A relentless rally in copper prices that began in the second half of 2025 gathered extraordinary momentum toward the end of the year and spilled powerfully into early 2026, pushing the metal to fresh record highs. LME copper surged past USD 14,000 per tonne in late January, up nearly 17% since the start of the year, before a sharp pullback reminded markets of the volatility underpinning the move. The surge was fuelled not only by tightening supply conditions but also by mounting uncertainty over potential United States tariffs on refined copper, a weakening dollar, and a resurgence of fund-driven speculation across the base metals complex. In China, speculative fervour was particularly intense, with trading volumes in the most active Shanghai Futures Exchange (SHFE) copper contract soaring to a record 1.5 million tonnes, lifting prices above CNY 114,000 per tonne. As the dust settles, the key question for 2026 emerges: can this record-setting rally be sustained? While structural supports such as constrained supply, tariff risks, and expectations of looser monetary policy remain intact, the extreme volatility of the past two months raises doubts. Understanding how these structural factors interact with speculative forces will be central to assessing copper’s trajectory in the year ahead.

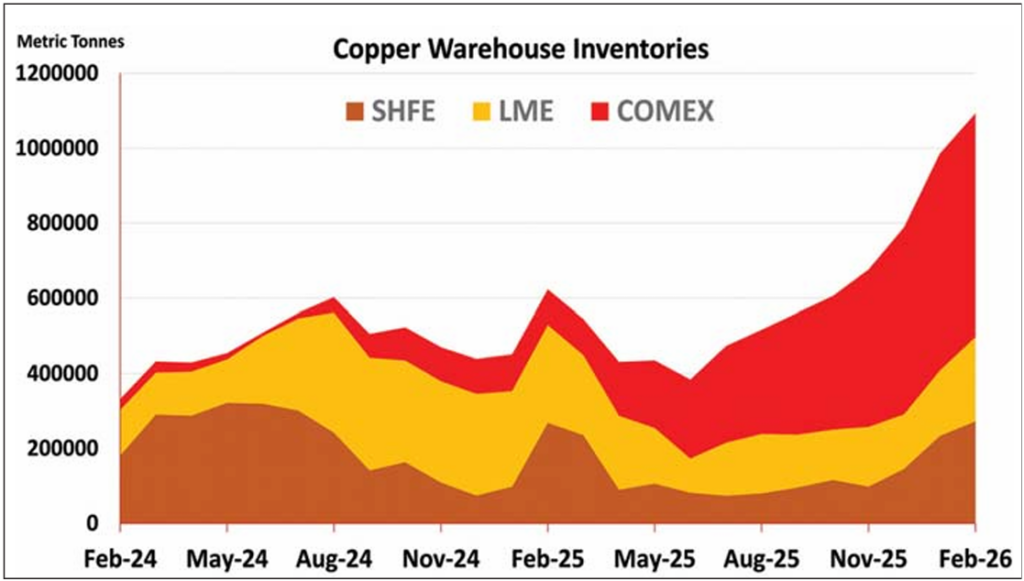

On the London Metal Exchange (LME), copper stocks have climbed to 224,650 tonnes, marking an increase of more than 50% since the start of the year. The buildup in available material has pushed the LME market into a deeper contango, where the cash contract trades at a discount to the three-month forward contract. Recently, this discount widened to around USD 111.50 per tonne, the highest level seen in roughly a year. Such a structure typically reflects comfortable supply conditions and limited immediate demand. Inventory growth has been even more pronounced in China. Copper stocks in warehouses tracked by the SHFE have surged to 272,475 tonnes, representing an 87% increase year-to-date. The rise underscores slower-than-expected uptake from Chinese manufacturers at a time when seasonal restocking usually begins to pick up. Meanwhile, COMEX copper inventories in the United States have surged to 595,518 tonnes, exceeding the combined stock levels of both the LME and SHFE. With this jump, global visible copper inventories have surpassed the one-million-tonne mark, a level considered ample by historical standards. Overall, the rapid accumulation of copper across major exchanges highlights a temporary mismatch between supply and demand. Ample stocks are weighing on the prompt market, reinforcing contango spreads and raising questions about the timing of demand recovery in key consuming regions.

The global refined copper market posted a preliminary surplus exceeding 300,000 tonnes in 2025, as elevated prices and heightened economic uncertainty curbed demand growth. Looking ahead, concerns are mounting about the impact of record high prices on consumption in China, the world’s largest copper consumer. Demand has already begun to soften, with SHFE copper settling at CNY 100,260 per tonne ahead of the Lunar New Year holidays, marking a monthly decline in February and erasing much of January’s gains. Even with the recent correction, prices remain historically elevated and continue to weigh on buying interest. Beyond price pressures, China’s ongoing housing market slowdown and weak manufacturing activity are expected to further dampen demand across traditional end use sectors. Meanwhile, growth in green energy-related consumption is likely to moderate, particularly in the solar industry, following recent pricing reforms. Power sector reforms introduced in China in 2025 eliminated the guaranteed rate of return previously offered to renewable energy projects, requiring projects commissioned from June onward to sell electricity at market-determined prices. The shift has introduced greater uncertainty for investors who had long relied on fixed pricing mechanisms to secure predictable returns. As a result, global copper demand growth is expected to recover at a more moderate pace in 2026.

Looking ahead, persistently low treatment and refining charges (TC/RCs) are expected to continue squeezing smelter margins in China, the world’s largest producer of refined copper, significantly increasing the risk of output cutbacks through 2026. This margin pressure reflects the ongoing mismatch between rapidly expanding smelting capacity and limited availability of concentrate, a trend that is unlikely to ease in the near term. At the global level, the copper market is already under considerable strain. Mine supply disruptions, sharply weakened refining margins and strategic stockpiling by the United States have collectively tightened conditions throughout the supply chain. These challenges are poised to extend into 2026, as refined copper availability remains constrained by persistent logistical frictions, policy driven shifts in supply management, and accelerating demand from electricity grid upgrades, defence manufacturing and the build out of AI-related infrastructure, sectors that require large volumes of copper.

Although scheduled mine expansion projects and the gradual reactivation of capacity idled in 2025 are expected to boost global mine output by around 2.3% in 2026, this increase will not immediately translate into refined copper supply. The conversion process, along with existing bottlenecks in smelting and refining, means that the bulk of this new material is unlikely to reach the refined market before 2027. As a result, while the refined copper market is likely to tighten substantially in 2026, a modest surplus may still persist, largely due to the slower than expected recovery in end use demand.