India’s economy in the first quarter of calendar year 2026 stands at crossroads, influenced by technological disruptions, geopolitical realignments, and domestic fiscal policies. The market sentiments are shaped by a confluence of factors, including the AI bubble, trade pacts, and corporate earnings trends offering characteristics of both boom and bust. In a volatile session of global sell-off and correction in the Indian IT space, investors are expected to hold their nerves with a long-term vision.

We need to understand that the transition disguised as a disruptor holds the path of new growth, carrying the new system of work advancement. This new way of development will require fast adaptation, or else we carry the risk of obsolescence. An economy, industry, and company will survive and grow well if they adopt what is bound to be disruptive today.

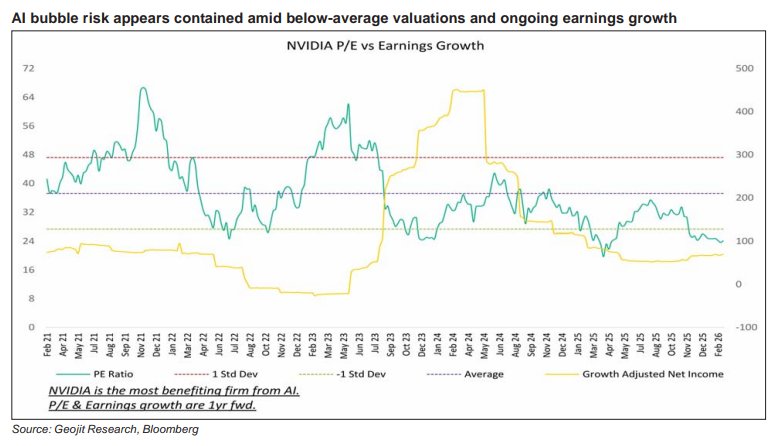

India has unleashed $200 bn of AI-based capital expenditure for the next 2 years, it is placing its resources in the right way. This is expected to boost the economy through the involvement of key ecosystems, such as reality, power, software, and hardware manufacturing. The association between Infosys and Anthropic is encouraging, as it suggests that next-generation AI applications are unlikely to disrupt Indian IT companies’ business models to the extent initially feared. These solutions are expected to be incorporated into both existing and new projects, which should help ease concerns around long-term business sustainability. That said, some uncertainties persist—particularly regarding how deal sizes and pricing may evolve and the net impact on margins once employee-cost efficiencies and productivity gains are balanced out. While the sector’s outlook for FY27-28 appears muted, which is reflected in current 5-year low valuations. At the same time, the environment is offering opportunities for long-term investors to re-enter the space, as more clarity is likely to emerge over the short to medium term.

The selloff in the IT sector: AI disruptions

The Indian IT sector, a cornerstone of the nation’s export economy contributing over 8% to real GDP, has faced one of its most severe corrections in recent years. In February 2026, the Nifty IT index tumbled 8.2% in a single week, its worst performance in over 10 months, erasing

~Rs. 3 Lakhs crore in market capitalization of the top six IT firms. This selloff, which has seen the index decline 13.7% YTD, surpassing the 12.6% drop in 2025, was triggered by heightened anxieties over AI disruptions.

Key catalysts include the launch of advanced AI tools that automate workflows that are traditionally dominated by Indian IT firms’ headcount-based models. Moreover, commentary on “AI deflation” further amplified fears, suggesting that it will reduce project timelines and headcount needs. As a result, major tech players encountered declines of up to 14-17%. The Nifty IT index hit a 52-week low; moreover, the index reflected a 32% correction from its all-time high, reminiscent of post-2008 declines.

Analysts attribute this to a structural shift. AI is automating routine tasks, pressuring the headcount-based outsourcing model. Clients are increasingly favouring outcome-based pricing, potentially leading to layoffs and muted revenue growth of 7-8% for FY27-28 among top firms. Stronger-than-expected US employment data in early February also diminished hopes for Fed cuts, adding to the pressure by curbing IT spending. However, some view this as an “opportunity in disguise.” Current valuations are lower than the sector’s 5-year average at~20x one-year forward P/E suggests undervaluation. Moreover, collaborations like Infosys with Anthropic indicate integration rather than obsolescence, potentially easing long-term sustainability concerns.

India-US trade deal: A boost for bilateral trade and economic growth

The India-US trade deal, announced on 06 February 2026, marked a significant de-escalation in bilateral tensions and a pivot toward reciprocal trade. Under the interim framework, the US has reduced tariffs on Indian goods from 25% to 18%, while eliminating a punitive 25% tariff linked to India’s Russian oil imports. In return, India pledges to purchase over $500 billion in US goods—spanning energy, technology, aircraft, and agriculture, over 5 years, and to cut tariffs on US industrial and agricultural products in key sectors. This pact, expected to culminate in a full Bilateral Trade Agreement (BTA) by 2026-27, aims to elevate bilateral trade to $500 billion by 2030.

Economically, the trade pact has injected optimism into the Indian economy, with economists projecting an upgrade in the FY27 GDP forecast by 20–30 bps. It addresses longstanding imbalances, restoring India’s competitiveness against regional peers like China, and is expected to propel Indian exports to the US beyond $100 billion soon. Sectors poised to benefit include pharma, gems and jewellery, textiles, aquaculture, auto ancillaries, chemicals, and capital goods, with zero tariffs enhancing market access and supply chain resilience. Post-announcement, the rupee appreciated below 91 against the dollar and equity markets rallied 2.7%.

However, the INR’s momentum has moderated recently after the Supreme Court struck down Trump’s reciprocal duty policy, a development the market has interpreted as marginally positive. Meanwhile, the US and India have deferred the ongoing trade talks, which were earlier expected to be finalised by March. In parallel, the US has reset to a universal tariff of 15% on all imports, reducing the deal’s relevance in the near term. That said, the US government remains engaged and is exploring legal provisions to implement the policy framework. Although the revised tariff rate is lower at 15%, the new framework was initially expected to offer India a relative advantage over other Asian peers. At the same time, the universal tariff has introduced fresh uncertainty into global markets, as it may apply across countries and product categories, warranting greater clarity. Additionally, it remains to be seen whether the Modi government will seek to renegotiate or recalibrate the deal to make it more beneficial for India following the Supreme Court’s intervention. Nevertheless, alongside India’s FTA with EU, UK, Australia and Oman positions India as a key player in global supply chains and tariff advantages against Asian peers, potentially unlocking private investments. Deals represent a “win-win” with long-term gains which will start to materialize from 2027 onwards.

What does Q3 performance imply so far?

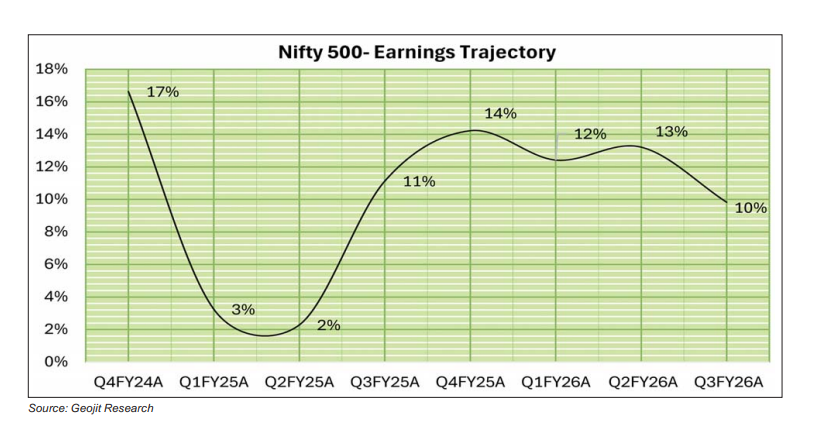

With the Q3FY26 earnings season entering its final leg, early data from 460 companies within the Nifty 500 indicates a marginally in-line performance, with PAT growth of 10% YoY compared to the projected 9%. The results highlight a polarized landscape: 235 companies exceeded expectations, while 225 underperformed. Moderate demand, rupee depreciation, and global tariff concerns have weighed on overall performance.

Sector-wise, performance has been supported primarily by Energy, Financials, and Metals, which helped offset the drag from weaker segments. The Energy sector benefited from relatively low and stable crude oil prices, while better loan growth and stable asset quality underpinned the strength in Financials. Metals gained from higher realisations across non ferrous players and improved volumes in steel companies. On the downside, Communication Services and Consumer Discretionary have been the major laggards. Additionally, one-time provisions related to the new Labour Code have partly impacted earnings across several companies.

The GST rationalisation implemented in late 2025 has further supported disposable income, providing an additional boost to consumption. While FY26 was characterised by heightened global uncertainty, India is now better positioned following trade agreements with the US and the EU, which have significantly reduced tariff related risks. While AI-led disruptions and ongoing geopolitical tensions continue to pose headwinds.

India’s economic narrative in early 2026 is one of adaptation and potential. The IT sell-off highlights vulnerabilities to technological shifts but also adaptation opportunities. The India-US trade deal injects optimism, enhancing exports and investor sentiment. The Nifty 50 earnings growth is projected at 5–6% for FY26, accelerating to 12–15% in FY27. Looking ahead, the outlook for FY27 remains constructive, underpinned by resilient domestic demand and strong GDP growth. Investors should adopt a long-term, research-driven approach, focusing on sectors with structural tailwinds.