The opening weeks of 2026 have brought a stark reminder of how quickly global uncertainties can overshadow domestic optimism. Indian equities began the year on a buoyant note, with the Nifty50 climbing to a record high of 26,340 on 2nd January , fuelled by expectations of strong Q3FY26 corporate earnings and resilient economic fundamentals. However, a confluence of geopolitical developments and lingering trade frictions has injected significant volatility into the market, pushing indices into a corrective phase and testing investor confidence.

Geopolitical developments including the US operation in Venezuela, domestic unrest in Iran, the threat to take control over Greenland, the persistent postponement of the India-US trade deal and Trump’s tariff threat on Russian oil importers have expanded global and domestic risk. Heaven assets, such as Gold, Silver and key metals, are rising as safety demand increases and supplies are being controlled. While the third quarter was initially expected to deliver strong double-digit growth, early indicators point to pressure on profitability due to higher costs stemming from the new labour code, elevated metal prices, and increased interest expenses. Meanwhile, expectations from the 2026 Union Budget are narrow to boost a trigger in the stock market unless the government intends to offer a strong hand to the domestic investors.

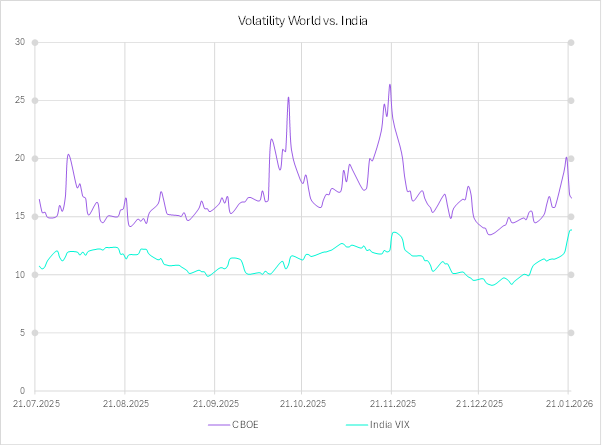

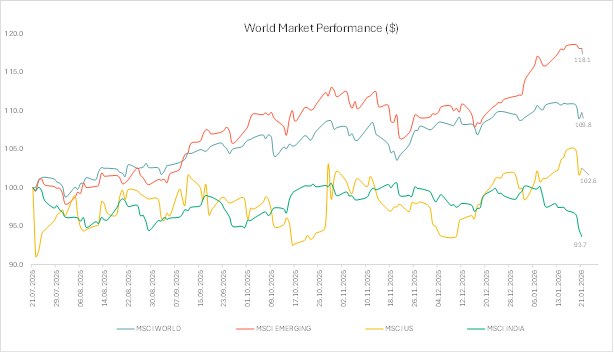

In essence, volatility indexes are expanding and the market is contracting. India continues to be a selling market for FIIs, while other EMs like Japan are on the buy list due to new growth after a decade of slowdown led by reforms The positive impact of direct and indirect tax reductions announced in 2025 is beginning to reflect in 2026. Although a reversal in India’s market trend is widely anticipated, the inflection point remains uncertain, with attention focused on ongoing negotiations and the need for sustained domestic policy support amid the expansion of global protectionist measures.

Escalating Geopolitical Risks

Geopolitical risks have emerged as the dominant issue in the early part of 2026. The raid in Venezuela, instability in Iran, and renewed US scrutiny of India’s imports of Russian oil have unsettled sentiment. Although Venezuela’s situation is unlikely to significantly affect global oil supplies given its limited output and the existing global surplus, it has introduced some uncertainty, resulting in bouts of volatility in crude prices. These concerns have been amplified by unrest in Iran and renewed geopolitical rhetoric by world leaders. However, given the oversupply situation of crude in the global market and the slowdown in world demand, the current price trend is mostly subdued. This trend is expected to continue in the long term, which will ultimately benefit major importers like India and China.

More pressing concerns stem from the US administration’s aggressive stance of using sanctions and tariffs as a policy. Sanctioning the Russia Act of 2025 by Trump has raised fears that the US could impose tariffs as high as 500% on countries importing Russian oil, with India potentially facing the continuation or even escalation of the existing 25% penalty tariff. Domestic market participants had been anticipating progress in US-India trade negotiations, especially the removal of the 25% penalty tariff, given India’s recent reduction in Russian oil imports. However, the lack of clarity on ongoing discussions and their implementation timeline continues to weigh on market sentiment and has contributed to FII selling.

Source: Bloomberg, Geojit Research

The broader shift in US foreign policy to take direct interventions, as in Venezuela, has elevated geopolitical risks. Including the 2025 attack on Iranian nuclear facilities, though it has demonstrated that such events may have limited impact on the global markets, yet the potential for escalation remains a concern. Additionally, the US’s renewed interest in acquiring Greenland for strategic and minerals reasons has sparked diplomatic tensions with European NATO allies by again using tariffs as a weapon. These developments have contributed to a rising trend in precious metals prices, while equities face downward pressure. Some moderation has emerged following Trump’s modest speech at the Davos meet, but the diplomatic tensions between the countries have deepened affecting future developments.

Source: Bloomberg, Geojit Research

Domestic Macros, A Source of Resilience

Domestically, India’s economic fundamentals remain a key source of resilience. Despite this, the market is struggling, led by external challenges, including FIIs selling. FII outflows continue to persist in India, while their buying in other Asian peers like Japan and China continues due to attractive peer valuation, stimulus & reforms from the government and AI growth. INR dropped to a new low against USD at 91.7.

The ongoing delays in the US-India trade deal remain a critical risk factor. Negotiations are expected to proceed in phases, with the initial focus on removing the 25% penalty tariff, followed by a comprehensive agreement later. However, US demands for greater market access in agriculture and dairy, sectors where India holds a protective policy for its small farmers, have complicated the trade talks. US narratives indicate that they are not satisfied with the reduction in Russian oil imports, suggesting more actions are expected. Sectors with significant US exposure, including IT, pharma, textiles, and gems and jewellery, are particularly vulnerable to prolonged uncertainty, facing potential loss of business or negative sentiment.

A preview analysis of Q3 results suggested a rebound in earnings, but actual earnings are marginally below estimate based on initial results from IT and Banks etc. This is because of the new labour code, high metal prices and interest costs. The majority of the effect is forecast to be one-time, and the outlook for Q4 is forecast to be better supported by management commentary. The outlook for FY27 is projected to be stronger than FY26, aided by tax reforms, although this assumes a successful trade agreement with the U.S. In parallel, India remains optimistic about progress on the EU–India Free Trade Agreement (FTA).

Persistent FII Outflows: A Continuing Challenge

FIIs have extended their selling spree into 2026, following a record outflow of ~Rs 1.66 lakh cr. in 2025. In January 2026 so far, FIIs have withdrawn ~Rs 25,777cr from Indian equities, with net selling reaching Rs 4,543cr on January 16 alone. Lack of triggers to accelerate growth and low expectations on key events like the union budget have exacerbated the downfall as global uncertainties persist, including delays in the US-India trade deal, making FIIs more risk-averse toward India. In contrast, DIIs have provided crucial support, buying Rs 41,977cr worth of equities in January to date, supporting buying at lower levels with a long-term vision. Analysts warn that continued FII outflows could prolong India’s underperformance, weaken the rupee, and add volatility to export outlooks, particularly if the upcoming Union Budget 2026 fails to deliver stimulus to the domestic economy.

Last 6 Months FII Inflow Details

| Month | FII Inflow |

| July 2025 | -24,723 |

| August 2025 | -37,823 |

| September 2025 | -18,928 |

| October 2025 | 11,050 |

| November 2025 | 333 |

| December 2025 | -23,690 |

| January 2026 (till 20th Jan) | -25,777 |

Source: Bloomberg, Geojit Research

Investor Positioning Amid Uncertainty

Looking ahead, volatility is likely to remain elevated until greater clarity emerges regarding US-India trade dynamics, tariff-related issues and global geopolitical risk. Any positive outcome from trade talks or easing tariff concerns could trigger a strong rebound. In the near term, the Indian market is expected to trade within a range with a mixed bias. Strong domestic fundamentals, resilient GDP growth, robust credit trends, and earnings recovery provide a buffer against external risks. However, heightened geopolitical headwinds and FII sentiment will continue to dominate. Investors are advised to adopt a cautious stance in the short term, avoid knee-jerk selling tendencies during periods of volatility, and focus on selective opportunities where earnings prospects remain favourable. Overall, 2026 has begun with a reminder that global interconnectedness amplifies risks, while the intact India domestic story offers a long-term investor a chance to chip into the market. Any further capitalisation will develop as a good time and price for domestic and foreign investors to adopt aggressive buying in the Indian market.

1 comment

Excellent advise as to how to position themselves in the volatile uncertainty. Thanks .