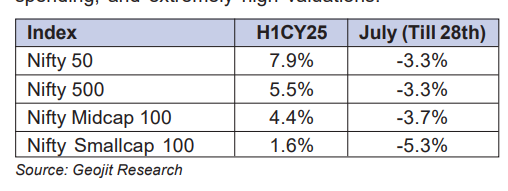

In H1 CY2025, the Indian stock market rebounded after the subdued H2 CY2024. The rally intensified from April onwards with a rise in large caps. The Nifty50 has posted a solid return of 7.9%, while the broader market advanced by 5.5%, reflecting a resurgence in domestic economic momentum. GDP growth accelerated to 7.5% in Q1 CY2025, up from 5.6% and 6.4% in prior quarters. This was largely due to a resumption of government spending and moderation in input cost, leading to a 10–12% YoY rise in broad corporate earnings, and a slight upgrade in future expectations.

Global headwinds have also eased, lending further support to India’s market recovery. The 90-day suspension of reciprocal tariffs announced in April helped de-escalate trade tensions, while geopolitical stability in the Middle East contributed to a decline in crude oil prices and mitigated supply risks. Investor sentiment improved, and market volatility dropped sharply, with India VIX falling from 22.8 to 12.8 between 7 April and 30 June. To sustain this momentum, a lot will depend on India-US trade talks and Q1 earnings. However, the market has a positive view regarding Free Trade Agreements (FTAs), as the US is expected to avoid aggressive tariffs to prevent high domestic inflation.

India’s corporate earnings outlook remains cautiously optimistic, as FY26 projections stand at 10–13%, with Q1 FY26 expected to begin on a softer note, showing a 5–7% YoY increase. Earnings are anticipated to strengthen in the subsequent quarters, supported by a favourable base effect, potential interest rate cuts, improved financial liquidity, and resilient consumption trends. Mid- and small-cap segments are expected to lead the next phase of the market rally. Importantly, Q1 results should deliver an upgradation in earnings potentials as valuation concerns persist with Nifty50 at 21.2x forward P/E, a 3-year high. Subdued domestic inflation is likely to lead to further interest cuts, which is good for equities.

H2 could be good for mid and small caps

After a subdued start to the year, the Indian equity market began to show signs of recovery as the consolidation phase—initiated in September 2024—neared its end by April 2025. This shift in trend was catalysed by easing pressures on both the global and domestic fronts. Globally, the challenges included the tariff war, geopolitical tensions, high inflation, and slowdown in the world economy. While in India it was a fall in corporate earnings, subdued government and private spending, and extremely high valuations.

As the risks moderated during the year and the broad market factored in the challenges by correcting about 21% during the period, the market started to recover. As India’s corporate earnings started to rebound in Q1CY25, and signs of further growth, the market responded positively. Nifty50 provided a return of 8.8% in H1, while the broad market underperformed.

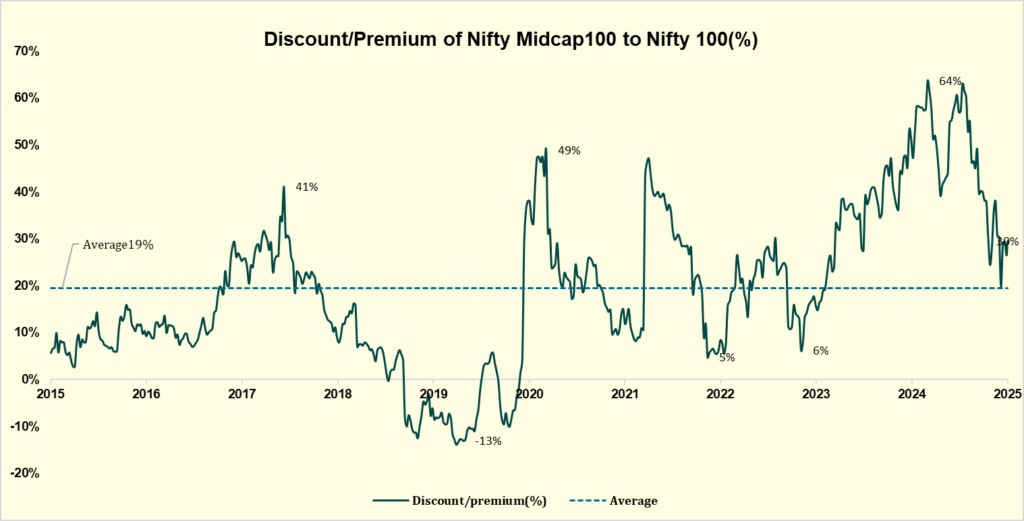

In H1 CY2025, the recovery was led by large caps, while mid and small caps struggled due to premium valuation and earnings downgrades. The presence of FIIs and retail investors has fallen in the last 2-3 quarters. We can expect a reversal in the mid-caps trend during H2 as premium valuations have corrected and the earnings growth cycle has improved with traction in the broad economy. Moderation in inflation (CPI in June at 2.1%), a fall in interest rates, and a rebound in urban and rural spending are expected to be positive for mid and small caps. It can ignite investor enthusiasm in the future as the global and domestic economies recover when global risks ease and the domestic economy continues to grow.

Source: Geojit Research

Sectoral Rotation

| Sectoral Index | H1CY25 Return (%) |

| Nifty Financial Services | 16.2 |

| Nifty Infrastructure | 11.7 |

| Nifty Metal | 11.2 |

| S&P BSE Capital Goods | 7.3 |

| Nifty PSE | 7.2 |

| Nifty India Manufacturing | 5.8 |

| Nifty FMCG | -1.9 |

| Nifty Media | -3.5 |

| Nifty Pharma | -5.5 |

| Nifty Realty | -6.2 |

| S&P BSE Consumer Durables | -7.1 |

| Nifty IT | -8.7 |

Source: Geojit Research

Rate sensitives like finance and infrastructure rebound faster due to better valuations below the long-term averages, and direct benefit of cheaper rates, accommodative RBI policy, and recovery in government spending. In contrast, sectors like automobiles and real estate saw a delayed recovery, gaining momentum only in the latter part of H1 CY2025 due to premium valuations earlier on and uncertainty surrounding tariffs impacting OEMs and ancillary players. Metals benefitted from a rise in the interactional prices, due to the imposition of a 25% US tariff, and improvements in the Chinese economy, thus reducing the domestic supply threat. These sectors, including manufacturing, are expected to do well on a long-term basis. Weakness was in export-oriented sectors like IT and pharma due to weak US spending and uncertainty on the impact of tariff on medicines. However, further correction looks limited as valuations have become attractive for a long-term investor.

Anticipation around the finalization of a Free Trade Agreement (FTA) has lifted sentiment, with US equity markets trading at new highs—factoring in the big budget, expected rate cuts, and increased fiscal spending. These developments could provide a positive spillover effect for Indian export sectors, especially as global trade dynamics stabilize.

The consumption sector—particularly FMCG and consumer durables—is emerging as a key area of interest in India’s equity landscape. After a period of underperformance, the sector is showing signs of revival, driven by a rebound in both urban and rural spending. Additionally, decline in input cost is expected to boost margins, and valuations are attractive on a long-term basis, which can provide further traction in H2. Similarly, Realty looks promising; however, it needs to be stock specific given the high valuation on a short-term basis.

We expect H2 to be better than H1

We began CY2025 with a Nifty50 target of 26,300, which we are now modestly revising upward to 26,500, reflecting improved earnings visibility and a more constructive outlook heading into CY2026. Looking ahead, we introduce our December 2026 target for Nifty 50 at 28,500, based on a forward P/E of 20x. This implies an absolute return of ~14% from the closing level of 24,968 as on July 18, 2025.

Following the rally between April and June 2025, the market is consolidating in July. This is because of muted Q1FY25 results, uncertainties around the implementation of tariffs, FII selling, and the premium valuation of India. To move ahead, two things need to be sorted out. One, the Q1 results should improve after the subdued start; importantly, it should provide signs of upgradation in the future. Because to sustain this valuation at a 3-year high level, growth in earnings is a must. Currently, market consensus leans toward an optimistic outlook, anticipating a recovery in earnings during H2 CY2025.

Secondly, clarity is required on the implementation of the trade deal with the US. While uncertainties persist, market sentiment remains broadly positive, with the consensus view that India will be relatively less impacted by tariffs compared to other economies. This optimism is partly driven by the belief in the so-called “TACO” (Trump Always Chickens Out) effect where aggressive trade measures are often softened, postponed, or reversed to avoid domestic economic fallout, particularly inflation. The US equity market is already pricing in favourable outcomes, trading at new highs on expectations of budgetary expansion, rate cuts, and increased spending. However, there is a short-term risk that the “TACO rally” may be overextended, especially given the elevated valuations in emerging markets and the lack of concrete policy clarity. Markets cannot rally on political reversals alone; fundamental earnings growth and macro stability are essential for continued upside.