In a bold shift in trade policy, the United States has placed industrial metals under intense scrutiny in 2025, with President Donald Trump imposing sweeping 50 percent tariffs on aluminum and steel imports. Copper, initially spared, has now joined the list under review and faces similar levies. These measures mark a strategic pivot toward protectionism, aimed at countering the global oversupply of subsidized Chinese metals. While the move is designed to bolster domestic production and secure supply chain independence, it threatens to ripple through key sectors such as automotive, manufacturing, and consumer goods, potentially driving up costs and straining resilience. As the world’s largest economy recalibrates its priorities, the long-term implications for global trade and industrial competitiveness remain to be seen. These tariffs are poised to reverberate through US industrial production, inflationary pressures, and overall economic competitiveness, raising critical questions about the long-term costs of strategic decoupling in an interconnected global economy.

The US remains heavily reliant on foreign sources for aluminum, importing nearly half of its total consumption, and an even greater share of the specialized, high-purity aluminum essential to precision-driven industries. A significant portion, approximately two-thirds, of primary aluminum imports originates from Canada, where lower energy costs make production more economical. Key sectors such as aerospace, electronics, and defense, which depend on high-grade aluminum, are already contending with elevated costs due to an existing 25 percent tariff. The newly imposed 50 percent duty is expected to intensify these pressures, potentially undermining the U.S. defense industrial base by raising the cost of critical military components, including aircraft structures and lightweight armor plating, at a time when global security challenges are mounting.

Although domestic steel mills supply roughly 75 percent of the US’s steel consumption, the country remains significantly reliant on foreign imports for specialized steel products, particularly seamless pipes and tubes engineered to withstand extreme pressures and temperatures. These materials are vital to sectors such as energy infrastructure, oil and gas drilling, aerospace, and large-scale construction. With approximately 40 percent of piping and rolled steel products sourced from abroad, the newly imposed tariffs are expected to escalate costs for US oil producers. This could lead to a slowdown in drilling activity and a rise in fuel prices, compounding inflationary pressures across the broader economy.

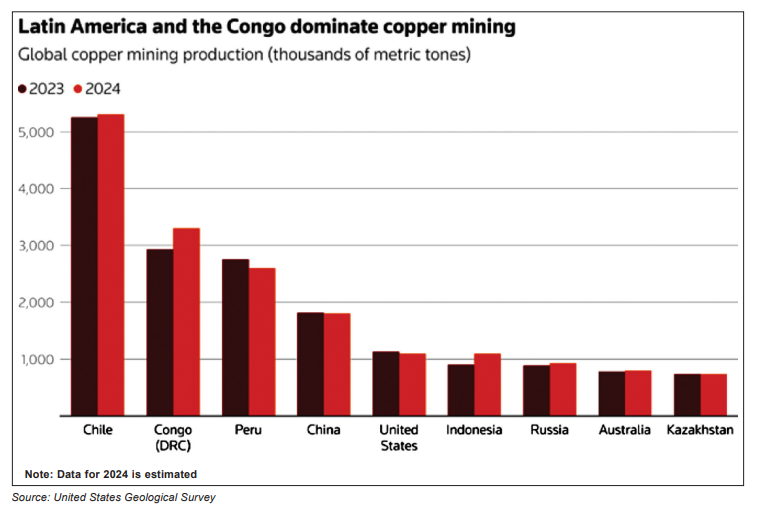

Beginning August 1, President Trump will implement a 50 percent tariff on copper imports, aligning the metal with the elevated duties placed on steel and aluminum earlier in June, up from the previous 25 percent. The escalation of tariffs on copper, a metal critical to semiconductors, electric vehicle batteries, renewable energy systems, and data infrastructure, marks a strategic turning point in US trade policy. Despite possessing substantial copper reserves, the US continues to lag in smelting and refining capacity compared to global competitors. Roughly half of the refined copper consumed domestically is imported, with Chile accounting for 65 percent, followed by Canada, Mexico, and Peru.

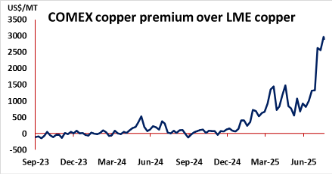

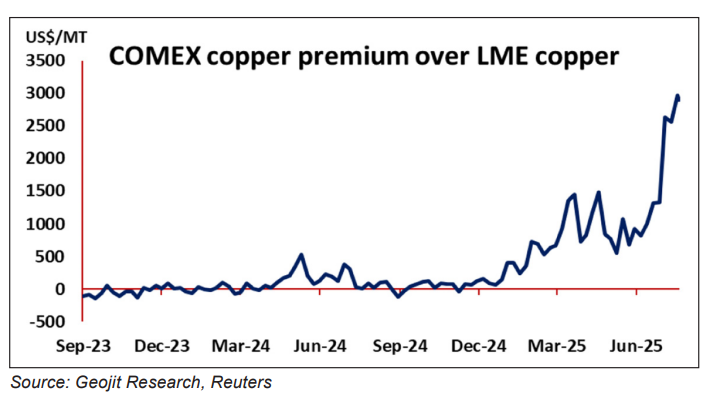

This tariff hike brings copper in line with the duties already imposed on aluminum and steel, reinforcing a broader protectionist framework. However, the market reaction has been swift and dramatic. Following the announcement of the copper import tariff, the arbitrage between COMEX and LME copper futures widened significantly. COMEX copper surged to an all-time high, trading near $5.80 per pound, while LME three-month copper futures hovered around $10,000 per metric tonne. This divergence pushed the premium of COMEX over LME copper to an unprecedented level of $3,000 per metric tonne, the largest arbitrage spread ever recorded. This unprecedented spike in COMEX prices reflects deep investor concern over constrained supply chains and rising production costs, with ripple effects expected across key US industries such as construction, advanced manufacturing, and electric vehicle production.

Domestically, the long-stalled Resolution Copper Mine in Arizona, backed by Rio Tinto and BHP, has the potential to supply up to 25 percent of US copper demand. However, it remains entangled in regulatory hurdles and opposition from environmental and tribal groups. Meanwhile, efforts by the Biden administration and the EU to diversify supply chains, such as the $1 billion investment in the Lobito rail corridor connecting Zambia and the Democratic Republic of Congo to Angola, aim to counterbalance China’s dominance in African resource extraction. Yet such infrastructure investments are long-term in nature and unlikely to ease near-term supply disruptions or pricing pressure.

According to projections by British research firm BMI, global copper mine production is expected to grow by 2.5 percent in 2025, with a compound annual growth rate (CAGR) of 2.9 percent through 2034. While this signals steady expansion in output, it falls significantly short of meeting the surging global demand driven by the accelerating transition to clean energy, electric vehicles, and digital infrastructure.

The International Energy Agency (IEA) warns that, even with this projected growth, global copper supply will only satisfy about 70 percent of expected demand by 2035. This looming supply-demand gap is likely to keep copper prices elevated over the long term, placing upward pressure on production costs across a wide range of industries, from construction and transportation to high-tech manufacturing and renewable energy deployment. The persistent shortfall underscores the urgency for investment not only in mining but also in refining and recycling infrastructure to ensure a stable and sustainable copper supply chain in the years ahead.

While the newly imposed tariffs may offer short-term insulation for US producers against foreign competition and reinforce the narrative of strategic autonomy, they also risk introducing significant economic distortions. Rising manufacturing costs, heightened inflationary pressures, and potential erosion of competitiveness in key sectors could offset the intended benefits. Without a parallel expansion in domestic processing capacity and accelerated approval for resource development projects, these protectionist measures may ultimately prove counterproductive. As the global economy pivots toward electrification and green technologies, which are heavily reliant on metals like aluminum and copper, the long-term cost of protectionism may soon outweigh its strategic advantages.