During the recently concluded India’s T20 World Cup triumph, one interesting thing, not related to cricket, which made the news were Hardik Pandya’s watches from Richard Mille to Favre Leuba.

For many people, watches, especially expensive ones, have always carried a certain meaning. For most folks, Rolex wears that crown; pun intended. It is less of an impulse purchase and more of a milestone. Something you arrive at after years of work, patience, and perhaps a few smaller watches along the way.

But something happened in 2020 which changed the nature of the watch acquisition industry, the pandemic. Prices of popular Rolex models began to rise sharply in the secondary market. That’s when the attention of watch collectors shifted to Tudor.

Tudor shared the same history as Rolex, and many of its watches carried familiar design cues. It came from the same stable, often used similar components, and offered a design language that felt instantly recognisable but at far more approachable prices. It’s no surprise then that it picked up the label of the “poor man’s Rolex”.

The phrase may sound dismissive. But spend some time with models like the Black Bay 58 or the Black Bay 41, and it becomes clear that Tudor isn’t just a substitute. It stands comfortably on its own.

A similar parallel exists in equity investing. A category within mutual funds, often overlooked that appears, at least on the surface, to share a philosophy with PMS and long-only equity AIFs: Focused Funds. Much like Tudor came to be seen as a more accessible alternative to Rolex, Focused Funds are often viewed as a way to access concentrated investing within the mutual fund Structure.

The comparison is intuitive. But it only tells part of the story.

By regulation, funds in this category can hold a maximum of 30 stocks which is a level of concentration typically associated with PMS and long-only AIF portfolios. In theory, that should demand a very different approach from managing a diversified mutual fund.

But concentration is not just about holding fewer stocks. It is reflected in how capital is allocated, how portfolios evolve, and how distinct they are from a manager’s broader strategy.

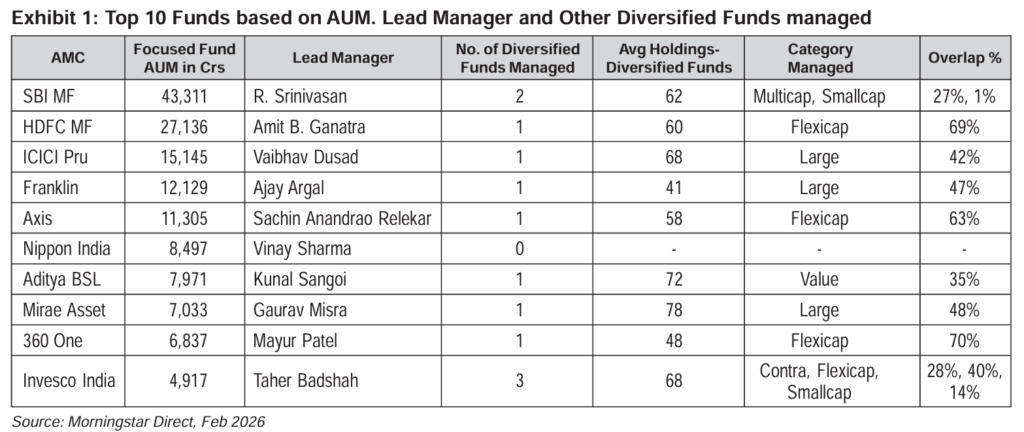

To understand this better, we looked at who manages these funds (lead manager) and what else they run within the fund house and how do they construct the portfolio.

In most cases, the managers running these portfolios also oversee diversified strategies. Across these mandates, the average number of holdings typically ranges between 60 and 78 stocks.

This raises a natural question. If a manager’s broader investing approach involves holding 60–70 stocks, what changes when they are required to run a 25–30 stock portfolio?

Funds like Quant Focused, though smaller, run far more concentrated portfolios in some cases with just 18–20 stocks. On the other end, most large funds appear to be managed by teams whose natural orientation is more diversified.

A more revealing way to look at focused funds is not just by the number of stocks they hold, but by how different they are from the manager’s other portfolios. One way to test this is to examine the overlap between the focused fund and the diversified strategies run by the same manager.

Across the largest focused funds, this overlap varies meaningfully. A higher overlap suggests the focused fund may be drawing heavily from the same pool of ideas as the diversified portfolio, effectively representing a more concentrated version of it. A lower overlap, on the other hand, indicates a more distinct portfolio construction process.

This distinction matters as it clearly points to whether the portfolio is built through selection or merely through reduction. Managing a concentrated portfolio is not simply about holding fewer stocks. It requires deciding which ideas deserve disproportionate capital, and which ones are excluded.

Portfolio construction offers a clearer picture.

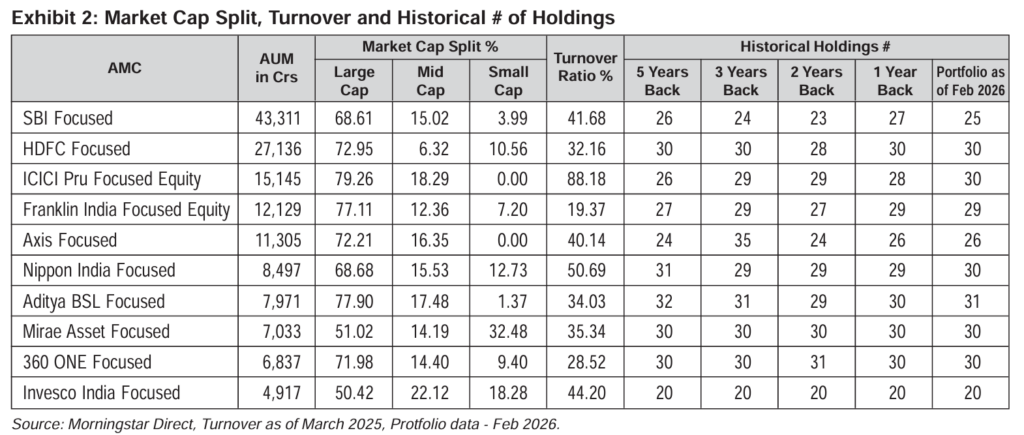

Looking at these portfolios, a few patterns emerge. First, most funds operate close to the upper limit of the category with respect to the number of holdings. A few, however, maintain slightly fewer holdings allowing flexibility to add new positions without exiting existing ones.

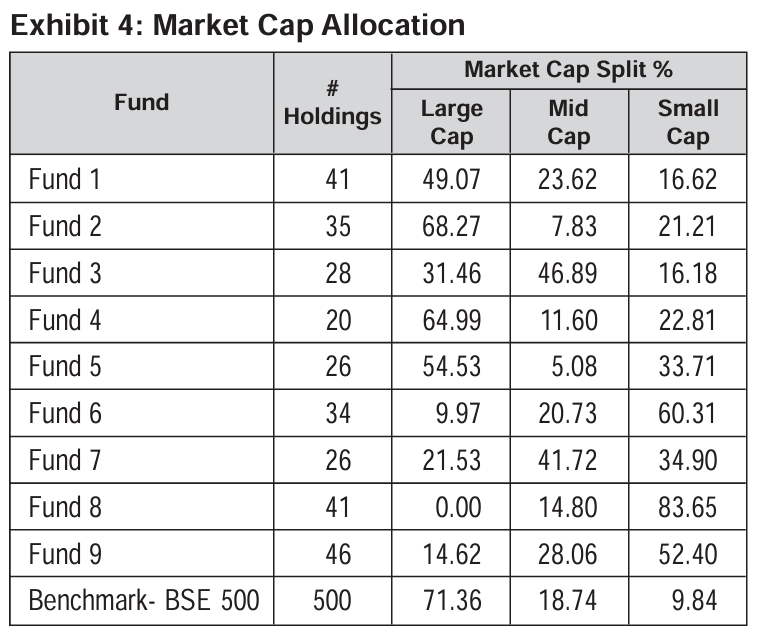

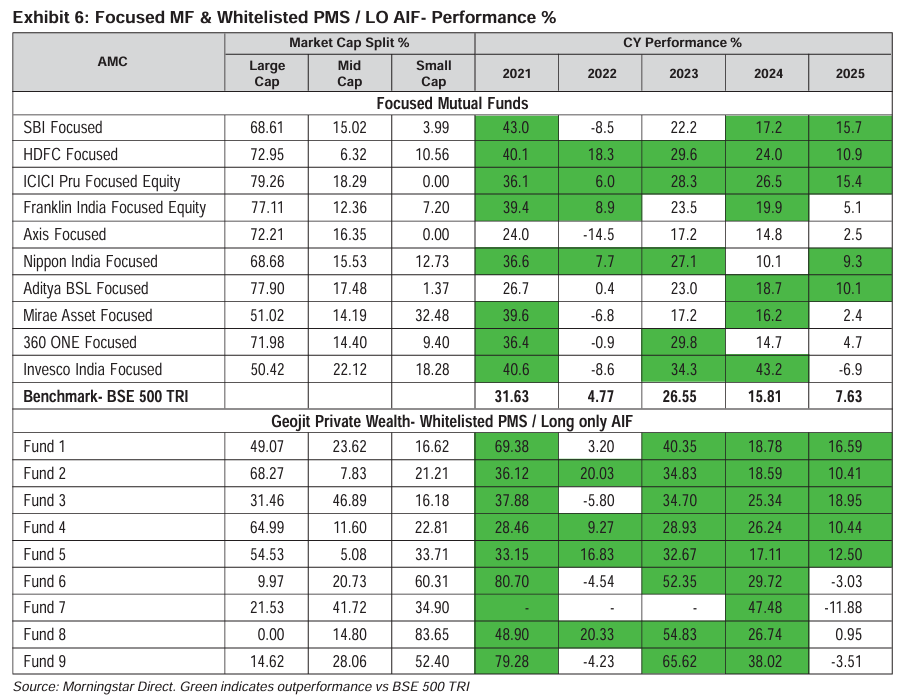

Second, market cap allocations remain tilted towards large caps. In several cases, large cap exposure exceeds 65–70%, with selective allocations to mid and small caps. This is especially evident in SBI Focused Fund, given its large AUM.

There are, however, notable deviations. Mirae Asset Focused, for instance, carries a higher allocation to small caps, indicating a willingness to move down the market cap curve. SBI Focused also stands out as the only fund in this group with a meaningful allocation to international equities, with roughly 10–11% invested overseas.

Portfolio turnover adds another layer. Ratios range from sub-30% levels in some funds to upwards of 80% in others, reflecting differing approaches to conviction from stable portfolios to more actively rotated ones. With fewer stocks, each change carries a higher opportunity cost.

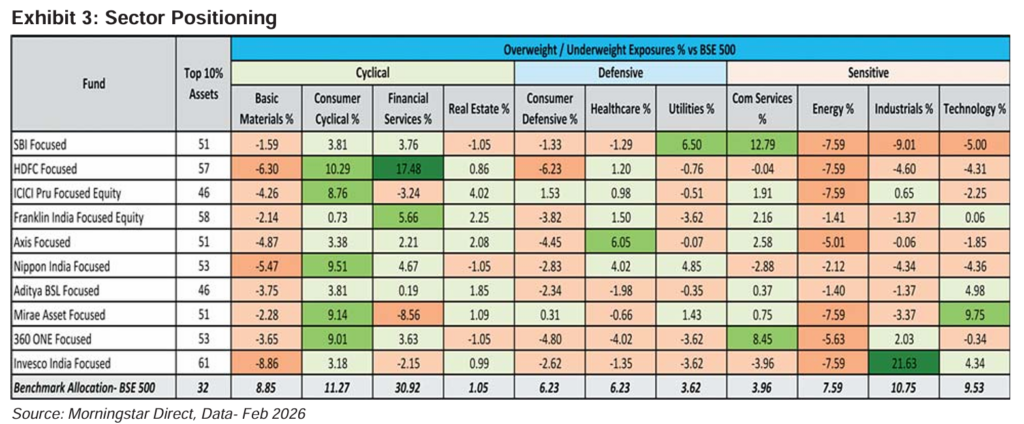

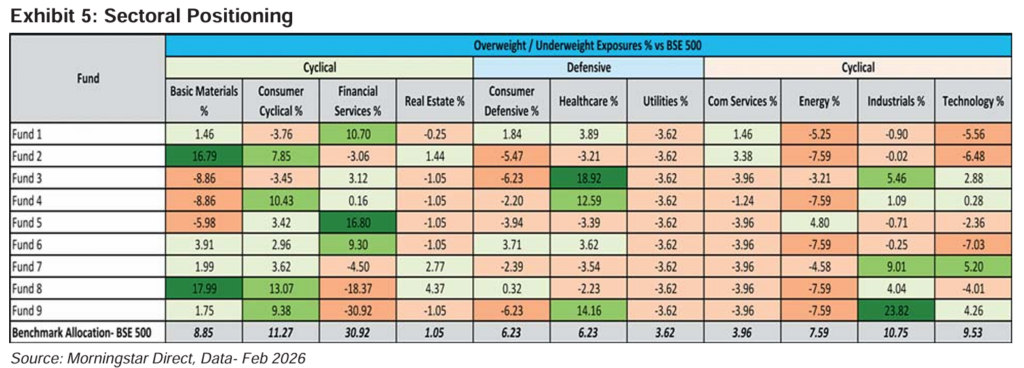

Most managers seem to adopt a bottom-up stock-picking approach. As a result, sector deviations tend to be more pronounced.

The data shows that funds like HDFC Focused, Invesco Focused and SBI Focused have taken meaningful sector exposures relative to the BSE 500. At the same time, most funds remain underweight on Basic Materials and Energy.

Portfolio construction also reflects differing styles across managers. For instance, SBI’s approach leans towards quality and valuation, while HDFC has historically taken sharper valuation calls. With recent changes in fund management at HDFC, how this evolves remains to be seen.

PMS & Long-Only AIF – Differentiators

Not every manager who runs a focused fund is necessarily a focused investor.

A comparison with select PMS / long-only AIF strategies offer a useful contrast. Unlike mutual funds, PMS / long-only AIF portfolios are not bound by daily liquidity requirements or position limits. This allows for greater flexibility in both stock selection and position sizing.

As a result, portfolios often exhibit:

- Higher allocations to mid and small cap stocks

- More pronounced deviations from benchmark sector weights

- Greater variation in position sizing

For context, we opted to compare with Geojit Private Wealth’s Whitelisted PMS / long-only AIFs.

While most focused funds remain underweight on Basic Materials, PMS / long-only AIFs show selective overweight exposures. Sector positioning particularly in communication services and healthcare also shows wider dispersion in PMS strategies compared to the relatively measured positioning of focused funds.

What the performance portrays

From the table above, it is clear that PMS / long-only AIFs can outperform meaningfully during favourable market conditions. That said, during periods of volatility, they can also see significant drawdowns.

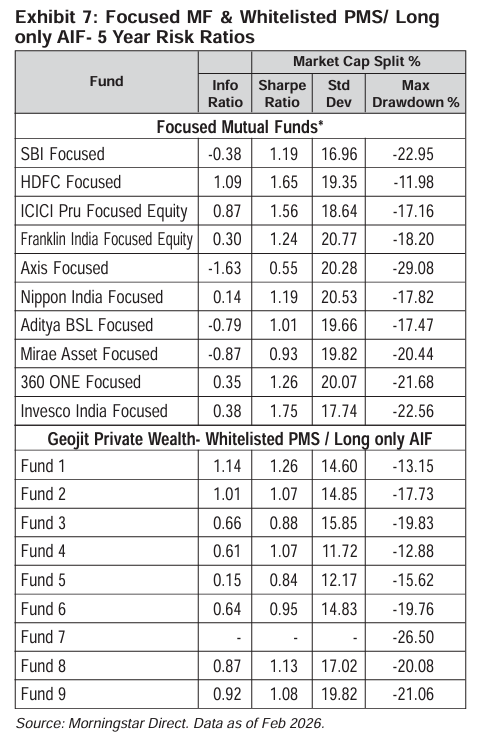

*It is important to highlight that the risk ratios are not measured on an identical basis. Mutual fund metrics reflect rolling five-year averages calculated since 2019, while PMS / AIF figures are on a trailing basis.

Even so, the data does not point to a clear winner. Both Focused Mutual funds and PMS / AIF strategies show a wide range of outcomes across risk-adjusted returns and drawdowns. What stands out instead is the dispersion particularly among PMS / AIF strategies where outcomes appear more a function of the manager than the vehicle itself.

Key Takeaways

This article does not attempt to establish one as superior. Instead, it highlights how within concentrated portfolios, approaches and philosophies can differ, yet each can hold its own.

A concentrated portfolio may be defined by the number of stocks it holds.

But conviction lies in how those ideas are chosen and how they are managed and lastly identifying if the manager has the skills to manage it prudently. What this means in practice is that the choice between these vehicles is less about structure and more about where that philosophy is likely to come through more clearly.

Retail investors with a higher risk appetite may consider focused funds, which allow managers to take relatively concentrated calls within a regulated structure.

HNIs and UHNIs, on the other hand, may consider wellmanaged PMS / long-only AIFs as a complement to their mutual fund portfolios, particularly where flexibility and differentiated positioning are desired.

In watches, as in investing, products that look similar often operate very differently beneath the surface. The question is not what they resemble, but what they are built to do. But like all good choices in watches or investing it comes down to what suits you best.