Recently, Nifty made three attempts to surpass the all-time high recorded in September 2024. In the first two attempts, momentum faded amidst global headwinds and insufficient earnings traction. We think that the ongoing crossover looks more solid and could foster the enthusiasm in 2026 as trade uncertainty, geopolitical tensions, and domestic earnings growth become ensured. Global markets are increasingly expecting progress on US-China and US-India trade deals, driven by the view that the US economy cannot continue absorbing elevated inflation ahead of the 2026 midterm elections. The Trump administration has already begun reducing tariffs on key commodities to ease pressure on consumers. India has been rallying on expectations of a mid-level trade agreement; its short-term sustainability will depend on the fine print. A final tariff in the range of 10-15 percent is the number anticipated by the market, providing an imposing position for India amongst its Asian peers.

The domestic rally is also supported by better-than-estimated Q2 results by midcaps. Broad company results are in line with low double-digit growth of 10 percent, but midcaps category performance has been much better, around 20 percent, in the last two quarters. Importantly, domestic economy data (tax, inflation, and festival demand) and management narrative indicate bumper results in Q3. Additionally, confidence is gradually building that this momentum could extend into 2026, though the formalisation of the US-India trade deal is the key to strengthen these expectations.

On the downside, the current account deficit has widened, driven by weaker exports, and a depreciating rupee. Despite the muted performance of the stock market in 2025, India’s valuation never contracted. FII inflows have not improved in India. Wholesale inflation has reduced, indicating deflationary tends in the broader economy slowing business growth. Collectively, these factors imply that any near-term rally in Indian markets may face pauses at key checkpoints.

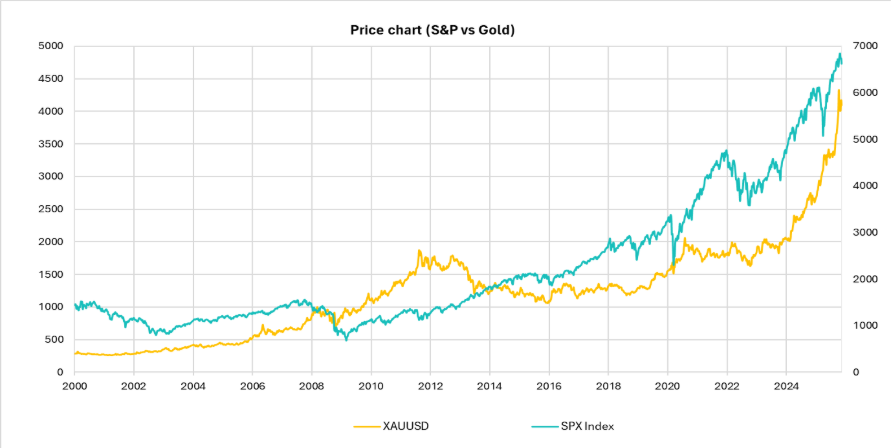

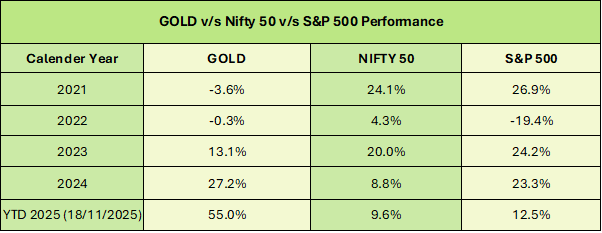

Gold is signalling why 2026 may prove to be more favourable for equities. After the international price soared 67 percent during the year—its strongest annual rally ever—the yellow metal is in a corrective mode. The inverse relationship between gold and equity has been strengthening, suggesting that a moderation in yellow metal prices could catalyse inflow for the stock market. Current trends suggest that a healthier economic backdrop in 2026 could trigger a meaningful shift to an equity-led cycle—one that was largely absent in 2025.

Gold’s rally: A three-year arc of geopolitics, monetary stress, and safe-haven demand

Since 2022, gold’s ascent was shaped by a confluence of geopolitical shocks and shifting monetary conditions. While the Russia–Ukraine conflict, which began on 24 February 2022, initially dampened global risk appetite, gold prices began reacting meaningfully only as the conflict intensified and new flashpoints emerged—most notably the Israel–Hamas conflict from 7 October 2023. These events revived demand for safe-haven assets, helping gold deliver 13 percent returns in CY23 and 27 percent in CY24 in dollar terms.

Central banks, especially in China and India, accelerated gold purchases during this period, reinforcing the global shift towards reserve diversification and de-dollarization. This structural bid underpinned gold’s momentum even as the US Fed embarked on its most aggressive tightening cycle in four decades. With Fed rates rising from 0.25 percent in March 2022 to 5.50 percent by July 2023, the US dollar strengthened sharply, driving the DXY Index to 110 by late 2024. Yet, despite a stronger dollar—typically a headwind—geopolitical risk, sticky inflation, and subdued equity return outside AI pockets continued to push investors towards gold and other non-yielding assets.

Source: Geojit Research

Whenever gold has outperformed the Sensex, the Sensex/gold ratio has contracted below 1, also dragging the 1-year rolling Sensex return. As the outlook for gold has moderated for the short to medium-term, we can expect the future equity return to improve and stay elevated, as the ratio attempts to move upward towards the resistance of 1.5x times.

2025: A policy pivot and the beginning of gold’s exhaustion phase

Gold price strengthened in 2025. Expectations of further tightening evaporated as inflation eased, labour markets softened, and Fed policymakers began signalling comfort with a pivot. The Fed rate fell to 4.0 percent, with the market pricing in additional cuts for 2026. The dollar weakened, and with DXY index touching 96, gold became more affordable for non-dollar holders. This coincided with renewed uncertainty from escalating tariff wars, pushing demand even higher.

Source: Geojit Research

However, signs of fatigue have emerged by the end of the year. With gold up nearly 120 percent over three years, sustainability concerns have intensified. Profit-booking appears likely, particularly as the US signals willingness to soften its protectionist stance. Recent moderation in rhetoric from the Trump administration, alongside expectations of a US-China trade arrangement, have eased some of the anxiety that previously supported gold. India, too, anticipates a deal; which could stabilize global trade flows. Meanwhile, the dollar has started rebounding toward DXY 100, potentially exerting downward pressure on global gold prices.

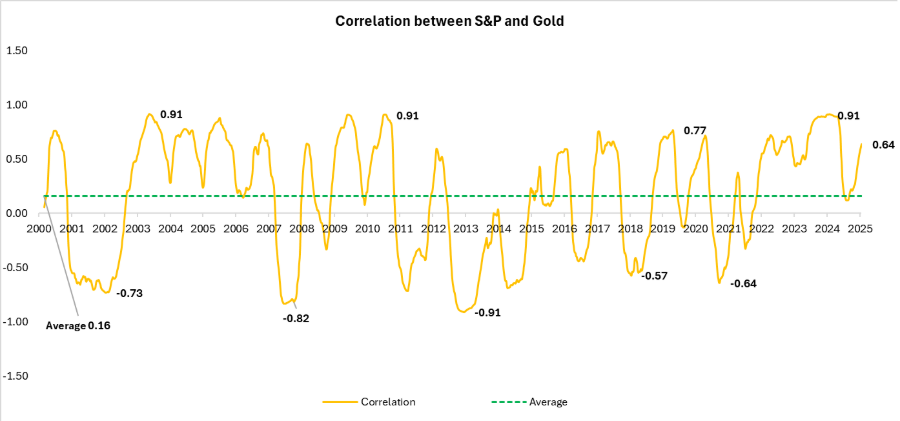

The long-term correlation between equity and gold is positive but narrow, at 0.16x with the S&P500. The ongoing rally in the US market is driven by AI stocks, indicative of a positive bias between the two asset classes. This trend can reverse with improvement in the broad economy stocks. A period of gold underperformance typically reinforces equity optimism, signalling a cooling-off in corrections and a potential upward move in long-term equity benchmarks.

Source: Geojit Research

Does gold’s correction pose a market risk? The Indian context says no

It does happen on a case-by-case basis, depending on the position of the economy and monetary policy. The likelihood of a downtrend spilling into Indian equity markets looks dim. Domestic markets are beginning to draw strength from improving earnings visibility and moderating inflation—both powerful counterweights to any negative sentiment stemming from precious metals, as it is positive for corporates and households. If the upcoming quarters confirm earnings upcycle and the Fed continues to cut rates in 2026, equities are positioned to see outsized gains, reducing the competitive appeal of traditional safe-haven assets.

Diminishing external risks and renewed domestic strength boost equities

Recent weeks have shown that global uncertainties—while influential—no longer dominate market direction the way they did during 2022–2025. This month, Indian equities, rebounded sharply and continued to rally despite a muted trend amid concerns over the Delhi explosion, as global cues improved. The passage of a bill ending the longest US federal shutdown and renewed optimism on a potential US–India trade deal fuelled the Nifty50 index to return above the key 26,000 mark. With Q2 corporate results broadly exceeding expectations for midcaps, the stage is set for domestic drivers to take the lead in market performance. PMI data has been mixed, but key indicators such as GST collections remain resilient even after rate rationalisation. Corporate results across the broad market have been strong, raising optimism for earnings upgrades in Q3.

A major positive surprise has emerged. India’s September CPI eased to 1.44 percent, followed by 0.25 percent in October, marking two consecutive months below the RBI’s lower tolerance threshold of 2 percent. While extremely low inflation could constrain growth in some contexts, the current moderation—driven primarily by food price stability and GST changes—gives the RBI greater flexibility to consider rate cuts to support economic expansion. The central bank expects inflation to rise modestly in early 2026 but remain comfortably within target ranges, suggesting growth in 2026.

Global markets stabilise, but AI valuations trigger tech-specific corrections

Global equities rallied on improved risk appetite following the US shutdown resolution and growing expectations of Fed rate cuts. Emerging markets, too, have benefited from the improvement in sentiment. However, US technology stocks—particularly AI-linked names—are undergoing valuation-driven corrections. Notably, SoftBank’s sale of its 32.1 million Nvidia shares for approximately $5.83 billion has amplified fears of stretched valuations in AI companies. Even when AI companies reported high quarterly reports, stocks could not sustain the trend. While India has limited direct exposure to this segment, some indirect effects can persist, underscoring the global interconnectedness of sectoral themes. However, Indian IT sector is expected to outperform, also benefiting from the implementation of AI leading to operational ease, GCC and data centre demand.

Why gold’s volatility could become an equity tailwind

Source: Geojit Research

As gold’s spectacular run begins to moderate, investors may increasingly rotate capital into equities, particularly in markets where earnings visibility is improving. Indian midcaps delivered 15–20 percent PAT growth in the latest quarter, strengthening the case for further upside. Again, the market has breached above the 26,000 level on the Nifty50; with domestic fundamentals strengthening and trade negotiations progressing positively, barriers this time look low.

In this context, a correction in gold is not a headwind but an opportunity—reducing the appeal of the non-yielding asset and pushing investors toward growth-oriented sectors. We continue to have a buy-on-dips approach as a sensible strategy for the Indian market. If the US-India trade deal materializes and becomes stronger, the equity outlook for 2026 becomes even more favourable, with global headwinds diminishing and domestic catalysts firmly in charge. FII’s outlook on India is catching up from neutral, as premium valuation has reduced and the earnings outlook is better.