As finance professionals, we often find ourselves at odds with economists. Brilliant thinkers who have spent their lives studying how economies function, how capital flows, and how interest rates shape behaviour yet whose conclusions can sit uncomfortably with how markets actually move.

Investors often joke that no economist has ever become rich by predicting markets. While the joke may carry some truth, it also misses the point. Economists are not meant to forecast prices. They are meant to explain systems.

This piece requires us to wear both hats: that of the economist and that of the investor. It is an attempt to examine a topic that has surfaced repeatedly in recent discourse “De-dollarisation”. In simple terms, de-dollarisation refers to a gradual reduction in the use of the US dollar in global trade and financial transactions, and a corresponding decline in reliance on the dollar by nations, institutions, and corporations.

Readers familiar with our work will know that we prefer to approach complex ideas through structure rather than spectacle. Before diving in, it is worth laying out the framework we use to write about this subject:

- How the global monetary system works — Historically and Today

- The rise of the US dollar

- The subtle bends in the system

- Game theory in monetary arrangements and Gresham’s law

- What does all this mean for Indian investors

How the global monetary system works: Historically and today

Sometimes, the simplest way to understand how large systems function is to see them reflected in fiction through movies or web-series. Great content breaks complex concepts and ideas that feel abstract when encountered only in textbooks into simple explanations.

One such example appears, almost unintentionally, in the Netflix series Money Heist.

For those unfamiliar with the series, Money Heist follows an audacious plan by a group of thieves to remove Spain’s gold reserves from the Bank of Spain. What makes the plot compelling is not the scale of the robbery, but how differently its implications are understood. To the police, it is an extraordinary crime. To the Governor of the Bank, it is an existential threat. He alone grasps what it would mean if the world discovered that Spain no longer had its gold. Bond yields would spike. Confidence would evaporate. What begins as a heist could quickly turn into a sovereign crisis.

Later in the series, one of the thieves articulates the real leverage of the plan with unsettling calm: the gold itself matters less than the belief that it exists. As long as the world believes Spain’s reserves are intact, the financial system continues to function.

This idea comes full circle in a quiet exchange away from the guns and chaos. By then, the real gold is already gone. The vault still looks intact. The doors are sealed. The cameras work. To the outside world, nothing has changed. Only the Governor knows the truth that what sits inside the vault is no longer what it claims to be. And yet, the system holds.

The global financial system operates on a similar logic. For decades, the US dollar has anchored trade, reserves, and cross-border settlements not because it is scrutinised every day, but because it is assumed to be accessible, reliable, and broadly neutral. For most of the post-war period, that assumption held.

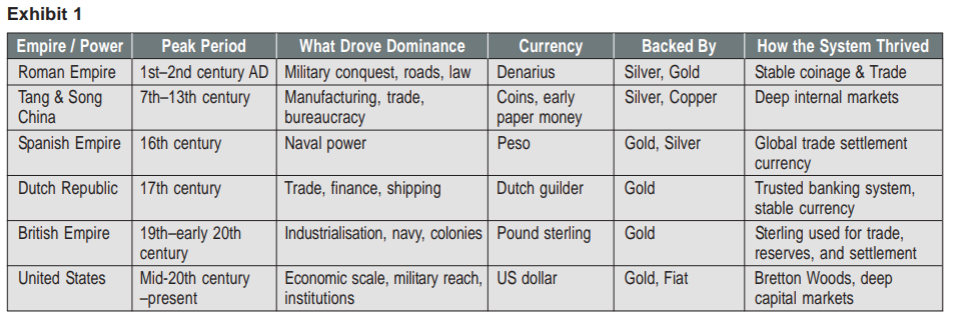

What history shows, even prior to US Dollar era is, every period of dominant trade has been accompanied by a dominant monetary system. The form has changed, but the pattern has not.

History also proves that no monetary order is perpetual. Each of these empires dominated not just for decades, but for centuries. Yet none proved permanent. Their influence faded as the conditions that once sustained it gradually changed. The pattern was familiar: the urge to expand territory led to expensive wars, persistent fiscal strain, and the growing use of money as an instrument of policy rather than trade.

The rise of the US Dollar

The dominance of the US dollar began to take shape in the aftermath of the Second World War, formalised under the Bretton Woods system. The arrangement was straightforward. Most global currencies would be pegged to the dollar, while the dollar itself would be convertible into gold at a fixed price of $35 an ounce. To reinforce confidence, several countries also chose to hold a significant portion of their gold reserves with the United States, further entrenching the dollar at the centre of the system.

This was also, in effect, a transition away from the pound sterling, which had anchored global trade during the height of the British Empire. For nearly two decades, Bretton Woods functioned with relative stability. By the late 1960s, however, pressure began to build. The costs of the Vietnam War, alongside expanding domestic programmes, led to persistent fiscal deficits.

In August 1971, President Richard Nixon suspended the dollar’s convertibility into gold, effectively bringing the Bretton Woods System to an end; called as the Nixon Shock. The dollar became a fiat currency and, by extension, so did most other major currencies.

Much like in Money Heist, what sat inside the vault was no longer what it claimed to be.

What followed, however, was not collapse. In the years that followed, the United States entered into arrangements with major oil-producing nations to price crude oil transactions in US dollars. As global trade expanded through the 1980s and beyond, oil became one of the most critical commodities in the world economy. To participate meaningfully in global trade, countries needed dollars not because of convertibility, but because of usage.

Just as important, the United States did not treat this privilege casually. Through much of the 1980s and 1990s, policy choices reinforced credibility. When inflation surged into double digits in the late 1970s, Paul Volcker, then Chairman of the Federal Reserve, raised interest rates into the high teens despite intense political pressure and the certainty of short-term economic pain. Fiscal discipline, while imperfect, remained a guiding norm rather than an afterthought.

Over time, this combination of deep markets, energy trade, and institutional restraint restored confidence. The dollar’s dominance no longer rested on gold, but on credibility, usage, and the perception of an independent, rules-based system.

The vault had changed. The doors were still sealed. And once again, the system held.

The subtle bends in the system

The first major stress test of the modern monetary system came during the global financial crisis of 2008. To prevent a full-blown collapse, extraordinary measures were deployed – quantitative easing, emergency liquidity facilities, and coordinated central bank action. The system bent, but it did not break.

The second shift came more quietly, fairly recently. As financial infrastructure became increasingly centralised and digitised, control over payment rails, settlement systems, and reserve assets became more visible. What had long been perceived as neutral financial plumbing began to reveal itself as leverage.

This became unmistakably clear in recent years, when certain nations saw portions of their foreign exchange reserves frozen. These actions were powerful, effective, and often justified within their specific contexts.

For countries not directly involved in these disputes, the message was less political and more practical. Trust in the system had long rested on the assumption of neutrality and continuity. What changed was not the dollar’s role, but the recognition that access could depend on alignment, compliance, or circumstance.

Once that realisation set in, behaviour began to adjust slowly and quietly.

Game theory in monetary arrangements and Gresham’s Law

To understand what is unfolding, it helps to step back and revisit a familiar idea from game theory. It is not about predicting outcomes, but about understanding incentives when decisions are interdependent.

Consider traffic at a busy intersection. No driver decides in isolation. Breaking the signal may help one car briefly, but if enough drivers do it, the junction locks up. The rational choice is not speed but avoiding a breakdown of coordination.

Countries behave much the same way. No nation makes decisions about trade, reserves, or currency settlement alone. Exiting a dominant monetary system abruptly may offer short-term autonomy, but done unilaterally it risks volatility, capital flight, or retaliation. Remaining fully dependent, once the system’s conditionality is visible, carries its own risks.

No country wants to be the first to exit. The costs are obvious. But no country wants to be the last either. The result is predictable. Everyone stays, but everyone hedges.

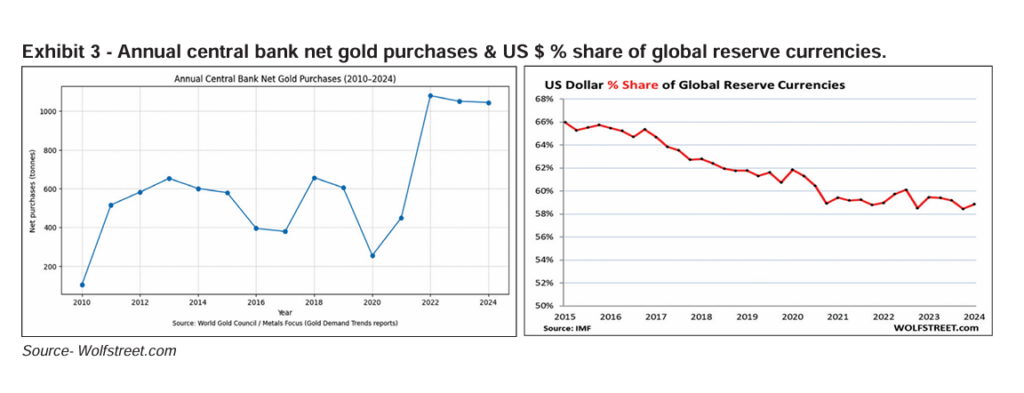

That hedging shows up at the margins. Bilateral settlement mechanisms are tested in small volumes through alternate currencies such as the euro or renminbi. Reserve diversification happens incrementally rather than dramatically—most visibly into gold.

Exhibit 3 – Annual central bank net gold purchases & US $ % share of global reserve currencies.

This behaviour echoes Gresham’s Law. When two forms of money coexist, economic actors tend to hoard what they trust and spend what they do not. The result is not confrontation, but substitution. Over time, the preferred asset moves out of circulation not because it has failed, but because it is being protected.

The dollar is not being rejected. It is being conserved. What gets misunderstood on this topic is- as long as using the dollar remains cheaper operationally, legally, and politically than the alternatives, behaviour will not change abruptly. What is unfolding is not a binary move away from the dollar, but a gradual rebalancing of dependence as the cost of unquestioned reliance rises.

What this means for Indian investors

India’s response to the shifting monetary landscape has been measured. The country continues to trade, settle, and hold reserves in dollars because the dollar remains liquid, efficient, and deeply embedded in global commerce. At the same time, India has expanded its options through selective local-currency trade arrangements, experimentation with alternative settlement mechanisms, and steady accumulation of reserves.

For Indian investors, this distinction matters.

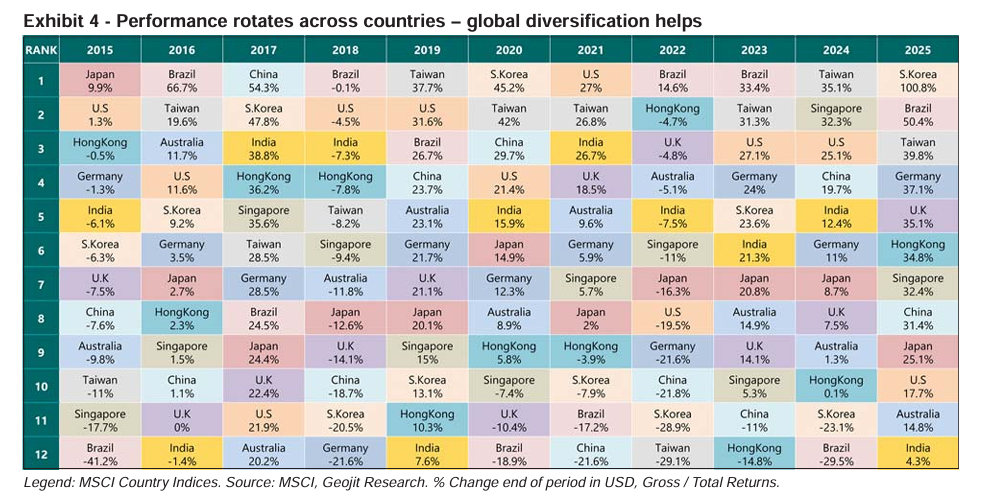

The case for global diversification remains strong, particularly exposure to the United States. The US continues to host the world’s most advanced technology ecosystem, its deepest capital markets, and many of the most globally dominant companies. Innovation clusters, institutional depth, and a sustained ability to attract global talent give the US an economic gravity that is difficult to replicate.

But global investing cannot be reduced to a single geography. Over the past few decades, few countries have matched Taiwan’s dominance in semiconductor manufacturing, and even fewer have rivalled China’s ability to scale manufacturing across industries. These are not marginal contributors to the global economy; they are foundational.

Legend: MSCI Country Indices. Source: MSCI, Geojit Research. % Change end of period in USD, Gross / Total Returns.

The implication for investors is straightforward. The opportunity set is global, and portfolios that remain narrowly domestic risk missing where value is being created.

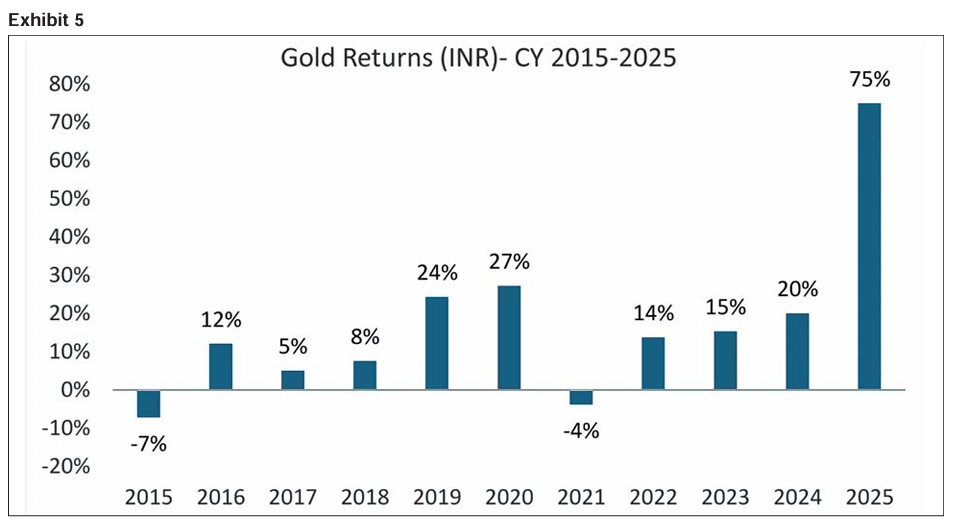

Thankfully, geographic diversification is not the only way to diversify risk. Periods of structural transition also tend to elevate the role of assets that sit outside financial and political systems altogether, and which have a low or no co-relation. Gold occupies a unique position here. It is no one’s liability, requires no counterparty, and does not depend on access to payment rails or settlement infrastructure.

Evaluating gold through the lens of cash flows and yields misses the point entirely. Gold is not meant to produce income; it is meant to preserve trust. If gold were as irrelevant as it is often made out to be, it would not have outlived empires, currencies, and financial systems over thousands of years.

Its relevance is not driven by fear or speculation, but by behaviour. As trust in systems becomes conditional, the appeal of assets that do not require trust increases quietly, and often without announcement but through steady returns and preservation of purchasing power.

This piece is not an attempt to predict how economies or markets will behave in the future. It is an effort to examine the global monetary system without alarmism, to recognise that subtle shifts are underway, and to ask a more practical question: how investors can respond thoughtfully.

In the end, the system still functions. The vault still looks intact. What has changed is not belief but the quiet preparation for a world where belief alone may no longer be enough.