct and significant effect on global aluminium prices. Current indicators point to sustained demand, supporting a bullish near term outlook for the metal.

In the US, the defence sector could contribute modest additional aluminium demand in the months ahead. Military uses—particularly in armaments and aerospace—depend heavily on aluminium because of its high strength to weight ratio. Rising geopolitical tensions and increased defence budgets may lead to greater consumption. Although this demand is relatively small compared with broader industrial use, it provides extra support to the market and highlights aluminium’s strategic importance beyond civilian applications.

Amid these developments, US President Donald Trump revised national security tariffs on steel, aluminium, and copper imports. The adjustments reduced duty rates on derivative products, simplified compliance requirements, and addressed concerns around under-reporting of import values. The policy changes are expected to moderate cost pressures for downstream users while maintaining protections on primary metal imports.

As of January 2026, the global aluminium market was estimated to be operating with an implied supply deficit of approximately 1.27 million tonnes, highlighting the severity of current market tightness. With shipping through the Strait of Hormuz severely restricted, supply disruptions risk intensifying further as smelters deplete their raw material inventories. Looking ahead, aluminium prices are expected to remain elevated through the remainder of the year, supported by robust demand and persistently constrained supply. Price volatility is likely to continue amid ongoing geopolitical risks, fluctuations in energy markets, and heightened speculative activity. Should oil prices remain firm and inventory levels stay low, aluminium prices could continue to trade near record highs. However, any slowdown in China’s economic growth or a de-escalation of geopolitical tensions could temper the rally.