Earnings growth is the pivotal factor in India’s stock market landscape. In Q3, earnings grew by 10%, which is almost half of the current one year forward valuation of 19x. However, this marks an improvement from the 6-7% YoY growth recorded in Q1 and Q2. Encouragingly, economic indicators and corporate commentaries suggest further improvement in Q4, driven by higher government spending and rising urban demand. If earnings growth moves closer to India’s long-term average of 15%, it could support a recovery in the domestic stock market, which has been undergoing a five-month correction. India’s FY26 earnings are expected to grow at 12-13%, better than the 7-8% estimated for FY25.

Another positive development is the trade agreement between the US and India. If effectively implemented over the next 6-7 months, it could help shield India from the adverse effects of the ongoing tariff war. President Trump is considering implementing country-specific reciprocal tariffs, a policy that contradicts WTO regulations and poses a risk to global trade stability. However, if India secures a waiver under the proposed US trade policy, it could strengthen the domestic economy and support long-term real GDP growth of 6-7%.

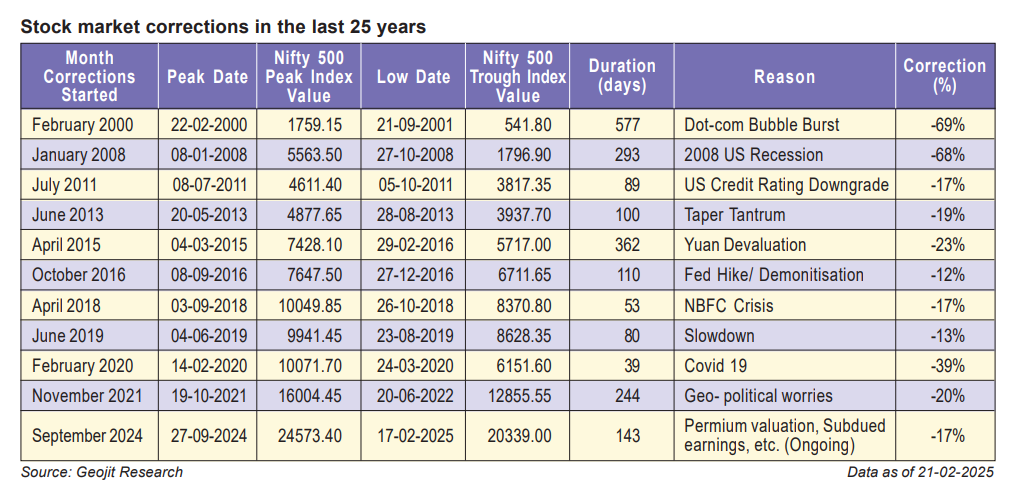

Stock market corrections in the last 25 years

Over the past 25 years, India has undergone eleven market corrections, each triggered by a combination of global and domestic factors. The most severe downturns were the dot-com bubble and the 2008 global financial crisis, which led to a two-thirds decline in the Nifty 500 index due to the widespread disruption in global financial markets. The Covid-19 pandemic was the third largest market shock, causing a 39% decline. However, its impact was relatively brief, lasting just 39 days, as swift fiscal and monetary interventions helped stabilize global financial markets and limit further downside for investors.

The fourth-largest market correction occurred in 2015, primarily driven by global economic factors. The key trigger was the turbulence in the Chinese stock market, where the devaluation of the Yuan led to a 43% decline in the SSE Composite Index within two months, sparking a global sell-off. Additional pressures came from Greece’s debt default and the conclusion of quantitative easing in the US. This brought about a correction of 23% in the Indian broader market.

Apart from these four major events, the remaining market corrections ranged between 12% and 20%, lasting anywhere from 53 to 244 days. The relatively limited impact of these downturns was due to their lower intensity and the absence of structural disruptions to the global economy. In most cases, it was a niche problem affecting a section of the world economy and financial markets, like a drop in financial liquidity, short-term inflation, or high valuation.

The last correction was in 2021, which was initiated by global inflation mainly due to supply chain disruptions caused by Covid-19 and the Russian-Ukraine conflict. Nifty500 corrected by 20%.

The current challenges, though disruptive in the short to medium term, are unlikely to destabilize the global economy. It is a culmination of tapering, high valuation, and low earnings growth. A new uncertainty added to the non-structure issue is the imposition of US tariffs, which is likely to affect world trade.

Greater clarity is anticipated regarding the US administration’s full intent, as such measures could also negatively affect the US economy. The strategy appears to be inflationary, driving up prices and manufacturing costs within the US However, it remains unclear whether the US is fully committed to implementing reciprocal tariffs, over the actual enforcement and its negotiation-driven approach. Moreover, the likelihood of retaliatory measures from other countries could further impact the US economy.

Trade talks with the US and hopes on Q4 results

India’s trade talks with the US (Modi-Trump) are a surprising development. It gives us hope that the future tariff imposition to be placed by the US on the rest of the world will have a lower effect on India. The market is still sceptical about this, as the US is still contemplating deploying reciprocal tariffs on all countries on an item wise basis. With the US accounting for 26% of the global economy and being the world’s second-largest exporter, the enforcement of such tariffs could significantly impact global economic growth. If implemented, these measures could disrupt international trade and create further economic uncertainty.

However, India has positioned itself advantageously by swiftly initiating trade talks, which are expected to be finalized and implemented within the year. In the budget, India reduced tariffs on segments like auto, auto parts, aircraft, energy storage, precious metals, EV batteries, and others to make it a balanced playing ground for US imports. India is attempting to increase imports from the US in areas like defence and crude to balance the deficit and increase the total trade to $500bn by 2030 from $200bn in 2023.

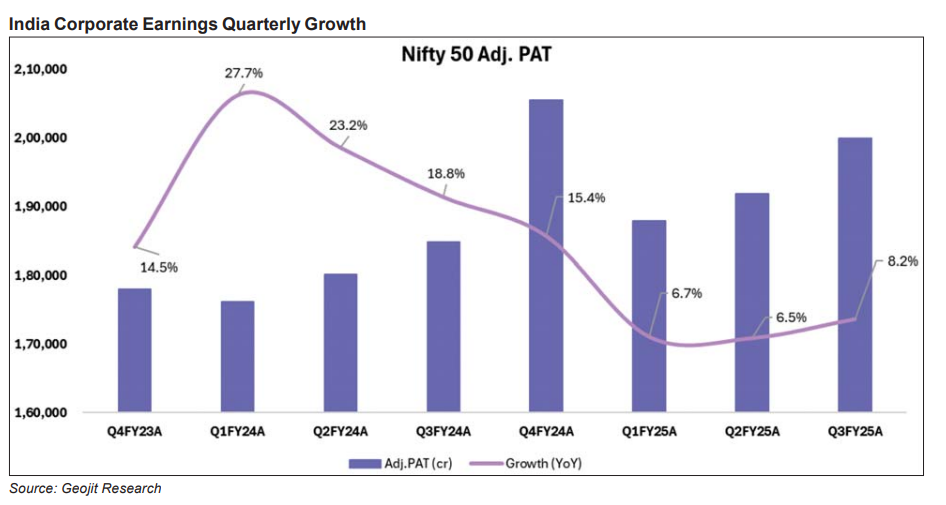

India Corporate Earnings Quarterly Growth

Source: Geojit Research

India’s corporate earnings growth has been declining since Q1. Nifty50 earnings were growing by more than 20% in FY24, which reduced to 7% in 9 months in FY25. The sharp contraction threatens the premium Indian valuation. Though the valuation has reduced in the last five months, the equal narrowing of the earnings keeps the valuation high at 19x one year forward.

Based on Q3, the market is hopeful of corporate growth recovering. Nifty50 adjusted earnings have improved to 8.2% in Q3 from 6.5% in Q2. The broader market reported PAT growth improving to 10%. Importantly, the narrative is that Q4 will be better than Q3, led by a rise in government spending and urban demand. It is a bit early to forecast the Q4 number, but indications point to about 12-13% earnings growth. The recovery can balloon in FY26 based on a reduction in the trade war and a stable domestic economy. Currently, consensus estimates suggest a growth of 12-13% in FY26 from 7-8% for FY25.

With inflation easing, interest rates stabilizing, and a steady domestic economic outlook, the Indian stock market’s prospects appear positive. If earnings growth rebounds toward 15%, market trends are expected to improve during the April to September quarter, reinforcing investor confidence and supporting a more favourable investment environment.

1 comment

Realistic and appropriate research work done.