A large part of August was mainly about dealing with uncertainty after Trump imposed steep tariffs. This brought India’s oil and defence imports into sharp scrutiny, pushing the Nifty down by another 1.5% to add to the near 3% cuts in July. The July-August period also marked the longest stretch of declines since a strong recovery move was set off in April. But it would be too simplistic to see tariff uncertainty as the sole reason for the tumble. The bounce back from April lows that pushed Nifty 18% higher just about stretched as far as the September 2024 peaks, and it was not surprising that a profit booking spree ensued. The FIIs’ sell off can also be seen in this light.

India has become the most underweighted market in emerging market (EM) portfolios, with an active weight of –2.9%, according to Nomura’s analysis of 45 major EM funds. In July, relative allocations to India declined by 110 basis points month-on-month, as 41 of these funds trimmed their exposure. Meanwhile, Hong Kong, China, and South Korea saw increased interest, benefiting from this regional reallocation. Allocations to these markets rose by 80 basis points, 70 basis points, and 40 basis points respectively, signaling a clear shift.

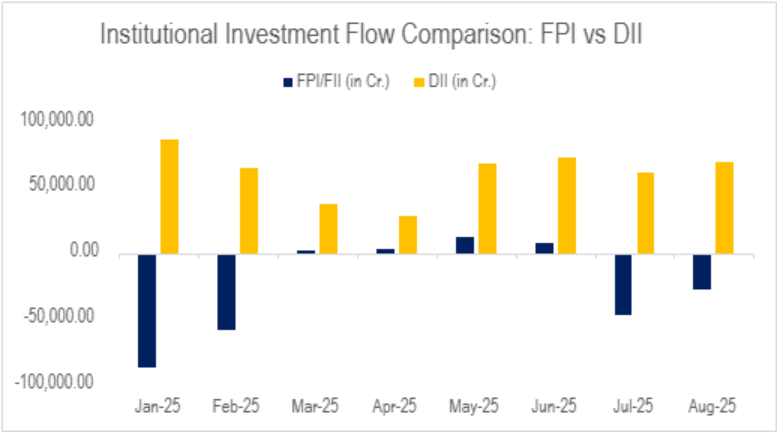

Domestic buying

Source: Geojit Research, NSDL

In 2025, DIIs invested ₹4.87 lakh crore in the market, which helped balance out the ₹1.98 lakh crore withdrawn by FPIs. This led to a total net investment of ₹2.89 lakh crore. In August, FPIs withdrew investments worth ₹28,217 crore, indicating caution but DIIs responded with an investment of more than 2.4 times the FPI outflow.

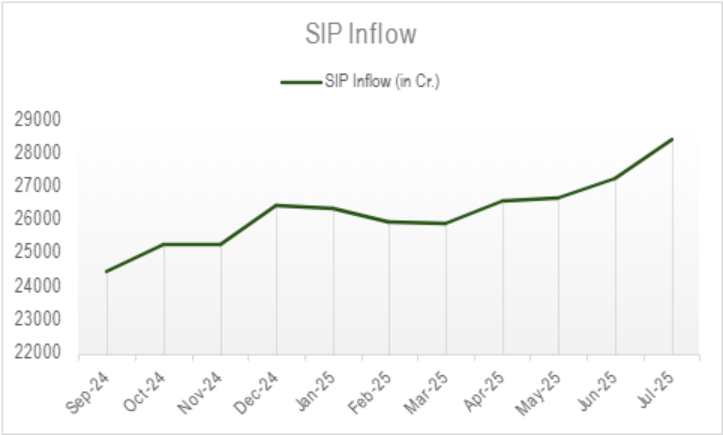

Amidst all these, equity oriented Mutual funds saw an inflow of 42,702 crore rupees, aided by monthly SIP inflows of 28,464 crore rupees.

Source: Geojit Research, AMFI

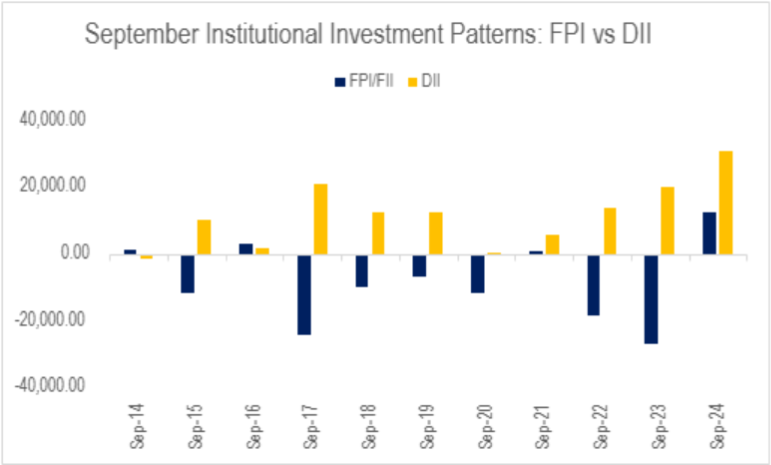

Seasonality – Institutional flows

Source: Geojit Research, NSDL

FPIs have pulled money out of the market in 7 of the last 11 Septembers, with the biggest withdrawal being ₹26,692 crore in September 2023. On the other hand, DIIs were positive in 10 of those 11 years, but they were able to fully balance out the FPI outflows only 4 times, including 2023 and 2024.

Seasonality – Nifty

In the last 15 years, the combined returns of July-August were less than 2% in seven years. In five of these seven years, the month of September delivered positive returns, with an average return of 5.15%. This gives us a 71% chance of seeing a positive return this September, with this year’s July-August months returning a combined 2.88% (data as of 26th August).

FII’s index future positions as a proxy

Source: Geojit Research, NSE

It has been usually seen that the proportion of index futures held by FIIs has given an indication towards FIIs’ market expectations. It has also been found that the extreme build up in either shorts or longs usually is followed by a reversal. At present only 10% of FIIs’ index future positions are held as longs. This is an extreme scenario. In March 2023, when index future longs went below 30%, the downward trend in Nifty accelerated, but a few days after the proportion hit 8.3, Nifty started the reversal, as FIIs started covering their short positions. However, it is difficult to predict how soon the reversal will play out. It must be noted that the extreme positioning has come with a reason, and not just an anomaly which needs a correction. The extreme position is evident because FIIs’ outlook on Indian markets is negative. It may take a while before the bearish view plays out entirely, or the FIIs are proved wrong. For all we know, we are at an extreme position, with FIIs’ index future long proportion remaining at around 10% or below for over 18 days now, and that a reversal is possible soon.