India has been experiencing a sustained FII risk-off trend since late 2024, which has further intensified amid the energy crisis and escalating geopolitical tensions in March. Investor sentiment weakened further as uncertainties around the duration of the conflict weighed on the domestic growth outlook. Heavy FII outflows, coupled with profit booking by retail investors and a moderation in buying by DIIs, collectively amplified the decline in equity markets.

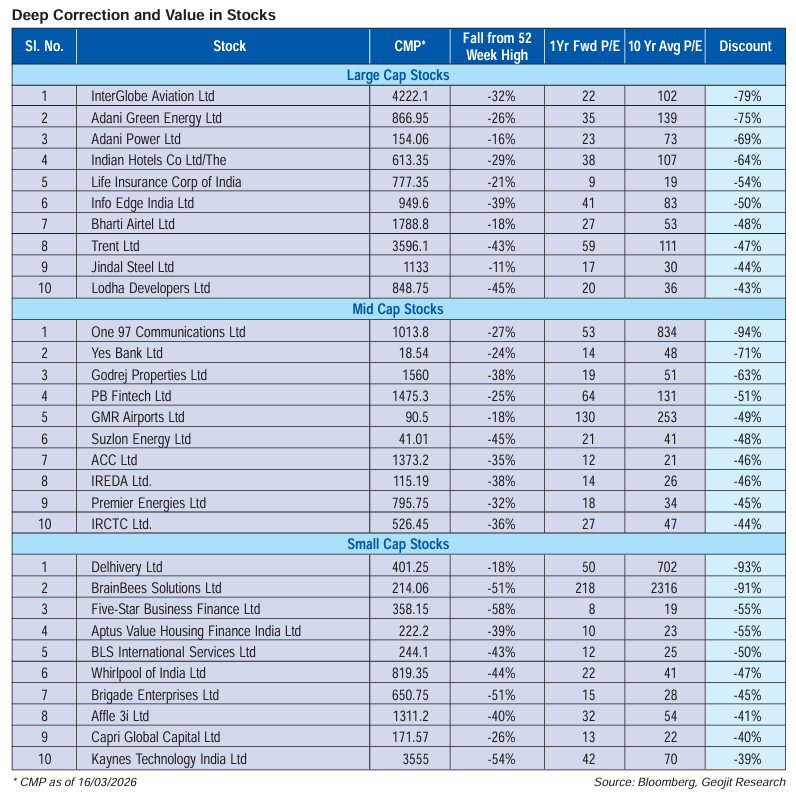

As a result, India’s market valuations have undergone a meaningful correction toward the lower end of their 5-year range, after historically trading at a premium supported by strong macro fundamentals and robust domestic investor participation. This correction places the market in a more favourable position for a healthy rebound, contingent on the assumption that the ongoing geopolitical conflict remains short-lived. Notably, several rated stocks have seen sharp declines in both prices and valuations, as reflected in their 52-week performance, creating selective opportunities for investors.

At the same time, the absence of clear signals from either side on a resolution to the conflict keeps uncertainty elevated, leaving room for further market correction or consolidation. On a 10-year valuation basis, India’s markets do not yet appear sufficiently attractive to warrant a strong rerating. Additionally, the extent of damage to oil infrastructure in the Gulf region raises the risk of persistently elevated oil and gas prices in the short to medium term, which could lead to earnings downgrades and, in turn, pressure on valuations.

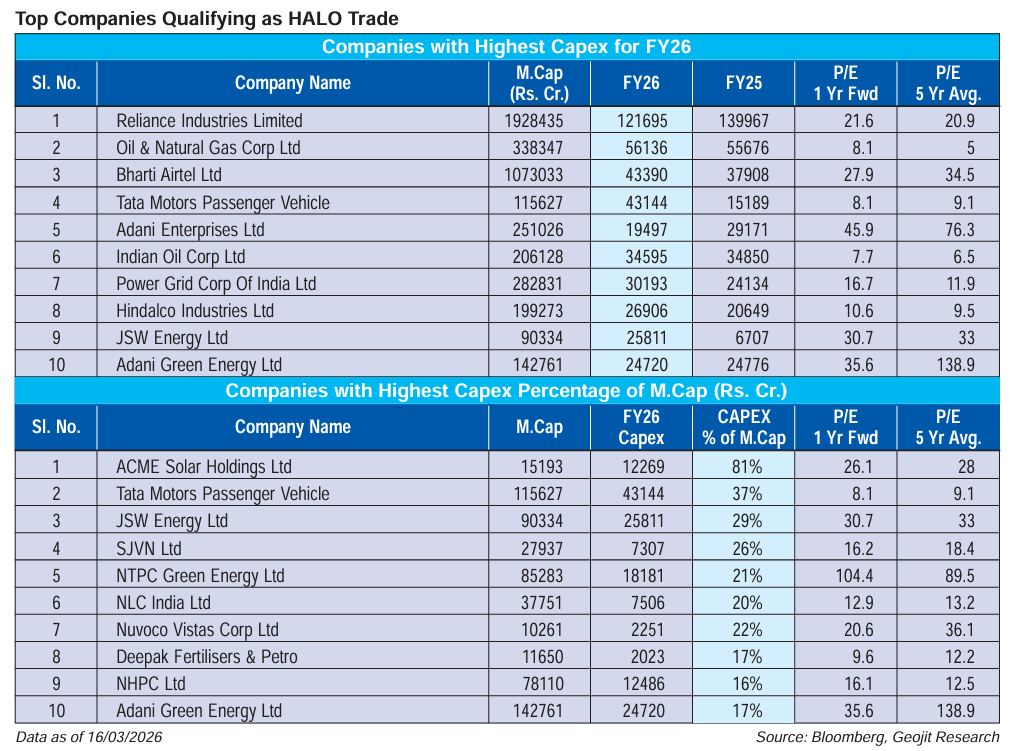

In this evolving environment, a notable shift in investment strategy is emerging through the “HALO Trade”—an approach focused on Heavy Assets and Low Obsolescence. This framework emphasizes companies with strong tangible assets, durable business models, and lower vulnerability to rapid technological disruption. Gaining traction in markets such as Japan, the HALO theme is as relevant for India as it reorients toward capital-intensive growth in manufacturing and advanced industries.

World politics and crude oil surge: The epicentre of market anxiety

Global equity markets are currently undergoing a phase of heightened volatility, driven by a combination of geopolitical tensions, inflationary pressures, and uncertainty around global growth. Investor sentiment has weakened significantly as markets grapple with a rapidly evolving macroeconomic environment. A key trigger behind this shift has been the escalation of tensions involving the US, Israel and Iran, which has disrupted global stability and triggered a broad-based risk-off sentiment. The conflict has intensified concerns around energy security, trade disruptions, and inflation, leading to capital outflows from emerging markets and a shift toward safer assets. As a result, global equities have turned volatile, with investors adopting a cautious stance amid rising uncertainty.

One of the most immediate consequences of the geopolitical escalation has been the sharp spike in crude oil prices. Oil prices have surged nearly 30% in a short period, reaching levels of around $115–117 per barrel, marking the steepest rise in recent years and still staying above the threshold level of $100. Lately the surge is attributed to the tug of war between the US and Iran to open or gain control over the Strait of Hormuz. The trend will dramatically change based on the ongoing outcome, which is hoped to be the last phase of the disruption. Nevertheless, given the high degree of damage in the oil infrastructure of the Gulf region, there is a risk that energy prices will stay elevated in the short to medium-term, which poses a major macroeconomic challenge for India, importing about 90% of its oil requirement.

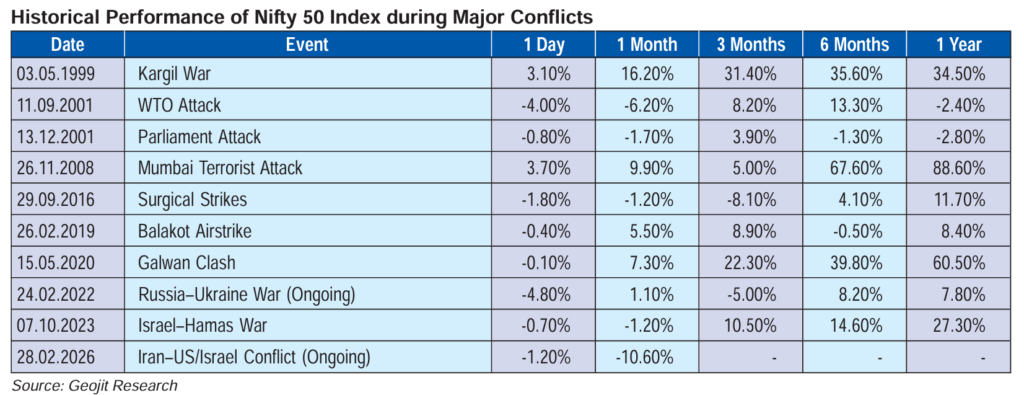

History states that war-related corrections bring opportunities

The ripple effects of global uncertainty have been strongly felt in Indian equity markets. The level of impact is based on the tenure of the war, global financial & economic risk, and volatility of crude. The Iran war has impacted India given its high vulnerability to oil prices and energy availability. India was already in the phase of consolidation due to trade issues, selling in tech, and FIIs’ risk-off strategy. Nifty50 has fallen from its 52-week high of 26,373 down by ~15%, indicating the depth of the overall correction.

Despite intermittent recoveries driven by value buying, the broader trend remains volatile and uncertain in the near term. The correction has led to a meaningful moderation in valuations based on the history of 5 years’ valuation. Indian equities, which were previously trading at a premium compared to other emerging markets, have now seen this premium narrow considerably.

However, it is important to note that valuations are not yet deeply discounted based on 10 years of data, as they still reflect the strong earnings expectations and structural growth narrative associated with India. While the correction has reduced downside risks, further market direction will largely depend on geopolitical developments, global liquidity conditions, and downgrades in earnings. If the Iran war is short-lived, the risk of a cut in earnings will be low, and will support a rebound in the market.

Mid- and small-caps positions and sectoral impact

Correction has been broad based; however, the impact has been more pronounced in the mid- and small-cap segments. These stocks had witnessed significant outperformance over the past year, driven by strong domestic inflows and optimistic growth expectations. As a result, they were trading at elevated valuations relative to historical averages. With the onset of global uncertainty and FII outflows, these segments have seen sharp declines, underperforming large-cap indices. The moderation in domestic inflows and declining risk appetite have further accelerated the sell-off effect. While the near term outlook remains weak, the correction has begun to create selective opportunities for long-term investors, particularly in companies with strong fundamentals and niche market leadership.

The ongoing market environment has led to a divergence in sectoral performance. Energy-intensive sectors such as aviation, paints, and chemicals are facing significant cost pressures due to rising crude prices. Similarly, sectors dependent on global demand are witnessing subdued sentiment amid concerns of a slowdown. On the other hand, defensive sectors such as pharmaceuticals and IT have shown relative resilience, benefiting from stable demand and currency tailwinds. Core sectors such as power, utilities, and infrastructure are also witnessing supportive trends, driven by domestic demand and government spending.

What makes halo stocks relevant in India?

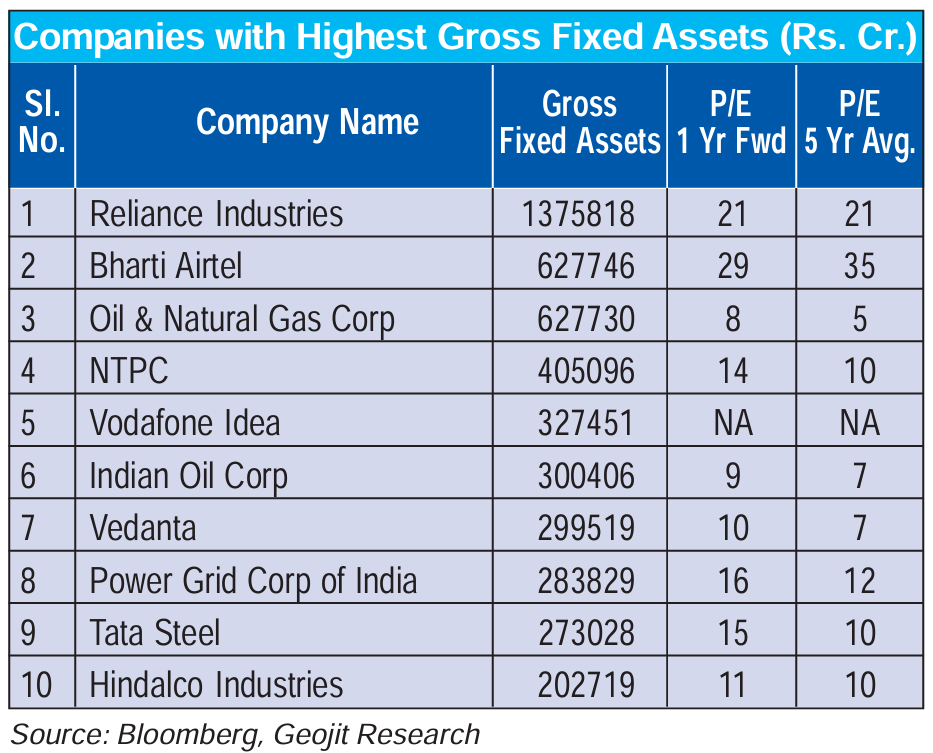

In this evolving global landscape, a new investment framework—the HALO Trade—is gaining prominence. HALO, which stands for Heavy Assets, Low Obsolescence, focuses on companies with strong tangible assets and lower susceptibility to technological disruption. This strategy has gained traction in markets like Japan, which has attracted substantial foreign inflows in recent months. Investors are increasingly favouring companies with durable asset bases, stable business models, and long-term earnings visibility, particularly in an era marked by rapid technological change and uncertainty. HALO trade will also bring importance to core sectors such as power, metals, mining, infrastructure, and industrial manufacturing. These businesses benefit from strong asset backing and are less vulnerable to rapid obsolescence, making them attractive in volatile market conditions.

Necessity of India’s strategic transition from asset-light to asset-heavy

India’s corporate landscape has traditionally been characterized by an asset-light model, marked by high return on equity, efficient capital allocation, and limited capital expenditure. While this approach has supported profitability, it may need to evolve in the context of a rapidly changing global economy. To remain competitive, India will need to increase investments in future-ready sectors such as advanced manufacturing, electronics, semiconductors, and robotics. Government led capex has already gained momentum, but private sector participation remains crucial for sustaining long term growth.

Several traditional sectors are undergoing transformation. Oil marketing companies are diversifying into renewable energy, while core sectors such as metals, power, and mining are adopting greener and more sustainable practices. These shifts align well with the HALO framework and highlight the potential for India to emerge as a key player in the global industrial ecosystem.

Emerging opportunities in halo-aligned sectors

Looking ahead, key investment opportunities in India are expected to emerge in sectors that combine strong asset bases with long-term growth visibility. These include advanced manufacturing segments such as industrial machinery, electronics, and semiconductors, as well as specialty areas like data centres, specialty chemicals, and industrial gases. Within the mid- and small-cap space, companies with niche leadership and strong competitive advantages are likely to outperform over the long term. Investors are increasingly focusing on businesses that demonstrate resilience, scalability, and the ability to adapt to technological changes.

While the HALO trade offers a compelling investment framework, it is not without risks. These businesses typically require high capital investment, which can impact cash flows and returns in the short to medium term. Additionally, rapid technological advancements could still pose obsolescence risks, even for asset-heavy industries. Valuations also remain a concern, as many HALO stocks are trading at elevated levels due to strong investor interest. Furthermore, a shift in market preference back toward asset-light models or changes in global liquidity conditions could impact the sustainability of this theme.

In short, a key underlying outcome of the war history is that it is usually short-lived. The presumption of the Iran war is also based on the same thesis along with understanding the political impulsions of the nations. None are in a position to endure a long war. If the presumption is true, the deep correction in March will open up a chance of strong rebound in the short to medium-term. At the same time, we need to realise the importance of companies and industries holding deep long-term value by building and growing high amount of tangible assets. Companies with heavy investment in new technology and up coming areas in India will hold advantage as long-term wealth is generated. A caveat we need to note is that such companies trade at premium valuation, but this correction has brought that risk down, opening opportunities.

Disclaimer: This article is only our view on the market and the impact it may have on sector specific stocks cited therein, which are only by way of examples. Certain stocks included in the article may not be within our coverage and are only used for illustrative purposes. For those stocks which are within our coverage, for General disclosures and disclaimer: please visit: https://www.geojit.com/gil/research-disclosures