2025 marked a challenging year. We started with a cautiously optimistic view due to Foreign Institutional Investor (FII) selling, high valuations, a downgrade in corporate earnings, and low capital expenditure. Optimism was based on the low risk of global recession, high fiscal and monetary support to the economy. Negativity compounded as global tariff wars and geopolitical conflicts extended, affecting India by moving it from a good to worst tariff list. FIIs adopted a “Sell India and Buy China” strategy due to premium valuations and lack of triggers.

The year 2026 is expected to be better, as external risks have been tested and are likely to reverse, including a pending US-India trade agreement that may strengthen the Indian rupee despite phased implementation. Corporate earnings have shown improvement, supporting mid and small cap segments with a selective approach.

Key risks and market conditions include uncertainty about the US-India trade deal, elevated US Federal Reserve Vinod Nair rates, ongoing Russia-Ukraine conflict, and sustained high valuations, though overall market volatility has decreased. World economies are working to reduce inflation pressures, and market volatility indices have fallen to a one-year low, India VIX at sub 10x.

We had suggested a Multi-Asset Investment strategy for 2025, which we are upgrading in 2026. We increase equity allocation to 85% (60% large cap, 15% mid cap, 10% small cap), reduce debt to 10% and gold at 5%, targeting a Nifty 50 index of 29,150 by December 2026, implying a 12% return.

2025: A split-screen year

The beginning of CY2025 saw a cautious but optimistic asset strategy take shape. Allocation tilted towards large cap equities, select domestic themes, precious metals, and fixed income. The rationale was clear: India was trading at a steep valuation premium, earnings downgrades were visible, and the global policy environment was unstable. The term “Trumponomics” quickly became a catch-all reference for the rapid escalation of tariff pressure that pushed India from a relatively advantageous position into one of the highest tariff targets of the year. Geopolitical pressure added fuel to volatility. The Israel–Hamas conflict and tensions between India and Pakistan contributed to sustained investor risk aversion. Commodities reacted first – gold and silver posted standout performances, aided by US dollar weakness after tariff disruptions, the freezing of Russian assets and the Federal Reserve’s halt of quantitative tightening.

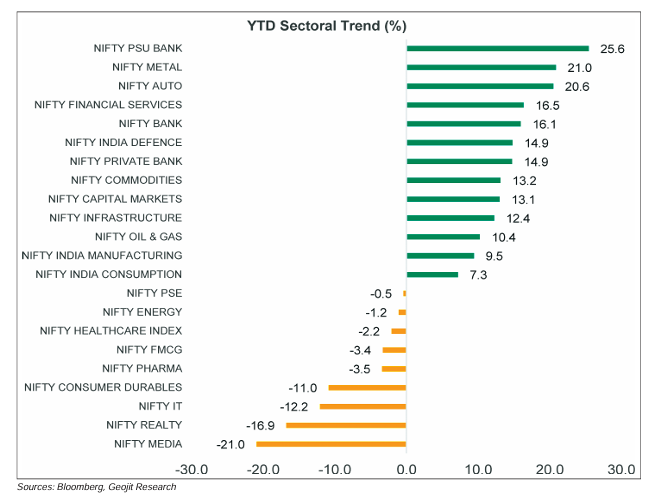

FIIs cut India exposure meaningfully. Their search for lower-valuation emerging markets and preference for AI-heavy markets created the largest capital shift of the cycle. The consequence was visible in foreign-exchange markets: the rupee depreciated to record lows, trade deficits widened late in the year, and global risk premia increased. Despite these headwinds, Indian equities did not break. Domestic flows acted as a counterweight. Systematic retail savings rose and household investors absorbed foreign selling. Earnings also began improving by Q2FY26 as inflation eased. Large caps, public sector enterprises, auto, metals and financials became key performance anchors, but gains were narrow rather than broad-based. As the calendar turns, 2026 still carries unresolved risks: uncertainty around a phased US–India trade negotiation, persistently high US policy rates, the Russia–Ukraine conflict, possible reversal of yen carry trades, and the pressure of Indian equities trading above long-term valuation bands.

A harsh external environment

US policy aggression has had visible ripple effects. Tariffs have compressed output, particularly in manufacturing intensive economies, and driven supply-chains away from established hubs. Mexico’s 50% tariff on Indian imports exemplifies how global diplomacy is being replaced by unilateral pressure. China’s restrictions on critical minerals further complicate the clean energy and semiconductor supply chain, raising the probability of input bottlenecks. These frictions tighten global liquidity conditions and often lead capital to retreat from emerging markets entirely. The US unemployment trend is turning upward, an early sign of labour-market stress. That dynamic, combined with weakening industrial output, could push the Federal Reserve toward additional rate reductions. But the timing will depend on inflation prints, job creation data, and yield curve normalization. With midterm elections scheduled for late 2026, US negotiators may accelerate trade de-escalation to stabilize domestic political optics.

Signs of global stabilization Not every macro signal is negative. From a medium-term standpoint, the probability of a structural peak in bullion is rising. If geopolitical conditions ease, gold may consolidate for an extended period, this typically supports equity performance because of their inverse correlation. Global growth is slowing, not collapsing. The IMF expects world output to soften from 3.3% in CY2024 to 3.2% in CY2025 and 3.1% in CY2026. Oil prices remain contained due to expanded output from OPEC+, US shale, inventory build-ups, seasonal shifts, and decarbonization. For India, lower crude is a direct inflation relief and current-account buffer. A durable return of foreign capital rests on softer US rates, a weaker dollar, and clearer trade policy. India’s valuation compared to EMs has declined to long term average, indicating positivity.

India’s macro setup: Strong real GDP, soft nominal growth

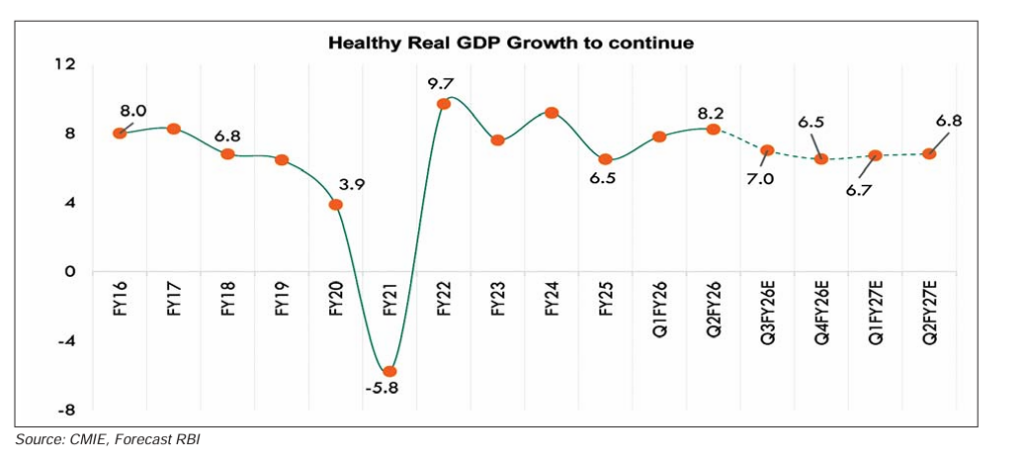

India’s real GDP remains strong at 8% in H1FY26 but nominal GDP has softened, printing 8.8%, well below the 10.1% budget assumption. The culprit is broad price stagnation in manufacturing and commodities. Inflation is expected to edge slightly upward in 2026 while remaining firmly within RBI’s target. That stability enables rate flexibility and reduces input-cost risk. Fiscal priority has shifted toward stimulating demand. After several years emphasizing supply-side frameworks, the government has introduced income-tax cuts, GST rationalization, and is preparing for the 8th Pay Commission, all of which lift household purchasing power.

Export performance remains uneven. Merchandise trade has been volatile, although resilient on an aggregate basis. Services exports continue to grow steadily, helping cushion the current account, particularly when combined with soft crude prices. Services’ rising share in the total export mix enhances India’s long-term external stability.

Liquidity, rates and domestic strength

The RBI cut the policy rate by 125 bps in CY2025, taking the repo to 5.25%. Given the inflation outlook, another cut is possible in 2026, though it is data dependent. Liquidity has also improved via a 100-bp CRR cut and open-market operations. Bank credit trends remain steady, with non-food lending expected near 10.5% in FY27E. Household leverage remains controlled, corporate balance sheets are cleaner than pre-pandemic levels, and borrowing costs are favourable. Domestic risk appetite continues to support equity depth. Monthly SIP inflows reached Rs.566 billion in H1FY26, while active SIP accounts crossed 179 million, a structural shift in household finance.

Valuation at the centre

Indian equities navigated 2025 with a narrow leadership profile. The Nifty 50 delivered 10.0% YTD, compared with 4.6% in mid caps and -8.3% in small caps. Investors favoured large caps, which is expected to continue in the short to medium-term, during periods of global trade anxiety. Mid caps saw episodic rotation as earnings rebounded in Q2FY26. Small caps, however, witnessed valuation pressure and selling due to high valuation. Forward valuations remain elevated. The market trades near 20.3x, modestly above the three-year average. That implies continued sensitivity to earnings disappointments and global volatility. However, expectations are high on Q3 results, which will serve as an important sentiment pivot of 2026.

The case for selectivity in 2026

India’s equity outlook in 2026 is supported by a combination of easing geopolitical and tariff pressures, resilient domestic demand, a liquidity-friendly stance from the RBI, and the gradual narrowing of India’s valuation premium versus other emerging markets, all of which together create a more stable backdrop for measured equity gains. US policy cannot sustain aggressive tariff postures indefinitely, domestic inflation, declining corporate profitability, job softness and political timelines will act as constraints. Multiple comprehensive trade negotiations underway also suggest a path to tariff reduction. Domestic consumption is poised to improve through tax relief, GST reforms, increased rural income, and controlled inflation.

Nifty target upgrade: A moderate upside year

A balanced allocation approach for 2026 would favour stability and measured participation, with a stronger tilt towards large-caps supported by moderate exposure to mid and small caps, while keeping gold, silver and debt at lower weights to manage volatility and insulate portfolios from external shocks. The Nifty currently trades near the 2025 base-case target of 26,500. The updated December 2026 base-case target stands at 29,150, implying ~12% annual upside. The assumptions underpinning the target include a recovery in private capital expenditure an improvement in the earnings cycle, a moderation in global-risk variables, a supportive inflation and liquidity dynamics.

The sectoral outlook for 2026 appears constructive. The banks enter the year with steady double-digit credit growth and healthier balance sheets, while consumption is poised to strengthen on rising disposable incomes, tax rationalization and softer inflation. FMCG demand should improve with better rural income and easing input costs, and healthcare continues to benefit from structural drivers such as ageing demographics and capacity additions. Infrastructure execution remains strong as spending by railways and roads accelerates and private participation rises, and the real estate cycle is supported by lower borrowing costs and resilient demand in premium markets. Technology may see a gradual recovery as global macro risks ease and AI-led deal flow improves, positioning 2026 as a year of stabilization rather than exuberance across major sectors.

Challenges remain: low domestic inflation may hinder nominal growth acceleration, US inflation remains sticky, and rate pivots could be slower than anticipated. But the direction of travel favours recovery rather than contraction.