Last month, after a short walk in the hot and humid weather of Mumbai, while walking past a bustling market, I stopped by a local juice vendor. He had two big jars on display – one labelled “Fresh Juice – INR 50” and another, more modest one, labelled “Juice + Ice – INR 30.”

I asked him what the difference was. He replied, “Same juice, sir. But the Rs. 30 one has more ice. Looks full, feels full, but you get less juice.” Since I just was looking to quench my thirst and feel refreshed, I opted for the INR 30 drink.

It struck me how often life – and investing – is exactly like that. We’re constantly offered versions of the same thing, dressed up differently, and with varying outcomes. The real trick is knowing what you are actually getting, especially when it comes to risk and returns.

This got me thinking about a conversation I recently had with my parents.

My parents, like many from their generation, built their financial lives around simplicity. In the 90s, Fixed Deposits ruled. They had a system: staggered tenures, money-back insurance, and regular savings. No fancy spreadsheets — just discipline and trust in guaranteed returns.

Over the years, their understanding evolved. Friends nudged them into equity mutual funds. And fortunately, they stayed put — riding out volatility and eventually earning solid long-term returns.

Still, what truly helps them sleep at night peacefully is their fixed income portfolio. Something about that “assured returns” gives a different kind of comfort. When I speak to them today, their investment queries are no longer about “where to invest,” but rather:

“कितना टक्का पैसा रिस्क में है और कितना टक्का सेफ वाला है?” (“How much of the investment is exposed to risk, and how much is safe?”)

“टैक्स कटने के बाद कितना मिलता है?” (“How much do you get after tax?”)

Simple, but smart questions. And to be fair, these are the very questions all investors—retired or not—should be asking.

The Dilemma:

But here’s the problem: the fixed income space doesn’t feel the same anymore. With FD rates hovering lower than the double digits my parents once enjoyed, many conservative investors feel they are fighting a losing battle.

Fixed income mutual funds also took a backseat post 2020, thanks to the equity bull run. And the 2023 budget’s removal of indexation benefit from debt mutual funds only made things worse from a post-tax return perspective.

The New Answer?

Amid this shift, something interesting has emerged: Income Plus Arbitrage Fund of Funds (FoFs).

Launched more actively since April 2025, these hybrid funds blend the best of two worlds:

- ~35% is allocated to arbitrage strategies—positions in equity that aim to be risk-neutral.

Here’s the clever part: Because arbitrage strategies are technically equity investments, if you hold the fund for over 2 years, your capital gains are taxed at just 12.5% (long-term capital gains rate), rather than your marginal income tax rate, which for many is 30%.

In essence, by adding just a little “equity ice” into the mix, investors can enjoy better tax efficiency—without taking full-blown equity risk.

As of now, there are 14 such Income/Debt Plus Arbitrage FoFs in the industry:

- 3 new ones launched in June 2025.

- 3 launched earlier in FY26.

- The rest have restructured older strategies into this newer, smarter approach.

Exhibit 1

Source – Morningstar Direct, AUM as of May 2025.

Exhibit 2 – Returns scenario for a 2-year period

| Debt Fund | Income Plus Arbitrage FOF | |

| Invested Amount | 1,00,000 | 1,00,000 |

| Assumed Return p.a | 7.50% | 7.50% |

| End of Period Value (2-years) | 1,15,563 | 1,15,563 |

| Pre-Tax Gains | 15,563 | 15,563 |

| Tax Applicable excl surcharge & cess | 30.00% | 12.50% |

| Tax | 4,669 | 1,945 |

| Post Tax Gains | 1,10,894 | 1,13,617 |

| Net Return (Post Tax) | 5.31% | 6.59% |

Tax applicable excludes cess and surcharge. For illustrative purposes

Undoubtedly, the post-tax return feature is the most compelling selling point of this new ‘Income Plus Arbitrage Fund’s, and for good reason. The difference can be easily more than 1% more than a regular debt fund considering similar returns. Additionally, a lower expense ratio can also potentially add to some incremental alpha getting generated over regular stand-alone debt fund. That said, it is important to note that investing in FOFs will also incur an additional expense of the underlying funds in addition to the FOF’s expense itself.

How different are these funds in their approach –

Based on the current holdings (May 2025), some AMCs have taken a simple approach of having a combination of 2 funds to align with the Income Plus Arbitrage FOF strategy. Whereas, on the other hand, some AMCs have relied on a combination of multiple funds.

Exhibit – 3- Underlying Funds

Baring DSP, all other AMCs have opted to have a Corporate Bond as one of the underlying debt funds in their Income Plus Arbitrage FOF offering.

Among these funds HSBC and Axis have taken unique approach towards creating their funds. HSBC has opted for a combination of multiple underlying funds across various categories to create their offering. Axis has on the other hand opted to have schemes of other AMCs including their own to form their offering. Apart from Axis, all other fund houses have their own underlying funds as a combination of their offering. One has to bear in mind that, these strategies can change over time and the underlying funds could see some change.

Underlying Debt Portfolio Approach.

This is primarily the element where fund managers would focus all their endeavour towards generating superior returns. In most funds, the underlying papers are primarily geared towards the AAA segment. Therefore, in all likelihood there could be elements active duration plays to garner returns. Taking a look at the maturity profiling gives us further insight-

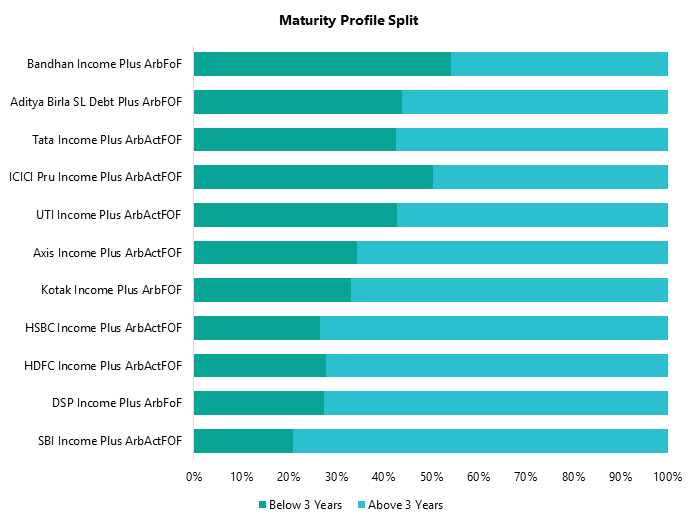

Exhibit 4 – Maturity Profile Split (Rebased to 100%)-

Source – Morningstar Direct. Portfolio as of May 2025. Fund name modified for easier representation.

Splitting the underlying maturity papers of each fund into 2 buckets (Below 3 years and Above 3 years) and rebasing the allocation towards 100% show which funds are having a lower average maturity (eg: Bandhan Income Plus Arbitrage FOF and ICICI Pru Income Plus Arbitrage FOF) and which funds have higher maturity. Funds which have a higher allocation towards a maturity profile above 3-years in-turn also have higher elements of duration play towards generating return.

Exhibit 5 – Avg Maturity and Mod Duration Mapping

Source – Morningstar Direct. Portfolio as of May 2025. Fund name modified for easier representation.

From the table above, it can be seen that in funds where the average maturity is above 5-years the Mod Duration too is also at a slightly higher number relative to others. This can work advantageously during falling interest rate scenarios. Investors should therefore also look into these aspects before investing into any or a combination of these funds and ensure it is in alignment with their risk profile and goals. Clearly none these portfolios are optimally not designed to be invested for less than 2 years, which investors should make a note off.

This is an evolving yet new category of funds which are at their inception stage and hence it would not be right to measure their performance so soon. It deserves more time. Nevertheless, pleasingly it is an important “innovation” by fund houses to give fixed income investors a fresh new lease of life.

Final Thoughts

As always, I’ll like to have a cricketing analogy for this new interesting segment of funds.

For years, debt mutual funds enjoyed a sweet spot — like batting with a slightly shorter boundary (indexation benefit). Even if the scoring wasn’t flashy, the post-tax outcomes looked reasonably good for the risk taken.

But then the rules changed — the boundary was pushed back (indexation removed), and suddenly it got a lot harder to score clean runs in the traditional way. That’s when Income Plus Arbitrage FoFs walked in. Think of it like this: the bowler just overstepped after making life tough for the batsman — and now the batsman can swing freely on a free hit, thanks to equity taxation. It’s not a windfall — it’s a tactical response to a tough delivery. These funds are converting a rule change setback into a clever opportunity, combining debt-like safety with a surprise shot at equity-style tax gains.

1 comment

What if someone’s marginal income tax rate is lower than 30%? Wouldn’t debt fund still provide better return in the illustrated case?