Early results from listed companies indicate that the slowdown in sales witnessed in recent times continues in the September 2025 quarter. Profits growth has moderated too, and expansions in profit margins have been arrested. Early results show a fall in net profit margins. But these companies are unlikely to be fairly representative of the full set of listed companies.

Financial statements of 291 companies were available till 21 October 2025. Of these, comparable statements for each of the preceding four quarters were available for 279 companies. These 279 companies account for a mere six percent of all companies that announce their financial statements on a quarterly basis, but a significant 23.6 percent of their sales. We analyse the results of these 279 companies. The analysis will place the result in context of the broad long-term trends seen in all companies but will mostly discuss the results of these companies in the most recent five quarters.

Net sales of the 279 early birds grew by 4 percent, year-on-year (y-o-y), in the quarter ended September 2025. This is better than the less-than 2 percent growth seen in the previous, June 2025 quarter. But, it is lower than the 5-8 percent growth seen in the preceding three quarters.

A large part of this fall in the growth in the top line can be explained by the fall in retail inflation. While the y-o-y growth in nominal sales of companies dropped from nearly 8 percent in the September 2024 quarter to 4 percent in the September 2025 quarter, inflation also fell from 4.2 percent to 1.7 percent in the same period. Prima facie then, real growth in sales in the quarter ended September 2025 is lower than in the September 2024 quarter but, it is distinctly higher than in the preceding three quarters.

While this seems to be a relief, it is still quite an anemic growth rate. Further, real growth in sales of these companies has been quite poor in all the five quarters. This can be judged by comparing the inflation-adjusted growth in sales of these companies to the real growth in GVA. In the quarter ended June 2025 when the economy galloped at 7.6 percent, these companies shrank their top line in real terms. In the preceding two quarters, while real GVA grew by 6.5 and 6.8 percent, real sales of listed companies grew by 1.7 and 0.9 percent.

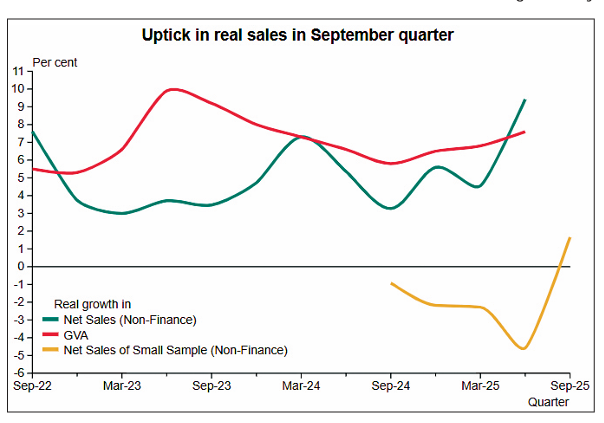

Growth in real sales of listed non-finance companies illustrates this problem better. Real sales of the 184 non-finance companies among the early birds grew by 1.7 percent in the quarter ended in September 2025. But, the same 184 companies saw their real sales fall in each of the four preceding quarters. This was when the economy was growing between 6 and 7.6 percent.

Real growth in sales of all listed companies does not bear out India’s growth story as is seen in the real GVA growth series. In 9 of the 12 quarters ending in the quarter ended June 2025, growth in real sales of non-finance companies is lower than the growth in real GVA and in one quarter the difference is negligible. On an average, the real growth in sales of companies was 1.9 percentage points lower than the growth in real GVA. While the average real GVA growth during these 12 quarters was 7 percent, the growth in real sales is 5 percent.

The growth trajectory of the 184 early birds is completely out of sync with the GVA growth and also the growth of the full set of listed non-finance companies. Between September 2024 and June 2025, while the average y-o-y growth in real sales of all listed non-finance companies was 5.7 percent, these 184 companies recorded a real fall in each of the quarters.

In nominal terms, while the full set of all listed non-finance companies shows an average growth of 4.6 percent per quarter between September 2024 and June 2025 quarters, the 184 companies show a growth of only 3.4 percent in the September 2025 quarter.

Therefore, we do not believe that inferences drawn from this set would be reliable in telling us of the overall performance of the listed companies in the September 2025 quarter.

Nevertheless, the early birds tell us that while the growth in sales was sluggish, other income and extraordinary income of these companies shrunk. As a result, growth in total income was more sluggish. Raw material expenses growth was correspondingly sluggish. Interest expenses of these companies declined for a third consecutive quarter.

Growth in profits has been modest. 91 finance companies whose results are available saw their profit after tax increase by a smaller 5.6 percent in the September 2025 quarter after having seen them grow by 8-12 percent in the preceding four quarters. PAT growth of the 184 non-finance companies has been volatile. It grew by -2, 8, 6 and 33 percent in the four quarters from September 2024 through June 2025. In September 2025, the PAT of these companies grew by a modest 2.5 percent.

The net profit margin of the 279 companies had been rising steadily in the past four quarters. It grew from 13.1 percent in the quarter ended in September 2024 to 13.7 percent in the quarter of December 2024 and then to 14.1 percent in the March 2025 quarter and 14.6 percent in the June 2025 quarter. In the September 2025 quarter, the net profit margin fell to 13.4 percent. This fall in margins is essentially a non-finance companies’ phenomenon.

We need to wait for more results to be announced in the coming days to gain a more reliable sense of the performance of the listed companies in the September 2025 quarter.

Author is MD and CEO of Centre for Monitoring Indian Economy Pvt. Ltd.