Prospects opening for medium-term rally

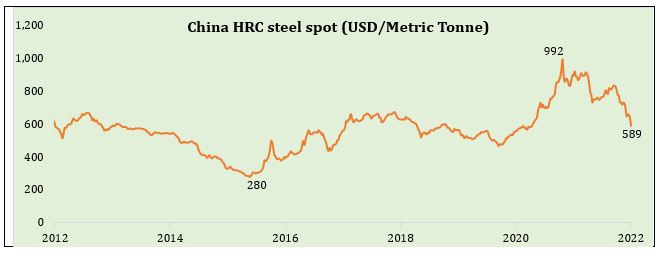

We feel that henceforth, the outlook of Fed policy may not be as pertinent as it was during the year. Because much of the hostile view has been factored in the world financial market while future worries on inflation are moderating. We feel that the market can do better in the second half of 2022 if commodity prices continue to moderate, especially crude. A big caveat is if the war escalates, and inflation increases the situation will change. But we see a strong possibility of inflation being brought under control if the world economy reverts to old norms by re-opening, the relaxation of China’s covid-zero tolerance policy, slowdown in war effect, and slowing economy. This can trigger a rally in the equity market on a medium-term basis.

Much is factored in by the market price

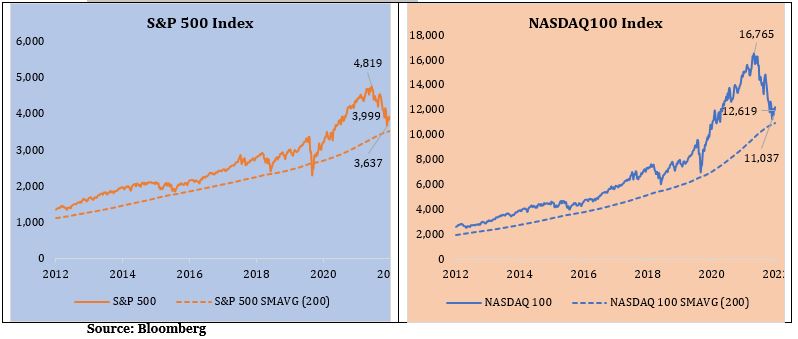

The correction of the world equity market has been humongous. MSCI World index fell by 25% from the 52week high to the 52week low. For example, the world’s main equity market, the US, corrected heavily during the year. Broad indexes like S&P500 fell by 25% while the technology based Nasdaq100 index was down by 35%. Today they are hovering with a slight positive bias up by 10% to 15% from their 52 week low, respectively. They are still lucrative when purely reviewed on a price basis, down by 17% to 24% from the respective all-time high and trading near the long-term averages.

The two reasons for the correction were hawkish monetary policy due to stubborn inflation and fear of recession. An assessment of the current situation shows that these two risky points are moderating in anticipation of a rapid fall in inflation and a change in policy in the future.

Hope of stability in the financial market

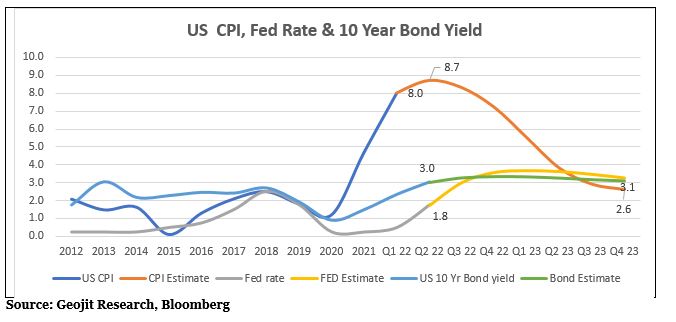

World inflation is expected to fall steadily in H2CY22 and CY23. This is due to a strong clampdown on commodity prices, which were elevated from 2020 to 2022 because of supply constraints and high liquidity.

US CPI is expected to fall rapidly in the next four quarters, indicating that, hostile policy may not be required in 2023. As a result, bond yield is expected to stabilise, and trade in a range of 2.5% to 3.5%, which rapidly increased from 1.5% to 3.5% in 2022.

The caveat is that, firstly, the scenario does not factor in a serious recession but a mild one. Secondly, the Indian market will benefit from the correction in commodities, but it is a concern for the global bourses due to fear of a slowdown in the world economy. Hence, the investors will have to remain cautious due to the possibility of fizzling out of this rally in the medium-term because of the limited upside in valuation. Nevertheless, we are more positive about the Indian market in the short to medium term and expect sectors like FMCG, consumption, and auto to do better than the market.

Indian market is trading at reasonable valuation

Indian market is trading at one year forward P/E of 18x, just above the 7 years average of 17x. It is reasonable, not expensive, and cheap. A slowing economy limits a strong upside in valuation, hence a lot will depend on corporate earnings growth for the stock market to sustain the current positive trend. The downside of valuation is also protected in anticipation of a sharp fall in inflation but the actual outcome whether a mild or strong recession will defence the valuation trend. We should also understand the fact that the 7year valuation trend escalated due to the bull rally from July 2020 to Dec 2021 despite a low earnings base.

We are positive about the Indian market in a medium-term basis, due to the sharp correction in commodity prices, especially crude. We can see an opportunity for an upside as FII selling can moderate during the year. This is highly possible if crude prices are correct further, and the US bond yield stabilizes, which has reduced from 3.5% to the current 2.9%.

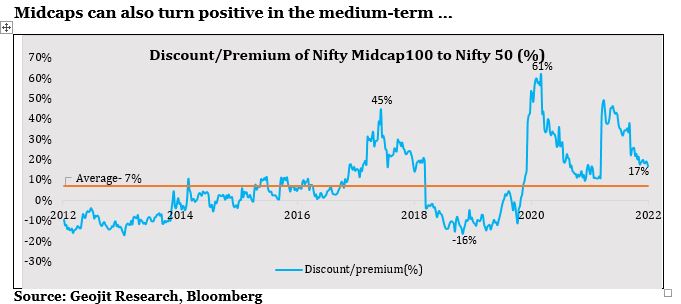

Midcaps can also turn positive in the medium-term …

The premium of midcaps increased to 61% during 2020. It has reduced to 17% as on 19th July 2022. On a long-term basis, the Nifty midcap 100 index, has an average premium of 7%. We feel that this premium will increase during the year as the domestic market improves. The valuation of midcaps has corrected from 35x to the long-term average of 22x. We believe that they will trade on the higher side compared to large caps in the medium-term due to better earnings growth. But as investors, we should continue to be stock specific, while investing in midcaps by sticking only with quality names. Overall world equity market continues to be neutral with a feeble sentiment.