Just imagine turning a monthly investment of just Rs. 20,000 into a retirement fund of nearly Rs. 2 crore in 20 years. Now, picture using the same money to receive a steady monthly income for the next 20 years. Sounds too good to be true, right? Let’s explore the powerful combination of Systematic Investment Plans (SIP) and Systematic Withdrawal Plans (SWP) – the dynamic duo of wealth creation and preservation. Let me show you how it worked for Maya, a 35-year-old software engineer who has always dreamed of financial freedom.

Maya, like many young professionals, found the world of investing overwhelming until a Saturday morning coffee with her uncle Ravi, who is a certified financial planner. “Investing is a lot like planting a tree,” he said, reclining in his chair. “You can’t expect fruits on the first day, but with patience and the right approach, you’ll have a harvest that lasts generations.”

Ravi explained the magic of SIP using a simple example. “Imagine you’re filling a piggy bank, but instead of just saving, you’re investing smartly. Every month, you invest a fixed amount into equity mutual funds. Some months, when markets are low, your money buys more units. Other months, when markets are high, you buy fewer units. Over time, this averages out your cost per unit, reducing the impact of ups and downs in the market.”

Maya was interested to know more. “How much difference can a small monthly investment really make?” she asked.

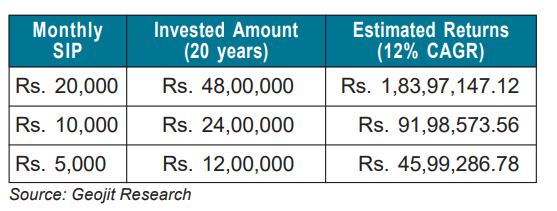

Ravi pulled out a compelling chart that made Maya’s eyes widen. “Look at this,” he said. “If you invest just Rs. 20,000 every month for 20 years, assuming a 12% return, you could turn Rs. 48 lakhs of total investments into nearly Rs. 2 crore. That’s the power of compounding – where your money grows and then the growth creates more growth.”

See how different monthly SIP amounts can grow over 20 years, assuming a 12% return:

The above is for illustration purposes only. The SIP amount, tenure of SIP and expected rate of return are assumed figures for the purpose of explaining the concept of the advantages of SIP investments. The actual result may vary from the depicted results depending on the scheme selected.

The numbers seemed almost magical. Maya understood this wasn’t about getting rich quickly, but about consistent, disciplined investing. SIP wasn’t just a method of investing; but it was a financial habit that could transform her future.

But Ravi wasn’t done, though. He introduced her to the second part of the financial puzzle: Systematic Withdrawal Plans (SWP). “Think of SWP as the harvest phase,” he explained. “Remember that tree we talked about? SWP is like carefully picking fruits without cutting down the entire tree. Your investment keeps growing while you withdraw a set amount of money each month.”

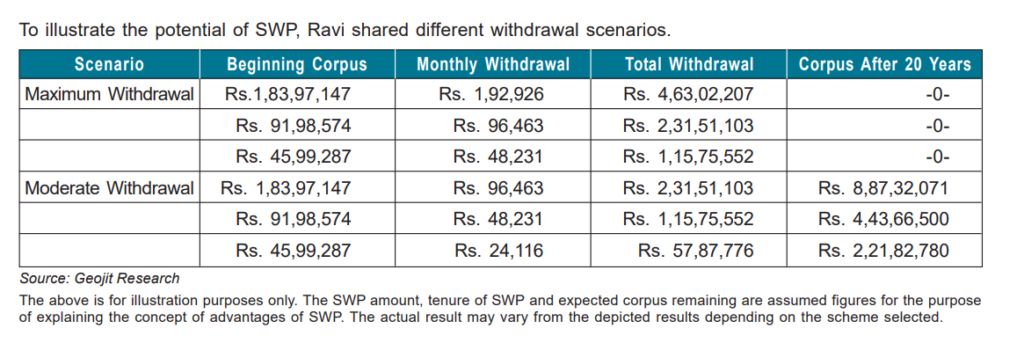

The above is for illustration purposes only. The SWP amount, tenure of SWP and expected corpus remaining are assumed figures for the purpose of explaining the concept of advantages of SWP. The actual result may vary from the depicted results depending on the scheme selected.

“Look at this table, with the corpus of Rs. 1.83 crore, you could withdraw a maximum of around Rs. 1.92 lakhs monthly for 20 years. This approach uses up all your savings in 20 years,” explained Ravi.

The secret, Ravi emphasized, was maintaining balance. “Don’t withdraw too aggressively,” he said. “A moderate withdrawal rate lets your money keep growing, providing a buffer against inflation and market uncertainties. For example, if you choose to withdraw about Rs. 96,000 monthly for 20 years instead of Rs. 1.92 lakhs, you will still have around Rs. 8.8 crore remaining! This happens because your money keeps growing even as you withdraw.” Ravi added.

Maya learnt that financial planning wasn’t about complicated strategies or massive lump-sum investments. It was about consistency, patience, and smart choices. She decided to start her investment journey right away!!

This is not a story about getting rich overnight. It was about understanding that wealth creation is a journey, not a destination. SIP and SWP are trusted companions on this journey – while SIPs are ideal for building wealth during earning years, SWPs are equally important as they help you manage wealth distribution during retirement years. Success lies in finding the right balance between how much money you take out and how long you want your money to last.

For young professionals like Maya, and those planning their retirement, the message is clear: Start early, invest consistently, and plan your withdrawals carefully. In a world of economic uncertainties, SIP and SWP offer a path to financial independence and peace of mind.

As Ravi always says, “Financial freedom isn’t about how much you earn, but how wisely you save and invest.” Ready to start your investment journey? The best time to start growing your money is today.