The Indian capital market is constantly evolving, and with it, the range of investment products available to both High Net Worth Individuals (HNIs) and retail investors has expanded significantly. For retail investors, there has arguably never been a better time in terms of the variety and accessibility of investment options.

In the realm of equity investing, individuals can choose to invest directly in stocks or opt for the fund route. Within funds, they can adopt either an active or passive approach—such as investing in index funds or Exchange Traded Funds (ETFs). These options can be further customized by choosing diversified or sector-specific funds, market cap-focused strategies, or thematic investments. Simply put, investors today have a wide array of choices to build portfolios aligned with their personal investment styles and goals.

Interestingly, within the passive investment universe, there has been significant innovation over the past several years. Building on traditional choices, investors now also have access to more sophisticated strategies like factor-based and smart beta funds. While these two may appear similar, there are important nuances that distinguish them.

Factor-based funds are broader in approach and focus directly on specific investment factors such as value, momentum, size, quality, and volatility. These funds are generally market-cap weighted or use fundamental weighting and often aim to isolate pure factor exposures.

On the other hand, smart beta funds use alternative, rules-based weighting methods instead of traditional market-cap weighting. These funds systematically tilt portfolios towards factors like value, quality, and momentum while maintaining broad market exposure.

In India, low-cost ETFs that mimic broader indices—especially large-cap indices—have seen immense traction over the past few years, as the ability of active managers to generate alpha in the large-cap segment has declined. Recognizing this shift, index providers have responded by launching a plethora of smart beta and factor-based indices, offering investors a richer and more nuanced set of options for portfolio construction.

Annexure 1

Source- ACE MF.

METHODOLOGY

Single Factor

Source: NSE

Computation of Single Factor score

Source: NSE. For arriving at the final selection & weight, factor level score and factor level percentile score needs to be considered.

Multi Factor Weights

Source- NSE. For arriving at the final selection & weight, factor level score and factor level percentile score needs to be considered.

Typically, schemes would have a cap of 20-50 names in the index as specified in the name. As a risk management, allocations to singular stocks will generally not exceed more than 5%. Lastly, most of these are re-balanced every 6 months (June and December).

PERFORMANCE

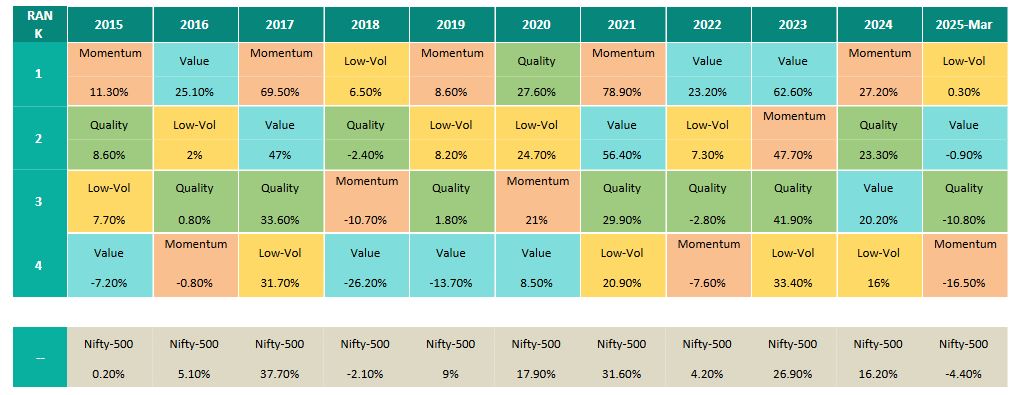

Annexure 2: Performance Analysis (CY)

Source- ACEMF, Data as on 31st March 2025. Outperformance v/s BSE 500 TRI = Green.

For our analysis, we chose to benchmark these funds against BSE 500 TRI. While we understand that, some of the underlying funds may belong to a certain segment (large, mid or small cap) specifically, we have chosen to focus on the factors as opposed to market caps.

Judging these funds purely from a return’s perspective, it is quite evident that most of these factors tend to outperform the broader Benchmark (BSE 500 TRI) convincingly during bull market-phases. That said, its corollary is also true. During volatile periods (e.g. 2022), the performance was disappointing.

However, as we all know, returns are just one aspect when it comes to analysing a fund. When we look at how these factors perform during volatile periods, it gives us a clearer understanding of the (potential) risks.

Annexure 3: Average Max Drawdown

Data- Morningstar Direct, Data as of March 2025. Outperformance v/s BSE 500 TRI = Green. Max Drawdown- A portfolio’s maximum loss in a peak-to-trough decline before a new peak is attained. Average of Max Drawdown considered for the period considered.

As the above table shows, when it comes to protecting the downside risk, the factors funds tend to be less resilient than perhaps what one expected. This is possibly on account of two main factors. Firstly, the factor going out of favour in the market and second, the concentrated nature of the indices (funds) which leads to a higher volatility relative to the benchmark which is broad based. While this can work in favour of the funds during rising markets, it could also make the funds underperform during volatile periods.

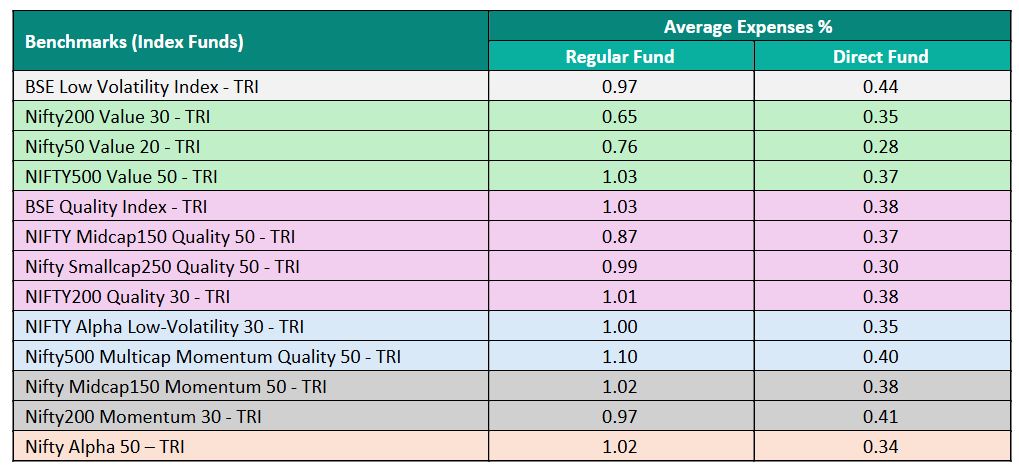

EXPENSES

Compared to simple broad based index funds, factor funds and smart beta funds tend to have a higher expense ratio which eventually eat up into returns.

Annexure 4: Expenses (%)

Source- ACEMF.

OTHER FACTORS

There are also important factors like tracking errors, flows and rebalancing actions which influence the overall returns. But in this article, we chose to approach this segment of investing from a first principal basis. In all fairness, most of the factor based & smart beta funds have had a very short history. Equity investments, as always should be looked at from at least a 5-year horizon or a full investment cycle and from that perspective, only a handful of these funds have been in existence for that long.

It is no secret that investment styles and factors go through cycles. Therefore, it would be a prudent approach for investors to consider factor-based investing / smart-beta investing as a tactical or satellite allocation of their portfolio rather than core.

Annexure 5: Style Analysis of Factors

Geojit Insights. Data as of 31ST March 2025.

From a positioning perspective, investors could consider the approach as:

- Defensive approach- Low Volatility & Quality

- Persistence/ Bull markets- Momentum

- Cyclical approach- Value & Size.

As like with all my earlier articles, I would like to give a cricketing analogy to this. Smart beta or factor-based investing is like practicing batting using an automated bowling machine. You can tweak the machine to deliver specific types of balls—fast, swinging, short-pitched—based on the conditions you want to train for. Similarly, factor investing lets you tilt your portfolio toward specific traits like momentum, value, or low volatility. It’s systematic, low-cost (like index funds), and designed to help you build muscle memory (or returns) around specific patterns in the market. But just like in real matches, real-life bowlers mix it up—Yorkers, Bouncers, Slower balls—and pitch or weather conditions can change unexpectedly. So, while smart beta strategies are great for targeted training, they don’t adapt mid-innings. That’s where active funds come in—like an experienced coach adjusting your game plan in real time, dynamically managing your portfolio based on current market conditions.

The investing world constantly witnesses debates between active funds vs passive funds where folks belonging to each camp make compelling arguments in their favour. We, however, look at each segment objectively and see if the product is a right fit in a client’s portfolio. To us, it is not a question of either-or but rather a question of “how much of each and where they best fit”. Every investor’s needs, goals, and risk tolerance are different, so we focus on constructing a well-balanced portfolio where active and passive strategies can complement each other, depending on the market conditions, asset class, and client objectives.